The US Federal Reserve experienced an eventful week. On Monday, it contacted New York–based banks to assess their USD/JPY exposure, sparking speculation that Washington could be coordinating with Japan to address the Japanese Yen’s weakness. This development prompted a sharp sell-off in the US Dollar early in the week.

The Fed’s midweek policy meeting resulted in no change to the federal funds rate, which was kept within the 3.50%–3.75% range, in line with expectations. During his press conference, Chair Jerome Powell avoided questions related to politics, his tenure, and the subpoena. However, he pointed to improving economic momentum and reduced risks to both inflation and the labor market.

The US Dollar Index (DXY) has since rebounded toward the 96.90 level, recovering most of its weekly losses after President Donald Trump nominated former Fed Governor Kevin Warsh as the next Fed Chair on Friday. The nomination now awaits Senate approval. Looking ahead, the US is set to release several key data points next week, including the ISM Manufacturing PMI for January, MBA mortgage applications, Challenger job cuts, and weekly initial jobless claims.

EUR/USD is hovering around the 1.1880 area after the US Dollar rebounded and recovered nearly all of its weekly losses. In the coming week, Hamburg Commercial Bank (HCOB) will release Manufacturing, Services, and Composite PMIs for both Germany and the Eurozone. Additional Eurozone data include the ECB Bank Lending Survey and December Producer Price Index (PPI), while Germany will publish December Factory Orders and Industrial Production figures.

GBP/USD is trading near 1.3600 ahead of the Bank of England’s monetary policy announcement on Thursday. Governor Andrew Bailey’s subsequent press conference is expected to shed further light on the central bank’s outlook for interest rates. UK data releases include the final January S&P Global PMIs and the Halifax House Price Index.

USD/JPY is holding close to the 154.50 level, paring earlier gains after Tokyo CPI data indicated easing inflation in January. Headline inflation slowed to 1.5% year-over-year from 2% in December, while core measures eased to 2%, undershooting forecasts. The softer inflation profile reduces pressure on the Bank of Japan to tighten policy.

USD/CAD is trading around 1.3580, with the Canadian Dollar maintaining a slight edge against the greenback despite data showing economic stagnation in November. Monthly GDP was flat following a 0.3% contraction in the prior month and fell short of expectations for modest growth. Upcoming Canadian releases include January S&P Global PMIs and the Ivey PMI.

Gold is trading near the $4,880 area after surrendering all weekly gains. Prices retreated from a record high of $5,598 as profit-taking emerged and the US Dollar strengthened sharply.

Looking ahead: Emerging views on the economic outlook

Scheduled central bank speakers for the week:

Monday, February 2: – Bank of England’s Breeden – Federal Reserve’s Bostic

Tuesday, February 3: – Federal Reserve’s Barkin

Wednesday, February 4: – Federal Reserve’s Cook

Thursday, February 5: – Bank of England Governor Andrew Bailey – Federal Reserve’s Bostic – Bank of Canada Governor Tiff Macklem

Friday, February 6: – European Central Bank’s Cipollone – European Central Bank’s Kocher – Bank of England’s Pill – Federal Reserve’s Jefferson

Central bank meetings and upcoming data set to influence monetary policy decisions

Key economic data and policy events for the week:

Monday, February 2: – Germany’s December Retail Sales – US ISM Manufacturing PMI

Tuesday, February 3: – Reserve Bank of Australia monetary policy decision – US December JOLTS job openings

Wednesday, February 4: – Eurozone January Harmonized Index of Consumer Prices (HICP) – US January ADP employment report

Thursday, February 5: – Australia’s December trade balance – Eurozone December retail sales – Bank of England monetary policy decision – European Central Bank monetary policy decision

Friday, February 6: – Canada’s January employment change – US January nonfarm payrolls – US February Michigan consumer sentiment

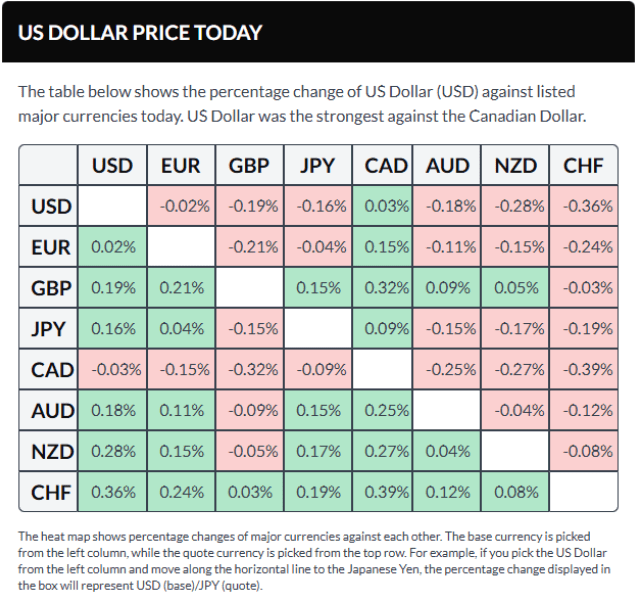

Most Asian currencies traded in narrow ranges on Friday, while the U.S. dollar held firm near a six-week high, supported by upbeat U.S. economic data and growing expectations that Federal Reserve rate cuts are not imminent.

The US Dollar Index tarded largely flat during Asian hours after rising to its highest since early December overnight

US Dollar Index Futures also traded flat as of 03:35 GMT.

Strong U.S. data delays expectations of Fed rate cuts

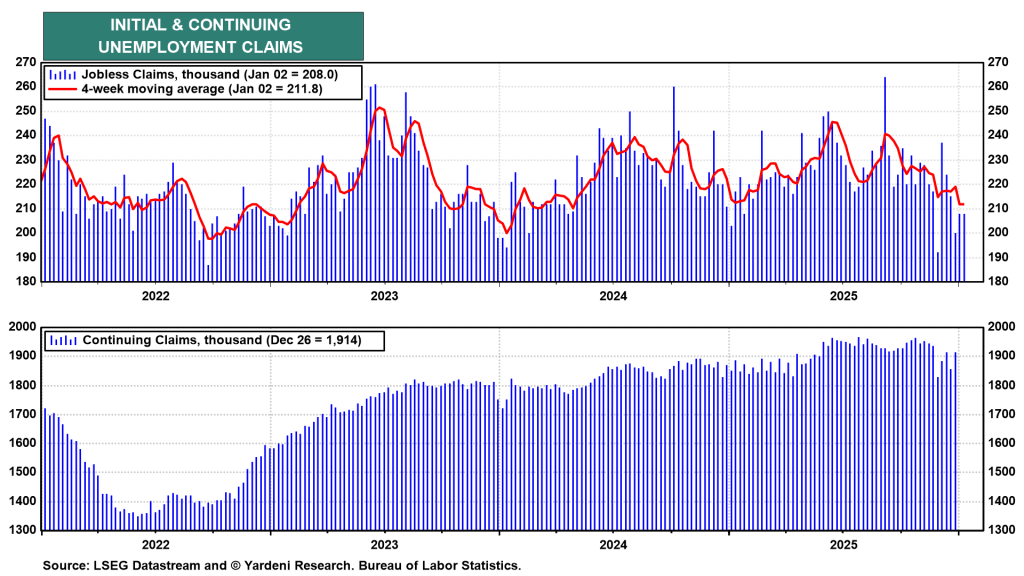

U.S. initial jobless claims unexpectedly declined to 198,000 last week, beating forecasts of 215,000 and underscoring ongoing resilience in the labor market.

The figures strengthened expectations that the Federal Reserve will leave interest rates unchanged for a longer period, with traders now projecting the first rate reduction around the middle of the year. Remarks from multiple Fed officials overnight further contributed to the cautious sentiment.

Policymakers indicated they may delay rate cuts at the upcoming meeting, pointing out that employment conditions remain firm while inflation pressures have yet to fully ease.

Yen holds firm on government backing; won heads for weekly loss

In Japan, the yen inched higher after hovering near 18-month lows, with USD/JPY slipping 0.3%. The currency gained some backing following verbal interventions from government officials aimed at curbing its rapid decline.

“Recent headlines suggest the Bank of Japan is growing uneasy about the yen’s weakness, and BOJ policymakers now view the exchange rate as having a bigger impact on inflation,” MUFG analysts noted.

The yen has faced persistent pressure amid rising speculation that Prime Minister Sanae Takaichi may call an early snap election as soon as next month. Markets view the prospect of a vote as negative for the currency, on expectations of looser fiscal policy and increased government spending.

Across Asia, the South Korean won saw USD/KRW climb 0.2%, putting it on track for a gain of more than 1% this week, despite Thursday’s pullback. Brief support came earlier in the week after remarks from U.S. Treasury Secretary Scott Bessent helped bolster sentiment toward the currency.

In China, the onshore yuan (USD/CNY) was steady, while the offshore rate (USD/CNH) inched 0.1% higher. The Indian rupee (USD/INR) and the Singapore dollar (USD/SGD) were little changed, while Australia’s AUD/USD pair added 0.1% on Friday.

If economists were meteorologists, this week’s forecast would predict a data blizzard. However, clarity is expected to improve as markets receive highly anticipated reports on inflation, retail sales, and industrial production ahead of the Federal Reserve’s policy meeting on January 28.

Few economists expect Fed Chair Jerome Powell and the Federal Open Market Committee (FOMC) to ease monetary policy again later this month—and neither do we. This week’s data could either confirm or challenge that view, starting with the December consumer price index report on Tuesday.

The Fed drama intensified last week after President Donald Trump instructed Fannie Mae and Freddie Mac to purchase $200 billion in mortgage bonds—an action typically undertaken by the Fed itself. Many saw this move as an attempt to restart quantitative easing. Meanwhile, Fed Governor Stephen Miran told Bloomberg he anticipates 150 basis points of rate cuts this year.

What’s still missing, however, is significantly lower inflation and a recession that would justify such aggressive easing. This week will also feature speeches from several Fed officials, which could provide insight into the central bank’s thinking. The lineup starts with New York Fed President John Williams on Monday, followed by Governors Miran (Wednesday), Michael Barr (Thursday), Michelle Bowman (Friday), and Vice Chair Philip Jefferson (Friday).

Here’s a rundown of this week’s key data releases likely to influence the timing and scale of any future Fed rate cuts:

Inflation

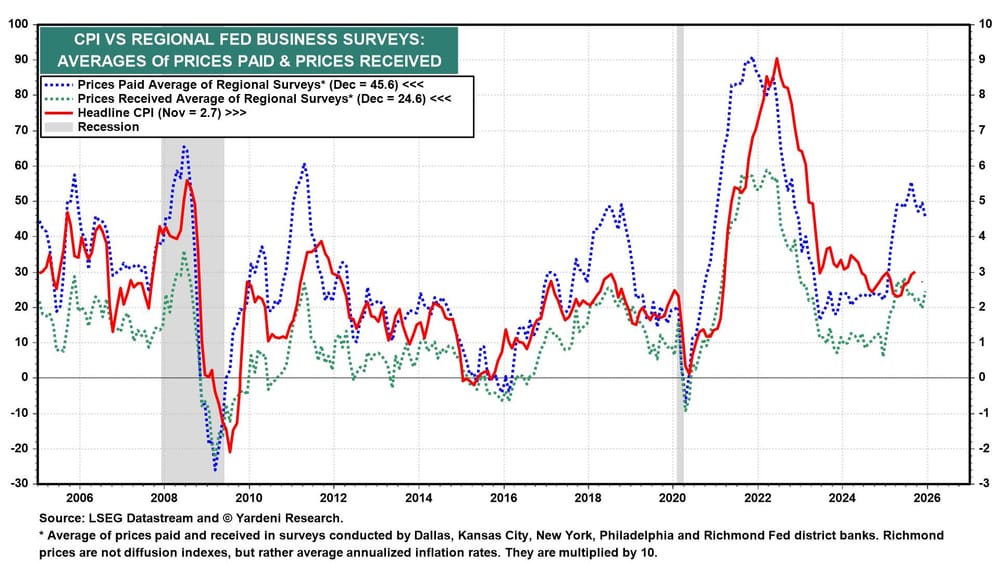

Since the 43-day government shutdown in October and November, investors have struggled to gauge inflation accurately. The 2.7% year-over-year CPI rise in November, a slight dip from October’s 3.0%, was met with caution, as the shutdown likely disrupted the Bureau of Labor Statistics’ data gathering.

This increases the importance of the upcoming CPI and PPI reports, which will be key indicators before the FOMC’s January 28 interest rate decision.

The upcoming CPI report on Tuesday is expected to show a modest easing in inflation, with the Cleveland Fed’s model forecasting a 0.2% monthly increase and 2.6% year-over-year growth. The November PPI report, due Wednesday, is considered less impactful, while import and export price data for November will be released on Thursday.

Retail sales

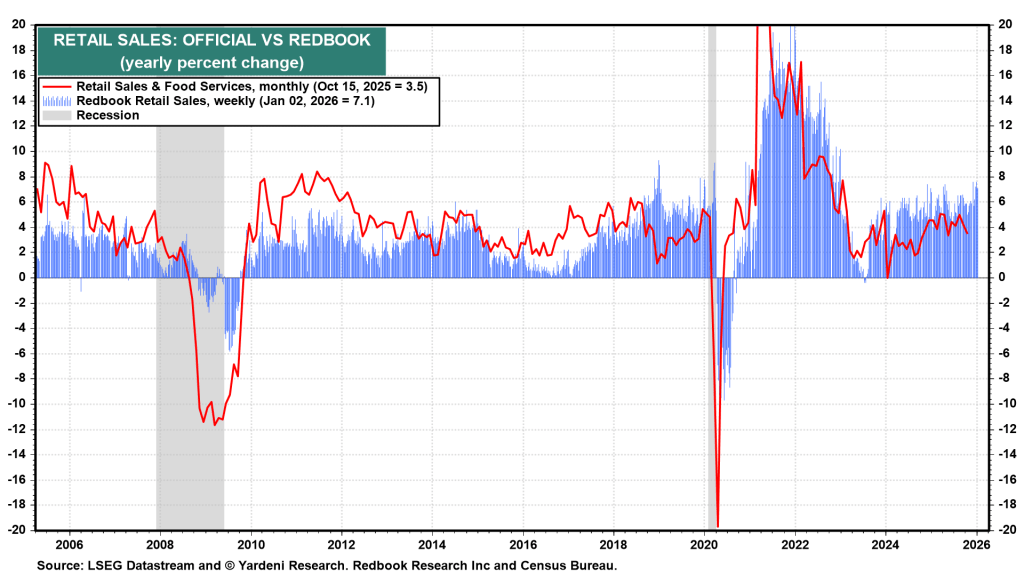

Retail sales (Wednesday) are expected to show a slight increase in November after remaining flat in October (see chart). Overall, we believe consumer spending remains resilient despite rising living costs and soft employment figures. Additional important demand indicators this week include December existing home sales (Wednesday) and mortgage applications for the week ending January 9 (Wednesday).

Jobless claims

We anticipate layoffs will stay minimal, which has been the key insight from recent initial unemployment claims data (Thursday) (see chart). While demand for labor may be slowing in certain sectors, the feared AI-driven collapse in the job market has not materialized yet.

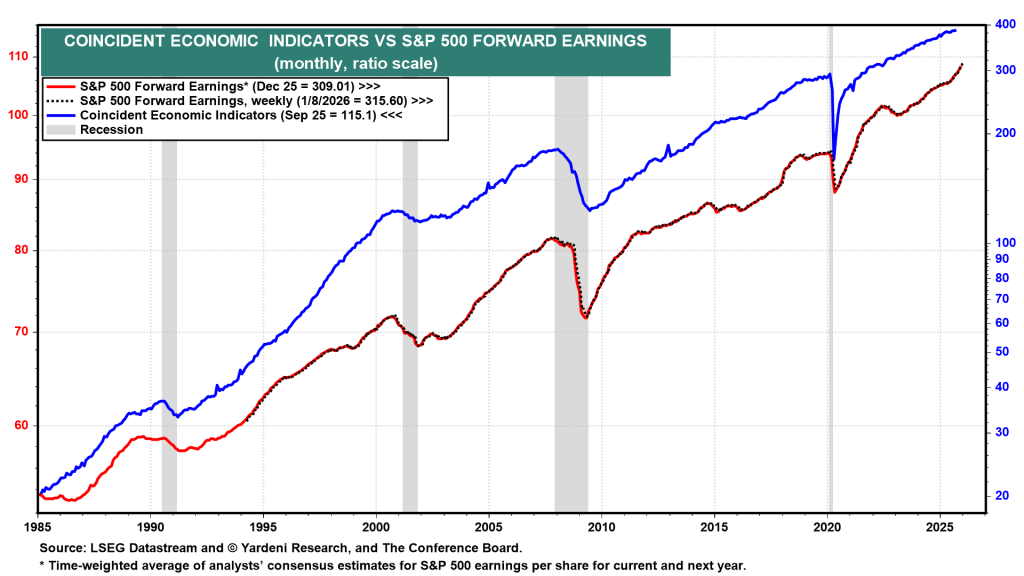

Composite economic indicators & business surveys

The composite cyclical indicators for December, due Thursday, are expected to show the coincident index holding at a record high, while the (mis)leading index continues its decline. Additionally, given delays in official hard data, the National Federation of Independent Business’ Small Business Optimism Index for December (Tuesday) should provide valuable insights, following its rise to 99 in November. Later in the week, the Federal Reserve banks of New York and Philadelphia will release their January business surveys (Thursday).

Our preferred coincident indicator is the S&P 500 forward earnings per share, which has accelerated in recent weeks and hit record highs (see chart).

U.S. employment figures reinforce the Federal Reserve’s cautious stance on monetary policy. Meanwhile, Europe’s economic growth remains sluggish, but policymakers appear comfortable with the current pace. As demand for the U.S. Dollar stays strong, the EUR/USD pair has potential to continue its downward move toward the 1.1470 level.

The EUR/USD pair opened the year on a weak note, declining for the second week in a row to hover near 1.1640, marking its lowest level in a month. The US Dollar gained strength across the foreign exchange market, supported by geopolitical tensions and robust US employment figures.

Geopolitical Unrest Drives Financial Markets Early in 2026

On Saturday morning, the world learned that U.S. President Donald Trump had executed a precise military operation in Venezuela, capturing then-President Nicolás Maduro and his wife, Cilia Flores, and transporting them to the United States to face charges related to narco-terrorism. Delcy Rodriguez, Maduro’s Vice-President, has now taken control of Venezuela. Although there was initial criticism of Trump’s actions, Rodriguez quickly shifted her stance and expressed willingness to cooperate with the U.S.

President Donald Trump did not hide his motives for the U.S. military action in Venezuela. At a press conference following the operation that removed Nicolás Maduro from power, Trump said the United States would exercise control over Venezuela and its oil resources and warned of further measures if the Venezuelan government resisted. He described a future “transition” for the country’s governance, but did not outline specific plans for democracy or civilian rule.

In the days after the raid, international tensions gradually eased, but the situation remained unresolved. One clear strategic factor behind the U.S. intervention was limiting Venezuela’s oil ties with major global powers, including Russia and China — a goal linked to broader geopolitical rivalry.

Meanwhile, Russia carried out a significant missile strike on Ukraine early on Friday, shortly after Ukraine and its European partners agreed on elements of postwar security guarantees. The attack was widely interpreted as Russian President Vladimir Putin challenging Western support for Kyiv and signaling that sanctions, including restrictions on Russian oil, would not deter Moscow’s military actions.

In addition, Trump reignited controversy with comments about Greenland, an autonomous territory of Denmark. He argued that the U.S. needs Greenland for national security reasons and suggested Washington might pursue control of the island — a stance that drew criticism from European leaders and sparked fears of future U.S. territorial ambitions.

Europe Maintains Ongoing Stability

News from Europe has had little impact on the Euro (EUR), which is understandable given the Eurozone’s fragile yet steady stability, with ongoing growth, manageable inflation, and no significant employment concerns.

Eurostat reported that the seasonally adjusted unemployment rate in the Euro area stood at 6.3% in November, slightly down from 6.4% in October 2025 but up from 6.2% in November 2024. The broader EU unemployment rate remained stable at 6.0% in November 2025 compared to October, though it rose from 5.8% a year earlier.

The Hamburg Commercial Bank (HCOB) released the final December figures for the Eurozone’s Services and Composite Purchasing Managers’ Indexes (PMIs). The data showed a twelfth consecutive monthly increase in private sector activity, with the Composite PMI at 51.5, down from 52.8 in November. Services output also declined to 52.4 from 53.6, marking three-month lows for both indicators.

Regarding inflation, Germany’s preliminary December Harmonized Index of Consumer Prices (HICP) increased 2% year-over-year, lower than November’s 2.6% and below the 2.2% forecast. Monthly inflation rose by 0.2%, half the expected 0.4%. The Eurozone’s overall HICP inflation matched expectations at 2% annually, with a 0.2% monthly rise following November’s 0.2% decline.

Germany reported mixed figures for November, with retail sales falling 0.6% while industrial production saw a modest 0.8% increase.

On monetary policy, European Central Bank (ECB) Vice President Luis de Guindos told Bloomberg that current interest rates are appropriate as inflation targets have been met, though uncertainty remains high. This aligns with the ECB’s current stance: pausing rate changes while maintaining vigilance.

U.S. Employment and Economic Growth Update

The U.S. macroeconomic calendar was busy with key data mostly signaling progress. The Institute for Supply Management (ISM) reported December Manufacturing PMIs, showing a contraction in manufacturing output as the index fell to 47.9 from 48.2 in November, below expectations of 48.3. However, the Employment Index improved slightly to 44.9 from 44, while the Prices Paid Index remained steady at 58.5. Meanwhile, the Services PMI rose to 54.4 from 52.6, with the employment sub-index increasing to 52 from 48.9 and the Prices Paid Index easing to 64.3 from 65.4.

The trade deficit narrowed sharply to $59.1 billion in October, down from $78.3 billion, reflecting the impact of Trump’s policies.

Employment data was mostly positive. The ADP report showed private sector job growth of 41,000 in December, a bit below the expected 47,000 but an improvement over November’s revised -29,000. The JOLTS report recorded 7.146 million job openings at November’s end, down from 7.449 million in October. Job cuts announced in December dropped 50% from November to 35,553, the lowest monthly total since July 2024.

The December Nonfarm Payrolls (NFP) report showed 50,000 new jobs added, below the 60,000 forecast, while the unemployment rate fell to 4.4%, better than the anticipated 4.5%. November’s payrolls were revised down to 56,000 from 64,000. This data put some short-term pressure on the USD but did not alter the Federal Reserve’s cautious monetary policy.

The Fed cut interest rates by 25 basis points in December as expected, signaling the possibility of one more cut in 2026—less than markets hope but consistent with a cautious stance focused on employment. Market watchers anticipate at least two rate cuts this year, especially with Chairman Jerome Powell’s term ending in May and a likely replacement aligned with Trump’s preference for more aggressive easing. Still, no immediate Fed action is expected in the first meeting of 2026.

What’s coming up next on the agenda?

In the days ahead, attention will turn to U.S. inflation data, with the December Consumer Price Index (CPI) scheduled for release on Tuesday, followed by the Producer Price Index (PPI) for October and November on Wednesday. November Retail Sales data will also be published on Wednesday. These reports are expected to influence the Federal Reserve’s future policy decisions and, consequently, the direction of the U.S. Dollar.

EUR/USD technical analysis

From a technical standpoint, the daily chart shows a bearish outlook for EUR/USD with potential for further decline. The 20-day Simple Moving Average (SMA) is trending downward but still sits above the 100- and 200-day SMAs, indicating weakening short-term momentum. The price remains below the 20-day and 100-day SMAs at 1.1733 and 1.1666 respectively, while the rising 200-day SMA at 1.1571 acts as support. The Momentum indicator has dropped below its midpoint, maintaining strong bearish momentum, and the Relative Strength Index (RSI) is falling toward 36, suggesting lower prices ahead. A close above the 100-day SMA at 1.1666 could relieve some selling pressure and target the 20-day SMA at 1.1733, but failure to break this resistance leaves the pair vulnerable to test the 200-day SMA support at 1.1571.

On a broader scale, the weekly chart also points to continued bearishness. The pair trades beneath the flattened 20-week SMA near 1.1665, with upside limited by this level. The 100- and 200-week SMAs are rising at 1.1085 and 1.0856 but remain far below the current price, so they are less relevant short term. The Momentum indicator on the weekly chart has turned downward but stays within neutral territory, while the RSI is declining around 52.

If the pair falls below the key 1.1600 level, the next significant support lies near 1.1470, a major long-term pivot. Overall, bears will maintain control as long as EUR/USD stays below the 1.1740-1.1750 resistance zone.

Most Asian stock markets saw modest gains on Friday, following a mixed close on Wall Street as investors remained cautious ahead of crucial U.S. jobs data that could influence expectations for future Federal Reserve interest rate cuts.

U.S. markets closed Thursday with mixed results: technology stocks pulled back after recent advances, putting pressure on the Nasdaq, while the Dow and S&P 500 showed little movement.

Futures for major Wall Street indexes remained mostly flat during Friday’s Asian trading session.

Asian stocks mostly flat as Nikkei posts gains

Asian markets showed limited movement, reflecting investor caution, with the technology sector leading declines.

South Korea’s KOSPI index remained mostly flat after reaching record highs earlier in the week, as chipmakers Samsung Electronics (KS:005930) and SK Hynix (KS:000660) dropped between 1.5% and 3%.

Australia’s S&P/ASX 200 gained 0.3%, while Singapore’s Straits Times Index held steady.

Futures for India’s Nifty 50 also remained largely unchanged.

In contrast, Japanese stocks outperformed the region, with the Nikkei 225 rising 1% and the broader TOPIX index increasing 0.3%. A weaker yen against the U.S. dollar supported exporters’ prospects.

Looking ahead, investor attention is focused on the U.S. nonfarm payrolls report expected later on Friday, which could offer crucial insights into the health of the world’s largest economy and influence the Federal Reserve’s monetary policy outlook.

China’s December CPI reaches highest level in 3 years, PPI deflation slows

In China, official data released on Friday showed consumer inflation rose to its highest level in nearly three years, offering tentative signs of improving demand.

The consumer price index increased 0.8% year on year in December, the fastest pace in about 34 months, while monthly prices rose 0.2%. At the same time, producer price deflation eased, indicating some stabilization in factory-gate prices.

The data indicated that China could be nearing an end to a prolonged deflationary period that has dampened economic growth, squeezed corporate earnings, and restrained consumer spending.

China’s blue-chip Shanghai Shenzhen CSI 300 index gained 0.3%, while the Shanghai Composite rose 0.6%. Hong Kong’s Hang Seng traded flat.

U.S. stock index futures were mostly flat on Wednesday evening, after Wall Street’s major benchmarks ended the session broadly lower from record highs, as investors looked ahead to key U.S. employment data due later this week.

S&P 500 futures edged up 0.1% to 6,967.0, while Nasdaq 100 futures were little changed at 25,837.25 by 20:03 ET (01:03 GMT). Dow Jones futures also added 0.1% to 49,263.0.

Wall Street Pulls Back From Record Highs Ahead of U.S. Jobs Data

During the session, the S&P 500 declined 0.3%, while the Dow Jones Industrial Average dropped 0.9%. In contrast, the Nasdaq Composite added 0.2%, supported by selective gains among large-cap technology stocks that helped offset broader market weakness.

Both the S&P 500 and the Dow had reached record highs in the previous session, and the mixed performance pointed to some profit-taking after the recent rally.

Figures from payroll processor ADP showed that private-sector job growth in December came in below expectations, signaling a slowdown in hiring momentum toward year-end.

Although the ADP report is often seen as volatile and not always a reliable guide to official government data, it added to evidence that the labor market may be gradually cooling.

Focus now shifts to Friday’s highly anticipated nonfarm payrolls report, which is expected to offer clearer insight into employment trends and wage growth. The data will be closely watched by markets evaluating the probability and timing of potential Federal Reserve rate cuts in the months ahead. Weaker-than-expected job growth could reinforce expectations that the Fed may begin easing policy earlier in 2026.

Attention on rising tensions between the US and Venezuela

Geopolitical strains continued to run high after U.S. forces apprehended Venezuelan President Nicolás Maduro, yet financial markets have so far exhibited only limited, short‑lived reactions to the dramatic turn of events. Investors appear to be largely unfazed by the heightened political risk, although the episode has introduced fresh uncertainty into the outlook for energy markets. U.S. President Donald Trump stated that Venezuela’s interim leadership would transfer up to 50 million barrels of crude oil to the United States.

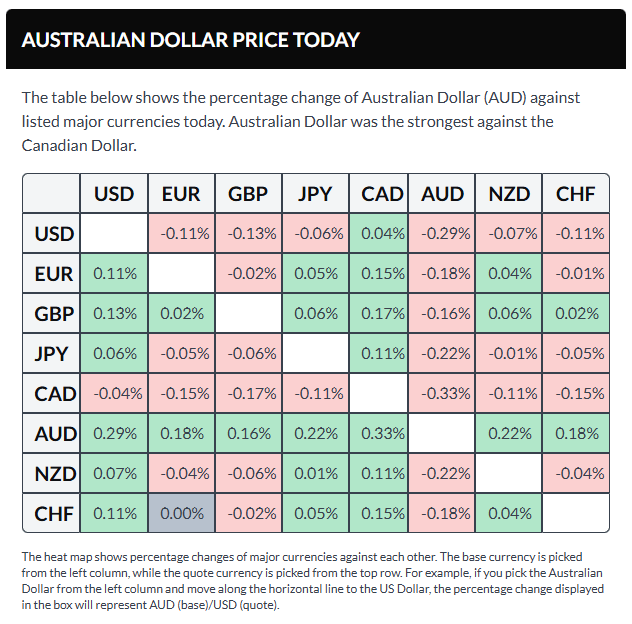

The Australian Dollar gains ground amid a hawkish outlook on the Reserve Bank of Australia (RBA).

Australia’s CPI slowed to 3.4% year-over-year in November, below expectations but still above the RBA’s target range.

Traders now turn their attention to Wednesday’s US ISM Services PMI and JOLTs job openings reports for further market cues.

The Australian Dollar (AUD) extended its winning streak for the fourth consecutive session on Wednesday, gaining against the US Dollar (USD) despite easing inflation figures for November. Traders are now focused on the upcoming full fourth-quarter inflation report due later this month. Analysts caution that a core inflation increase of 0.9% or more could prompt the Reserve Bank of Australia (RBA) to consider further tightening at its February meeting.

Meanwhile, the Australian Financial Review (AFR) highlighted that the RBA may not be finished with its rate hikes this cycle. A recent poll suggests inflation is likely to remain persistently high over the coming year, supporting expectations for at least two more rate increases.

The Australian Bureau of Statistics (ABS) reported on Wednesday that Australia’s Consumer Price Index (CPI) rose 3.4% year-over-year (YoY) in November, easing from 3.8% in October. This figure missed market expectations of 3.7% but stayed above the Reserve Bank of Australia’s (RBA) target range of 2–3%. It marked the lowest inflation rate since August, with housing costs rising at their slowest pace in three months.

Month-on-month (MoM), Australia’s CPI remained flat at 0% in November, matching October’s reading. Meanwhile, the RBA’s Trimmed Mean CPI increased 0.3% MoM and 3.2% YoY. In a separate report, seasonally adjusted building permits surged 15.2% MoM to a near four-year high of 18,406 units in November 2025, bouncing back from a downwardly revised 6.1% decline the previous month. Annual approvals jumped 20.2%, reversing a revised 1.1% drop in October.

US Dollar declines ahead of ISM Services PMI

The US Dollar Index (DXY), which tracks the US Dollar’s value against six key currencies, is slightly declining after posting small gains in the previous session, currently hovering near 98.50. Market participants are awaiting US economic releases that may influence Federal Reserve (Fed) policy outlooks. Later today, attention will be on the ISM Services Purchasing Managers’ Index (PMI) and JOLTs job openings data. The upcoming US Nonfarm Payrolls (NFP) report, due Friday, is forecasted to show an increase of 55,000 jobs in December, a decrease from 64,000 in November.

Fed Governor Stephen Miran stated on Tuesday that the central bank should pursue aggressive interest rate cuts this year to bolster economic growth. Conversely, Minneapolis Fed President Neel Kashkari cautioned that unemployment could unexpectedly rise. Richmond Fed President Tom Barkin, who is not voting on this year’s rate decisions, emphasized that rate changes will need to be carefully calibrated to incoming data, pointing to risks affecting both employment and inflation targets, per Reuters.

According to CME Group’s FedWatch tool, futures markets assign roughly an 82.8% chance that the Fed will keep rates steady at the January 27–28 meeting.

On the geopolitical front, the US launched a significant military strike on Venezuela last Saturday. President Donald Trump announced that Venezuelan President Nicolas Maduro and his wife were captured and removed from the country. However, Maduro pleaded not guilty on Monday to US narcotics-terrorism charges, signaling a high-stakes legal confrontation with wide geopolitical consequences, Bloomberg reports.

Traders anticipate two more Fed rate cuts in 2026. Markets also expect Trump to nominate a new Fed chair to succeed Jerome Powell when his term expires in May, potentially steering monetary policy toward lower rates.

In China, the Services PMI from RatingDog fell slightly to 52.0 in December from 52.1 in November, while Manufacturing PMI rose to 50.1 from 49.9 the previous month. Given China’s close trade ties with Australia, shifts in the Chinese economy may affect the Australian Dollar.

The Reserve Bank of Australia’s December meeting minutes revealed readiness to tighten monetary policy further if inflation does not ease as expected. Greater attention is now on the Q4 Consumer Price Index report scheduled for January 28, with analysts warning that a stronger-than-anticipated core inflation figure could prompt a rate hike at the RBA’s February 3 meeting.

The Australian Dollar has reached new 14-month highs, climbing above the 0.6750 level

On Wednesday, AUD/USD is trading near 0.6750. Technical analysis of the daily chart shows the pair moving upward within an ascending channel, indicating a continued bullish trend. However, the 14-day Relative Strength Index (RSI) at 70 signals that the pair may be overbought.

Since October 2024, AUD/USD has hit new highs and is now aiming for the upper boundary of the ascending channel around 0.6830.

Initial support is found at the nine-day Exponential Moving Average (EMA) near 0.6708, followed by the lower boundary of the ascending channel at about 0.6700. A drop below this combined support zone could push the pair down toward the 50-day EMA level at approximately 0.6625.

Financial markets extended the holiday-thinned mood on the first trading day of the new year, with investors largely staying on the sidelines. Markets remain in a wait-and-see mode ahead of a data-heavy week.

The US Dollar Index (DXY) traded near the 98.40 area on Friday, paring a significant portion of its New Year losses.

Gold (XAU/USD) traded around the $4,320 level, surrendering all intraday gains following the New Year’s break. Expectations of lower US interest rates and elevated geopolitical tensions have continued to support precious metals in recent sessions.

EUR/USD hovered near 1.1740 after edging lower earlier in the week, remaining under pressure as investors await upcoming economic data.

GBP/USD traded close to the 1.3480 area, little changed during the first US session of the year.

USD/JPY hovered around the 156.50 region, trading slightly lower on the day with limited intraday movement.

AUD/USD traded near the 0.6690 area on Friday, posting modest gains after paring nearly half of its intraday advance.

Key Economic Data Ahead: Upcoming Releases Set to Shape Market Sentiment

Over the coming days, investors will closely watch US employment figures and global inflation data, which are expected to influence central bank policies.

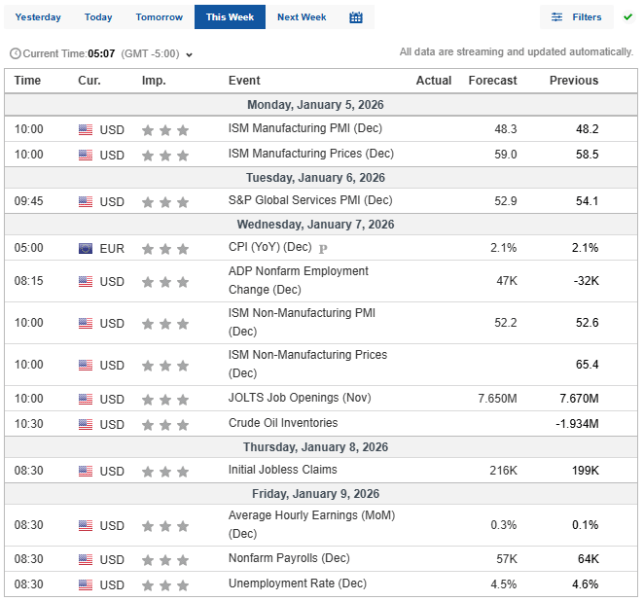

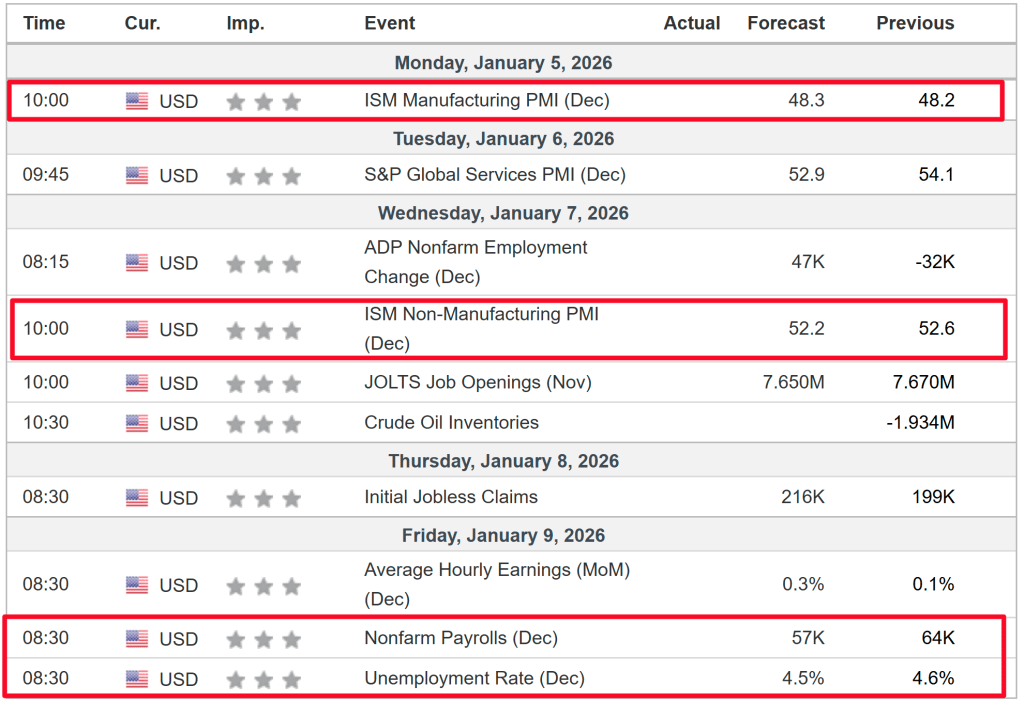

Monday: The US Institute for Supply Management (ISM) releases the Manufacturing Purchasing Managers’ Index (PMI) for December.

Tuesday: Germany’s Harmonized Index of Consumer Prices (HICP) and Australia’s Consumer Price Index (CPI) are scheduled for publication.

Wednesday: The US ADP Employment Change report (December), ISM Services PMI (December), and the preliminary Eurozone HICP (December) will be released.

Thursday: The US Trade Balance for October and Consumer Credit data for November are due.

January 9: The highly anticipated US Nonfarm Payrolls (NFP) report for December and the preliminary January Michigan Consumer Sentiment Index will be published.

These releases are expected to set the tone for market direction and provide clues on the pace of monetary tightening by major central banks.

This week’s highlights include the U.S. jobs report, ISM PMI surveys, and the CES Conference.

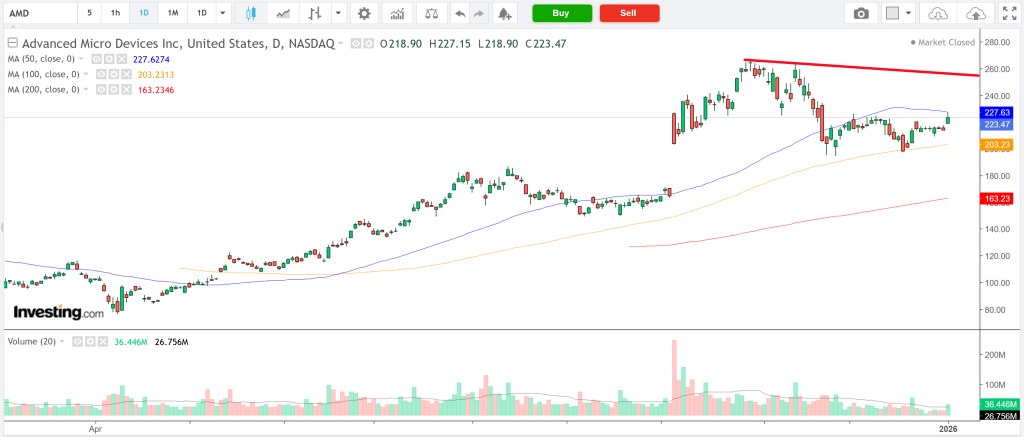

AMD is a recommended buy, driven by expected AI innovations presented in CEO Lisa Su’s CES keynote.

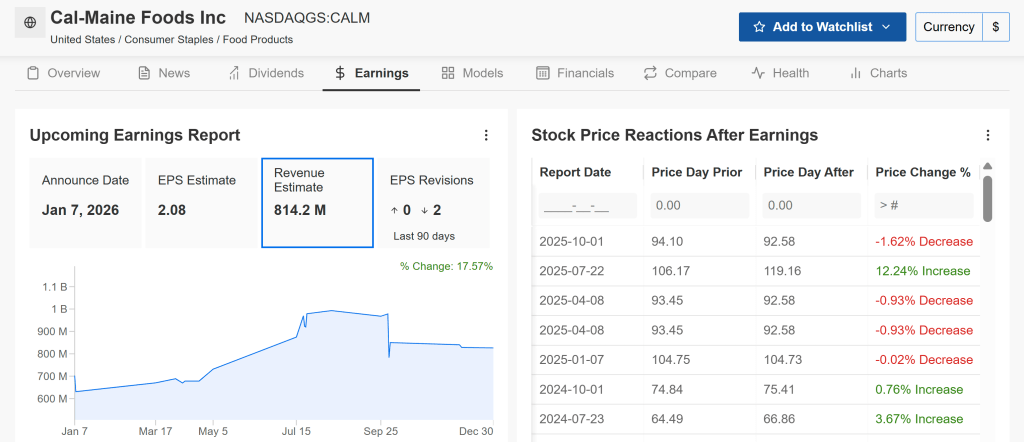

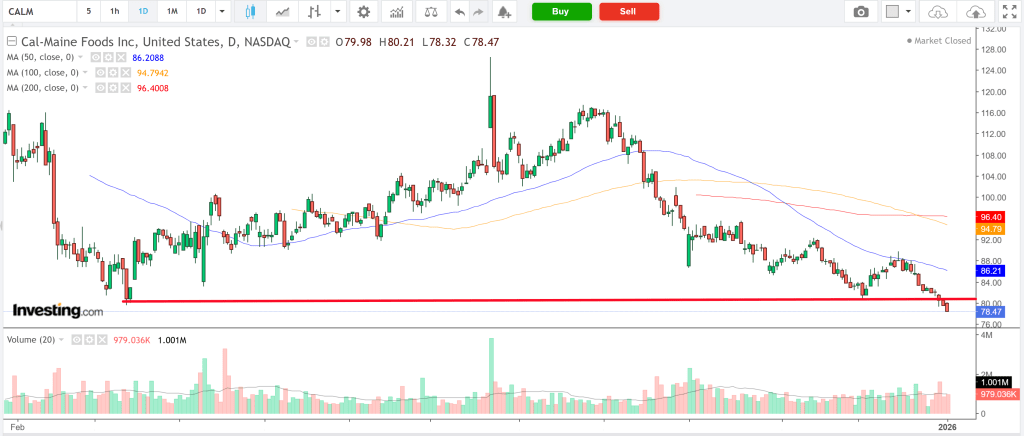

Cal-Maine Foods is a sell candidate ahead of a potentially disappointing earnings report and a weak outlook.

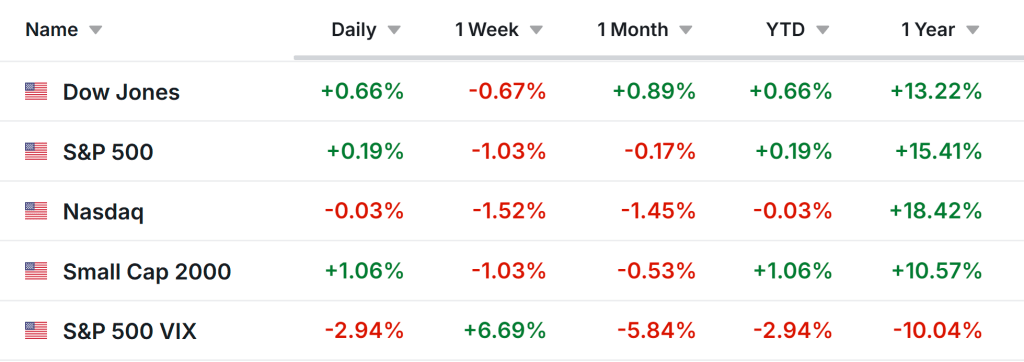

Wall Street’s major indexes closed mostly higher on Friday, the first trading day of 2026, boosted by gains in semiconductor and AI-related stocks. However, all three indexes still recorded slight declines for the week.

The Dow Jones Industrial Average slipped 0.7%, the S&P 500 dropped 1%, the tech-focused Nasdaq Composite fell 1.5%, and the small-cap Russell 2000 declined 1%.

The first full trading week of 2026 promises to be busy, with monthly jobs data taking center stage. Economists forecast nonfarm job growth of 54,000 for January, down from 67,000 in December, while the unemployment rate is expected to decrease to 4.5% from 4.6%. Additionally, the ISM manufacturing and services PMIs will be closely monitored by investors.

On the earnings front, only a few companies are scheduled to report this week, including Constellation Brands, Cal-Maine Foods, Jefferies Financial Group, Albertsons, and Applied Digital.

Meanwhile, investors in the tech and consumer sectors will be closely watching the CES conference in Las Vegas. Key companies to watch for product launches, strategic updates, and AI developments include Nvidia, AMD, Intel, Qualcomm, Meta Platforms, Samsung, LG, Sony, and Motorola.

No matter how the market moves, below I highlight one stock expected to gain interest and another that may face further declines. Keep in mind, my outlook is limited to the upcoming week, Monday, January 5 through Friday, January 9.

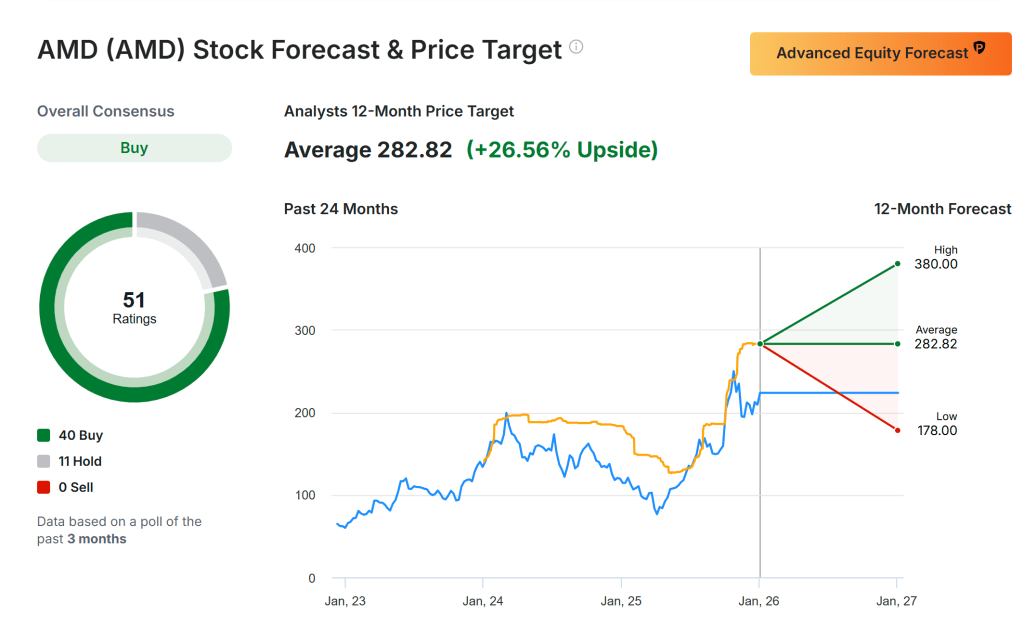

Stock to Buy: Advanced Micro Devices

AMD stands out as a strong buy this week, with the 2026 Consumer Electronics Show (CES) acting as a key catalyst. The highlight will be CEO Dr. Lisa Su’s opening keynote on Monday at 6:30 PM PT (9:30 PM ET).

Su is expected to present AMD’s vision for AI solutions across cloud, enterprise, edge, and devices, potentially unveiling new advancements in AI chips and related technologies. Historically, AMD shares tend to rally during the week of its major product announcements, often followed by multiple analyst upgrades.

Analysts remain optimistic, with a consensus Strong Buy rating supported by 40 Buy and 11 Hold recommendations, suggesting a 26.5% upside potential for 2026. TD Cowen recently named AMD among its top AI picks, setting a price target of $290.

Fundamentally, AMD’s growth is driven by its AI product portfolio, including the MI300 series accelerators, which are gaining ground against rivals like Nvidia.

AMD shares closed Friday at $223.47. From a technical standpoint, the stock has demonstrated resilience, recovering from mid-2025 lows near $150 to its current level, supported by strong trading volume. If the upcoming keynote meets expectations with announcements like new partnerships or product roadmaps, AMD could soon challenge its 52-week high around $270.

AMD holds a Financial Health Score of 2.98 (“GOOD”), indicating a solid balance sheet and strong operating momentum driven by excitement around its next-generation AI products.

Stock to Sell: Cal-Maine Foods

Cal-Maine Foods starts the week at $78.47, hovering near its 52-week low, as Wall Street anticipates a weak earnings report and a bleak outlook. The company faces headwinds including rising feed costs, supply chain challenges, and variable demand.

The largest U.S. producer and distributor of shell eggs is set to release its fiscal second-quarter results before the market opens on Wednesday at 6:00 AM ET, followed by a conference call at 9:00 AM ET.

Cal-Maine is projected to report earnings of $2.08 per share, a sharp 53.5% decline from $4.47 a year ago, driven by higher input costs and fluctuating demand. Revenue is expected to drop 14.7% year-over-year to $814.2 million, amid ongoing egg price volatility and potential disruptions from recent avian flu outbreaks that have affected supply chains.

Looking forward, the company’s guidance is likely to reflect continued uncertainty around production normalization and cost control, posing further challenges for investor confidence and stock performance.

Technically, CALM has slipped below key support levels, accompanied by declining volume that indicates weakening investor interest. Its one-year target price of $95.50 offers limited upside, but the risks from a disappointing earnings report outweigh potential gains.

With the likelihood of underwhelming results and cautious guidance, CALM is a sell this week to avoid volatility driven by these events.

Whether you’re a beginner investor or an experienced trader, using InvestingPro can help you uncover investment opportunities while managing risks in this challenging market environment.