Early on, some questionable US labor market data set the tone, but the real catalyst was the shift to a risk-off mood. Day two is often decisive. We also cover updates from the ECB and BoE—no policy changes, but plenty of developments.

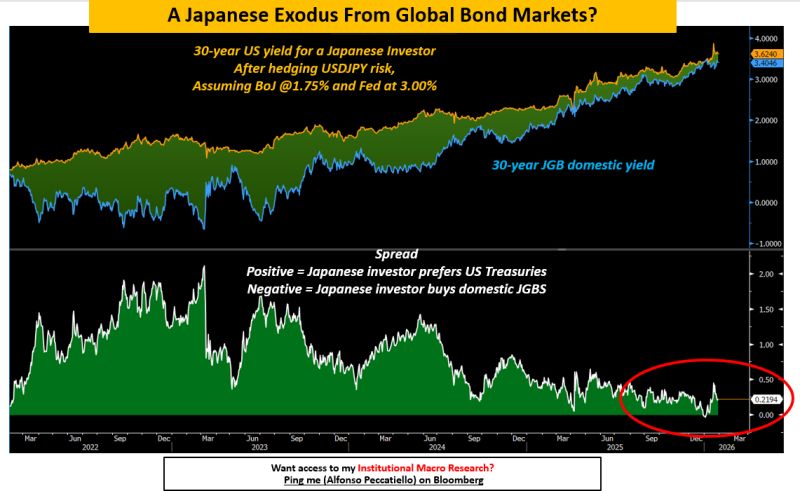

A growing sense of decay fuels demand for Treasuries

Markets reacted sharply to weaker US labor data on Thursday—arguably an overreaction. Challenger job cuts came in elevated, and headlines noting the highest January reading since 2009 quickly raised alarm. However, a higher figure was recorded as recently as October 2025, and the series itself is notoriously volatile.

A move lower in yields was the appropriate response, but the magnitude was reinforced by subsequent JOLTS data, which showed job openings falling more than expected. Openings remain sizeable at around 6.5 million, though down from 7.2 million. Initial jobless claims also edged higher, but the increase was modest and levels remain low in a broader historical context.

Broader market dynamics added fuel to the move. A pronounced risk-off backdrop—particularly concerns surrounding private credit—typically channels demand into Treasuries. Technical factors also played a role, with key thresholds giving way: the 10-year yield broke below 4.2%, while the 2-year slipped under 3.45%. While not extreme relative to recent months, the move was nevertheless notable. Hard to fight the move, particularly if the risk-off reassessment proves durable.

ECB meeting takes a back seat to global risk sentiment

A dovish tilt from the Bank of England, softer US labor signals, and persistent equity-market jitters have had a greater influence on markets than the ECB, with the 2s10s Bund curve modestly reflattening in a bullish move—still comfortably within recent ranges. The VIX remains elevated, indicating ongoing caution around potential equity volatility. While there has been no broad-based equity sell-off, investors are becoming more discerning about the sustainability of AI-driven business models.

ECB President Lagarde appeared to downplay the role of the exchange rate in the policy outlook, though our economists see it as a lingering vulnerability in the ECB’s “good place” narrative. In the near term, tail risks remain skewed toward further easing, even as the threshold for a rate cut stays high. Markets are currently pricing roughly a 25% chance of a cut later this year, which we view as reasonable. This pricing keeps the front end of the euro curve well anchored, implying that any further deterioration in global risk sentiment—stemming from outside the euro area—would likely continue to flatten the curve. That said, a concurrent strengthening of the euro would complicate the curve dynamics.

A dovish BoE fails to outweigh mounting political risks

Markets reacted far more strongly to the Bank of England meeting than to the ECB, with a March rate cut rapidly becoming the base-case scenario. The BoE’s relatively sparse inter-meeting communication means that policy surprises tend to generate outsized moves, and this meeting delivered just that. The 2-year swap rate dropped around 7bp as the outcome proved more dovish than markets had anticipated. We are broadly aligned with the revised pricing and see considerable scope for easing as inflation continues to soften. Governor Bailey appeared to endorse this view, later remarking that current market pricing for a March cut was “not a bad place to be.”

Attention now shifts to the long end of the curve, where political risks may continue to exert upward pressure on 30-year gilt yields. Unlike the front end, the 30-year yield actually rose by roughly 3bp on Thursday despite the BoE’s dovish pivot. Political uncertainty—particularly around Starmer’s position as prime minister—adds to doubts over the future fiscal trajectory. Ahead of November’s budget, we had estimated the 10-year gilt risk premium at around 25bp, underscoring investor sensitivity to the UK’s fiscal outlook. Against this backdrop, we see limited scope for 10-year GBP rates to move meaningfully lower in the near term.

Friday: Key Events and Market Outlook

Softer US labor indicators weighed on risk sentiment on Thursday. While Friday does not bring the official jobs report, attention will turn to the preliminary University of Michigan consumer sentiment index. Consensus expectations point to a weaker reading, but any sharper-than-anticipated deterioration would likely amplify existing market unease. Consumer credit data, also due on Friday, will be another point of focus.

In the euro area, the ECB will publish its Survey of Professional Forecasters. Following the ECB meeting, markets will also listen closely to remarks from ECB officials, with Kocher and Cipollone scheduled to speak. Elsewhere, BoE Chief Economist Huw Pill is also on the agenda.

On the supply side, government issuance is limited, with the only primary market activity being a €0.5bn Belgian ORI auction.

Sources: Padhraic Garvey