Nvidia’s (NASDAQ: NVDA) $78bn revenue projection would once have sparked a broad rally in global equities. This time, investors paused.

The stock initially slipped before edging slightly higher in post-market trading. In this stage of the AI cycle, rapid expansion alone is no longer enough to impress the market.

Over the past two years, artificial intelligence exposure commanded a premium almost regardless of valuation. Capital flowed aggressively into the AI infrastructure layer, with Nvidia at the epicentre. Its chips became foundational to hyperscale data centres, sovereign digital strategies, and enterprise AI rollouts. Valuations climbed on expectations of sustained, exponential demand. Now, scrutiny has intensified.

A $78bn forecast confirms demand remains robust—but it also suggests expectations were already set near perfection. Markets are no longer rewarding size alone; they are evaluating the durability, quality, and profitability behind that growth.

Investors are calling for tighter operating discipline. They want clearer visibility on margins, pricing strength, and forward orders. Strong revenue growth does not automatically guarantee lasting shareholder returns when valuations assume near-flawless execution.

Nvidia’s competitive position remains strong. It continues to underpin the AI infrastructure ecosystem. Hyperscale cloud providers are spending aggressively, governments are advancing sovereign AI ambitions, and enterprise adoption is accelerating. The structural tailwinds remain intact.

What has changed is the market’s tolerance for uncertainty. Premium valuations now demand premium predictability—stable gross margins, resilient pricing power, and a more diversified revenue mix.

Markets are likely to scrutinise customer concentration, especially reliance on a limited group of hyperscale clients. They will question whether current capital expenditure by major cloud operators marks a cyclical high or the start of a sustained multi-year investment cycle.

Any indication that AI-driven capex is plateauing rather than accelerating could trigger disproportionate market reactions. Competitive pressures are also building. As large cloud providers ramp up in-house chip development, investors will increasingly assess how defensible Nvidia’s ecosystem remains amid the rise of alternative silicon architectures.

This shift does not negate the AI revolution — it sharpens its contours.

The implications stretch far beyond a single company. Semiconductor peers, advanced memory manufacturers, data-centre infrastructure providers and AI-centric software firms have largely traded in tandem with Nvidia’s rally. A more discerning market is now separating businesses that translate AI adoption into concrete earnings from those still priced primarily on long-term potential.

Dispersion within AI equities is likely to widen over the coming year. Infrastructure leaders with strong cash flow and resilient balance sheets may continue to attract support. By contrast, application-layer companies that have yet to prove sustainable monetisation could face heightened volatility.

Institutional investors are applying greater discipline to their assumptions. Portfolio managers who heavily overweighted AI leaders during the initial surge are revisiting long-term growth trajectories beyond peak deployment phases. Scenarios in which hyperscale spending moderates into 2027 are increasingly part of valuation models, with capital intensity and return on invested capital under renewed scrutiny.

AI companies are being assessed more like established enterprises than early-stage disruptors. Market psychology has matured.

For Nvidia, this phase could ultimately reinforce its leadership if operational execution remains strong. Consistent free cash flow, ongoing innovation cycles and deep integration across the AI value chain offer structural advantages. However, expectations have risen materially. Earnings announcements may drive sharper volatility as the scope for positive surprise narrows.

Markets are transitioning from thematic enthusiasm to detailed financial examination. Compelling narratives must now be backed by measurable precision.

The AI expansion is tangible. The capital investment is tangible. The demand is tangible. But investors are no longer rewarding mere participation in the theme — they are rewarding disciplined growth, sustainable margins and transparent capital deployment.

Nvidia’s $78bn revenue outlook affirms that large-scale AI expansion continues. The subdued market response underscores a parallel reality: momentum alone is insufficient to justify elevated valuations.

The next stage of the AI cycle will favour companies capable of turning market leadership into reliable profitability. Those that fall short may discover that even strong revenue growth offers limited insulation when expectations are already stretched.

Futures tied to the main U.S. stock benchmarks edged lower as investors focused on key earnings from the technology sector. Nvidia, a heavyweight in the U.S. equity market, delivered stronger-than-expected results, though investors are seeking clearer guidance on when its substantial cash flow will translate into greater shareholder returns. Salesforce shares declined after issuing a softer revenue outlook. Meanwhile, oil prices held steady ahead of crucial nuclear negotiations between U.S. and Iranian officials.

Futures Edge Lower

U.S. equity futures moved down Thursday as markets digested earnings from AI leader Nvidia.

As of 03:05 ET (08:05 GMT), Dow futures were down 122 points, or 0.3%, S&P 500 futures slipped 0.1%, and Nasdaq 100 futures also fell 0.1%. This followed gains across all major Wall Street indices in the previous session, when investors positioned ahead of Nvidia’s earnings release.

Sentiment had improved on renewed optimism surrounding artificial intelligence, marking another shift in what has been a volatile narrative around the emerging technology. The Nasdaq led prior gains as investors regained confidence that AI could eventually deliver broad economic benefits — contrasting with earlier concerns that new AI models might disrupt software firms and limit returns on heavy data center spending.

Remarks from Richmond Fed President Tom Barkin also supported equities, as he noted uncertainty over whether automation would significantly raise unemployment and suggested AI could instead improve labor market efficiency.

Nvidia Little Changed Despite Strong Results

Nvidia reported better-than-expected earnings for the January quarter and issued revenue guidance above forecasts for the current period, yet its shares were mostly flat in after-hours trading.

Some investors questioned whether the chipmaker is returning sufficient capital to shareholders. Yvette Schmitter, CEO of Fusion Collective, pointed out that while Nvidia generated $35 billion in cash during the fourth quarter, it returned just 12% to shareholders — sharply lower than 52% a year earlier.

She also raised concerns about reduced buybacks despite record cash generation, especially as Nvidia highlights strong demand for its sold-out Ampere chips.

These concerns echoed questions raised during the company’s earnings call, including from a UBS analyst who asked whether Nvidia plans to distribute more of the anticipated $100 billion in cash expected this year. CFO Colette Kress emphasized ongoing investment in the broader AI ecosystem, while CEO Jensen Huang underscored AI’s foundational role in the future of computing.

Salesforce Drops on Soft Revenue Outlook

Salesforce shares fell in extended trading after the company issued fiscal 2027 revenue guidance below Wall Street expectations, suggesting softer demand for enterprise software amid economic uncertainty and tighter corporate budgets.

The company projected full-year revenue between $45.80 billion and $46.20 billion, slightly below consensus estimates at the midpoint.

Salesforce continues to invest heavily in artificial intelligence to counter investor concerns that emerging AI models, such as those developed by startups like Anthropic, could erode demand. These pressures have contributed to stock volatility as the company works to defend its position within the software-as-a-service industry.

However, Salesforce raised its fiscal 2030 revenue forecast to $63 billion from $60 billion, citing expected growth from agentic AI offerings. Analysts at Vital Knowledge described the report as not flawless but “good enough,” highlighting strong AI product momentum, stable core performance, and solid cash flow generation.

Oil Steady Before U.S.- Iran Talks

Oil prices were largely unchanged Thursday, remaining near seven-month highs as markets prepared for a third round of nuclear discussions between Washington and Tehran.

Brent crude gained 0.2% to $70.84 per barrel, while U.S. West Texas Intermediate rose 0.2% to $65.62 per barrel.

U.S. representatives, including special envoy Steve Witkoff and adviser Jared Kushner, are scheduled to meet Iranian officials in Geneva as negotiations continue over Iran’s nuclear program. President Donald Trump has warned that failure to make meaningful progress could lead to serious consequences, raising concerns that prolonged tensions may disrupt supply from Iran, a key OPEC producer.

Gold Edges Higher

Gold prices ticked up as uncertainty surrounding U.S. trade tariffs bolstered safe-haven demand, with investors also monitoring developments in the U.S.-Iran nuclear talks.

Spot gold rose 0.6% to $5,196.55 per ounce, while U.S. gold futures dipped 0.5% to $5,200.54 per ounce.

Markets are also evaluating the implications of newly announced U.S. tariffs following a Supreme Court ruling that struck down President Trump’s sweeping reciprocal tariff measures. Attention now turns to upcoming U.S. economic data, including weekly jobless claims. So far this year, gold has remained supported by geopolitical tensions, central bank buying, and portfolio diversification trends.

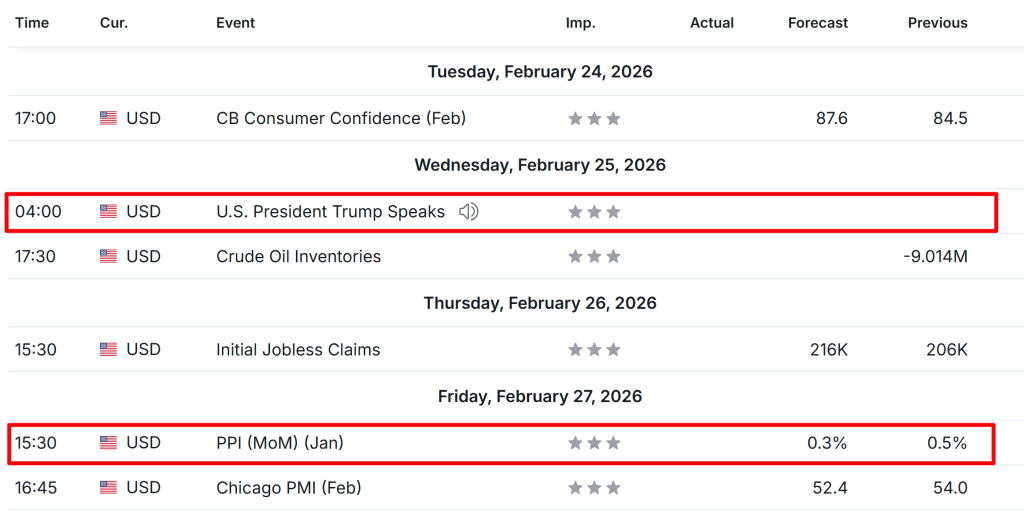

U.S. PPI inflation data and Nvidia’s earnings will take center stage in the coming week.

Nvidia appears set to post another standout quarter.

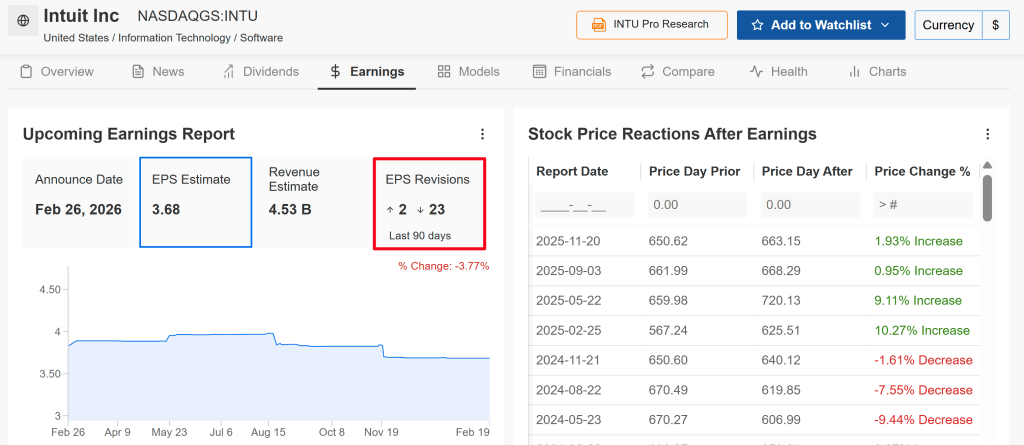

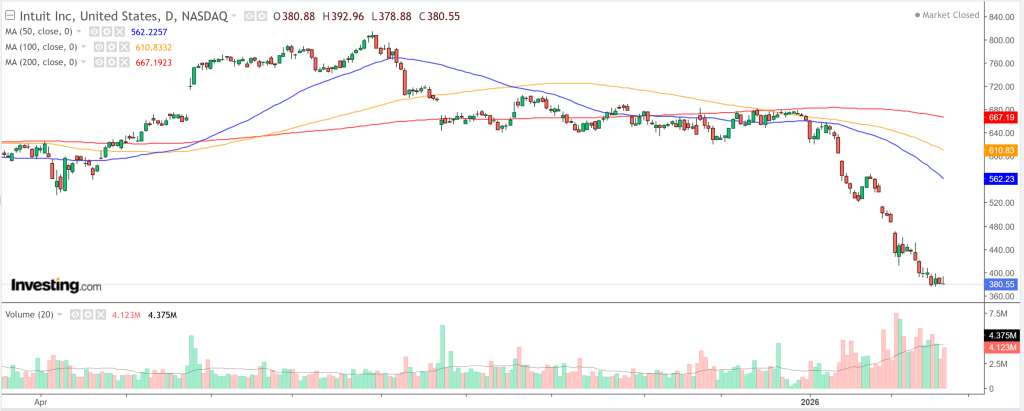

Meanwhile, Intuit is confronting mounting fundamental and technical pressures ahead of its results.

U.S. equities closed higher on Friday after the Supreme Court invalidated President Donald Trump’s tariffs. Trump criticized the decision as a “disgrace” and said in a Truth Social post on Saturday that he would introduce a new 15% global tariff, just one day after announcing a 10% levy.

After Friday’s gains, the 30-stock Dow Jones Industrial Average finished the week up about 0.3%. The S&P 500 advanced 1.1%, while the tech-heavy Nasdaq Composite broke a five-week slide with a 1.5% surge. The small-cap Russell 2000 added nearly 0.7%.

Markets may see heightened swings in the days ahead as investors weigh prospects for growth, inflation, interest rates, and corporate earnings against a backdrop of renewed trade frictions.

With a relatively light economic calendar, attention will center on Friday’s January U.S. producer price index report. As of Sunday morning, traders are pricing in slightly better than even odds that the Federal Reserve will lower rates by its June meeting.

On the earnings front, Nvidia’s (NASDAQ: NVDA) report will headline the week as the season winds down. Beyond Nvidia, investors will be tracking several major tech names, particularly software companies facing pressure from concerns that AI could disrupt their core businesses, including Salesforce (NYSE: CRM), Intuit (NASDAQ: INTU), Snowflake (NYSE: SNOW), Zscaler (NASDAQ: ZS), and Zoom Video Communications (NASDAQ: ZM).

AI infrastructure providers Dell Technologies (NYSE: DELL) and CoreWeave (NASDAQ: CRWV) are also set to post results. Outside the tech space, prominent retailers such as Home Depot (NYSE: HD), Lowe’s Companies (NYSE: LOW), and TJX Companies (NYSE: TJX) are scheduled to report.

At the same time, markets will be parsing President Trump’s State of the Union address on Tuesday and monitoring any developments involving the U.S. and Iran.

No matter which way markets move, below I outline one stock that could attract buying interest and another that may face renewed downside pressure. Keep in mind, this outlook covers only the week ahead—Monday, February 23 through Friday, February 27.

Stock to Buy: Nvidia

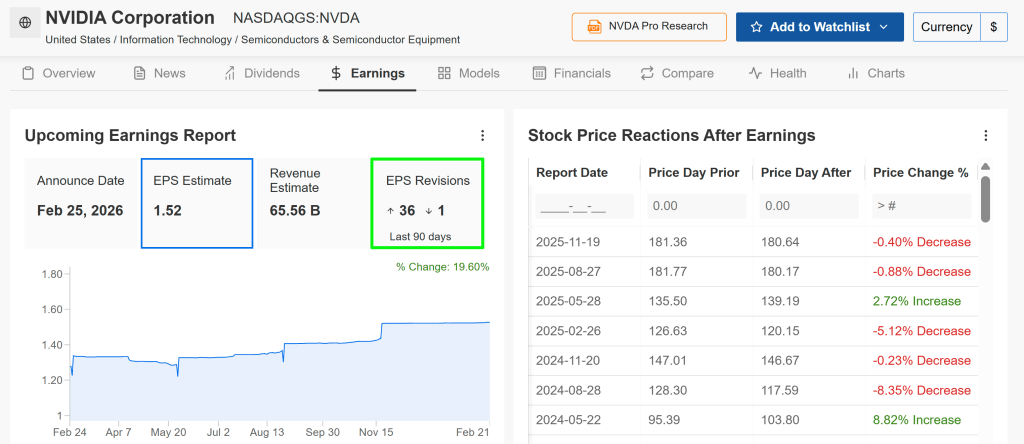

Nvidia heads into its earnings report with analysts anticipating another “beat-and-raise” performance, fueled by robust demand for AI infrastructure. Fourth-quarter results are scheduled for release after Wednesday’s market close at 4:20 p.m. ET, followed by a 5:00 p.m. ET conference call with CEO Jensen Huang.

According to an InvestingPro survey, profit forecasts have been lifted 36 times in recent weeks, compared with just one downward revision—highlighting growing optimism around Nvidia’s earnings outlook. In the options market, traders are pricing in a potential move of roughly ±6% in NVDA shares following the announcement.

Wall Street expects the AI powerhouse to deliver earnings of $1.52 per share, up 71% from a year earlier. Revenue is forecast to climb 67% to $65.6 billion, underscoring the company’s ongoing strength in the AI chip space.

Citi recently suggested that January-quarter revenue could exceed $67 billion, with projections pointing to even stronger results in the April quarter.

Another solid showing in data-center sales, along with widening margins and healthy free cash flow, would bolster the view that Nvidia remains firmly in the midst—not at the tail end—of an AI supercycle.

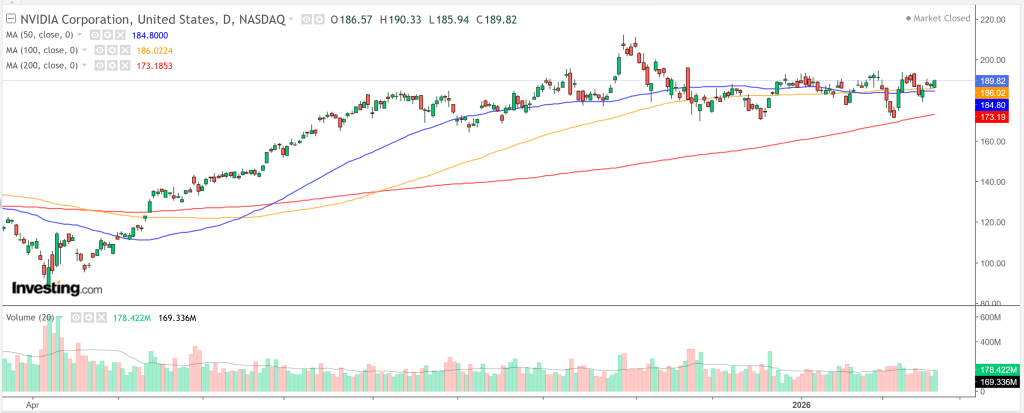

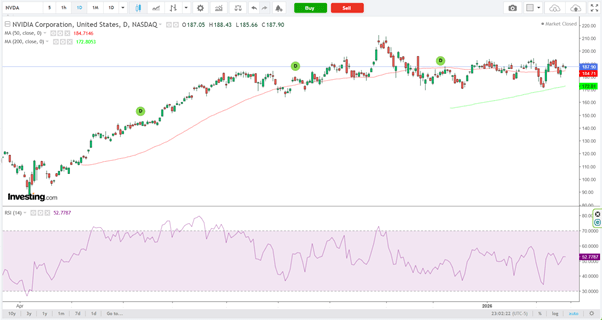

NVDA shares ended Friday at $189.82, consolidating after a strong advance but still positioned to move higher on favorable catalysts. Across multiple timeframes—from intraday charts to the monthly view—technical indicators and moving averages continue to signal a “strong buy.”

A beat-and-raise report could ignite another leg up, particularly if management emphasizes longer-term visibility into 2026–2027 growth driven by next-generation architectures such as Rubin.

Trade Setup:

Entry: Near current levels (around $190)

Target: $210 (approximately 10% upside)

Stop-Loss: $184 (roughly 3.5% downside risk)

Stock to Sell: Intuit

Intuit—the parent company of TurboTax, QuickBooks, Credit Karma, and Mailchimp—heads into earnings week facing mounting pressure. Concerns have escalated in early 2026 that generative AI tools could weaken its competitive moat across tax prep, accounting, and financial software by enabling free or lower-cost alternatives, custom AI agents, or in-house solutions for small businesses and consumers.

This anxiety has fueled broader “SaaSpocalypse” sentiment, with the software sector shedding trillions in market value. INTU shares have been particularly hard hit in recent months, sliding sharply alongside peers such as Salesforce.

Analyst sentiment has also turned more cautious ahead of the report, with 23 of the last 25 estimate revisions moving lower—signaling growing skepticism around near-term performance.

Wall Street expects Intuit to post earnings of $3.68 per share, up roughly 11% year over year, on revenue of about $4.5 billion. The bigger concern, however, centers less on the headline numbers and more on the narrative surrounding AI-driven disruption.

Although Intuit has made significant investments in artificial intelligence, investors seem to view these efforts as largely defensive—designed to protect its existing franchises rather than meaningfully expand them or counter broader competitive threats. TD Cowen recently cut its price target, pointing to doubts about the strength of Intuit’s AI strategy and intensifying competition.

Any remarks about rising competitive pressures, decelerating growth in key segments, or conservative forward guidance could amplify downside risks—particularly in a stock that may be technically oversold but remains vulnerable in a sentiment-driven market.

Shares of Intuit have fallen 42.5% over the past three months and are now hovering just above their 52-week low of $375.40. Technical signals remain decisively negative: across timeframes—from hourly charts to the monthly view—both moving averages and momentum indicators continue to flash “strong sell.”

With management’s outlook likely to face intense scrutiny, any earnings miss or cautious commentary reflecting a more competitive, AI-driven environment could deepen the selloff.

The artificial intelligence trade faces its biggest test of the year this week as three cornerstone companies in the AI infrastructure ecosystem prepare to deliver quarterly earnings. With tech stocks showing signs of fatigue, investors want more than simple earnings beats. They’re looking for proof that heavy capital expenditure is translating into the successful deployment of next-generation hardware. All attention will turn to the after-market close (AMC) on Wednesday and Thursday to see whether the AI rally still has momentum.

NVIDIA: The undisputed AI infrastructure leader

NVIDIA (NVDA) is set to report fiscal Q4 2026 results on Wednesday, Feb. 25, after market close. As the dominant supplier of GPUs powering large language models, NVIDIA remains the clearest gauge of the AI trade’s health. Wall Street is anticipating a “beat and raise,” with consensus revenue estimates around $65.6 billion — an impressive 67% year-over-year increase.

Investors are especially focused on the production ramp of its Blackwell architecture chips. Any updates on supply chain constraints or the development timeline for the upcoming Rubin platform could influence not only tech stocks but the broader S&P 500. Options markets imply a potential 6.5% swing in either direction, making NVIDIA’s earnings the week’s must-watch event for global investors.

Hardware and cloud players: CoreWeave and Dell under the spotlight

On Thursday, Feb. 26, AMC, attention shifts to the physical backbone of AI infrastructure. CoreWeave (CRWV), a specialized cloud provider and key NVIDIA partner, will report against high expectations driven by its sizable revenue backlog. Analysts project Q4 revenue of roughly $1.53 billion, but the more significant figure is its $56 billion backlog — a forward-looking signal of how much computing capacity AI firms and tech giants are securing

Also reporting Thursday is Dell Technologies (DELL), which has repositioned itself as a major supplier of AI-optimized servers. Consensus forecasts call for earnings of $3.53 per share on $31.6 billion in revenue. Dell recently earned a spot on Evercore’s “Tactical Outperform” list, supported by a sharp rise in AI server orders and an $18.4 billion backlog exiting last quarter. The key question for Dell will be whether it can preserve margins while rapidly scaling production to meet surging demand for AI infrastructure.

After a powerful rally in large-cap technology shares, investors are once again asking whether smart money is beginning to rotate.

With AI enthusiasm pushing tech valuations higher and energy names still trading at comparatively modest multiples, there are early signs that capital flows may be shifting beneath the surface. Here’s a closer look at the current landscape — and where institutional positioning may be headed.

The Case for Tech: Structural Growth Still Intact

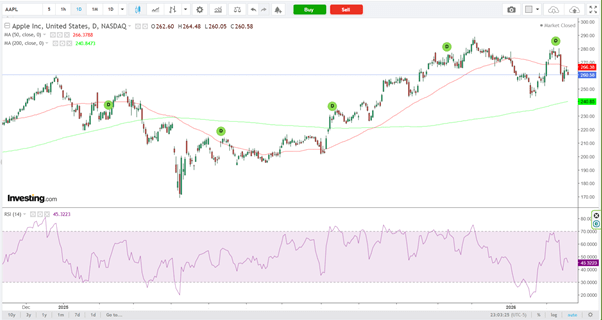

Companies such as Nvidia (NASDAQ: NVDA), Microsoft (NASDAQ: MSFT), and Apple (NASDAQ: AAPL) remain central pillars of institutional portfolios.

Technology continues to lead in earnings expansion, fueled by AI infrastructure investment, cloud migration, and ongoing software monetization.

Why capital is still favoring tech:

Revenue growth outpacing the broader market

High operating margins and robust free cash flow

Sustained AI-driven capex cycles

Strong balance sheets with significant liquidity

Mega-cap tech remains a structural core holding for institutional investors. Even during brief pullbacks, dip-buying has been persistent — a sign that long-term conviction in the sector remains strong.

That said, valuations in select segments have stretched beyond historical norms. If earnings momentum moderates, the probability of sector rotation increases, particularly as investors reassess risk-reward at elevated multiples.

The Case for Energy: Undervalued and Cash-Generative

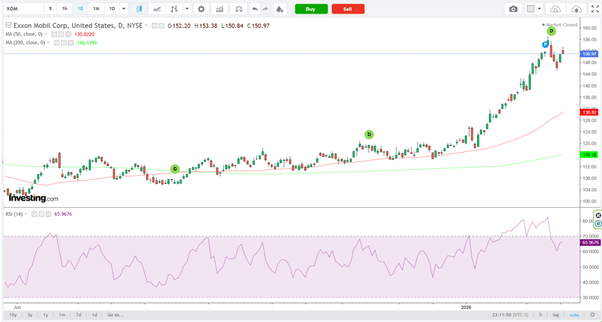

Integrated majors such as Exxon Mobil (NYSE: XOM) and Chevron (NYSE: CVX) are drawing renewed attention as investors reassess sector allocations.

Energy equities typically trade in cycles influenced by crude prices, global demand dynamics, and geopolitical developments. After extended periods of relative underperformance, the sector often becomes a magnet for value-oriented capital.

Why institutional money may rotate toward energy:

Lower forward P/E multiples compared to technology

Strong and visible free cash flow generation

Dividend yields frequently above the broader market average

Ongoing share repurchase programs

If crude prices remain stable or trend higher, integrated oil majors can produce substantial cash flows, offering a mix of income, capital return, and relative defensiveness.

In an environment where parts of the technology sector appear valuation-stretched, energy provides a compelling contrast on both multiples and yield.

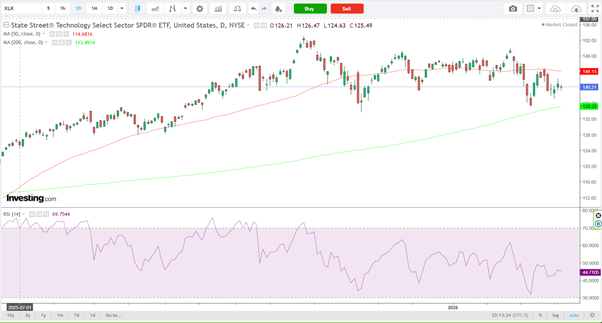

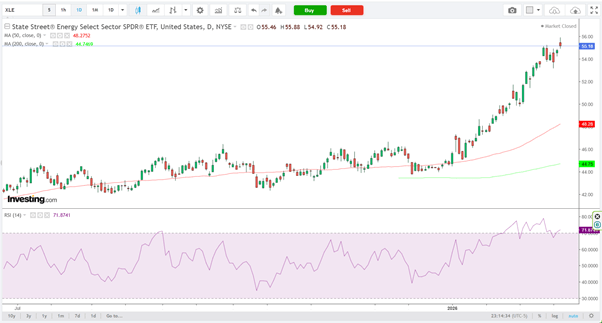

Sector ETF Signals: Tracking Institutional Flows

Sector ETFs can offer valuable insight into how institutional capital is rotating beneath the surface. Two key vehicles to monitor are the Technology Select Sector SPDR Fund (NYSE: XLK) and the Energy Select Sector SPDR Fund (NYSE: XLE).

ETF performance and fund flow data often act as real-time indicators of positioning shifts:

If XLK continues to outperform, it suggests growth leadership remains firmly in place.

If XLE begins to show sustained relative strength versus XLK, it may signal that rotation into energy is gaining traction.

Historically, sector leadership transitions tend to coincide with:

Shifts in interest rate expectations

Narrowing earnings growth differentials

Sharp moves in commodity prices

Monitoring the relative strength ratio between XLE and XLK can provide early confirmation of whether capital is merely rebalancing tactically — or whether a broader structural rotation is unfolding.

Macro Forces Driving Sector Rotation

1. Interest Rates Elevated yields tend to weigh more heavily on high-multiple technology stocks, as future cash flows are discounted at higher rates. In contrast, energy companies—often valued on nearer-term cash generation—can prove more resilient. If bond yields move higher, defensive value sectors may attract incremental capital at the expense of growth.

2. Commodity Prices Oil prices remain a primary earnings driver for energy producers. A sustained rally in crude can rapidly alter sector performance dynamics, drawing capital into integrated majors and upstream names as profit expectations improve.

3. Earnings Revisions Institutional allocation models closely track forward earnings revisions. If analyst upgrades begin to slow in technology while turning more constructive for energy, portfolio rebalancing flows may follow.

4. Risk Appetite Technology typically outperforms in strong risk-on environments characterized by abundant liquidity and growth optimism. Energy, by contrast, can gain relative strength during inflationary phases or periods of geopolitical tension, when commodity exposure and cash yield become more attractive.

What Institutional Capital Is Likely Doing Now

Rather than making an outright “either/or” shift, institutional investors typically adjust exposure more subtly. That can mean trimming extended technology positions, selectively adding energy holdings, or rotating within sectors—such as moving from mega-cap AI leaders into second-tier beneficiaries of the theme.

The real driver is relative earnings momentum, not headlines.

Which Sector Offers More Upside?

Tech Upside Scenario

Continued acceleration in AI-related spending

Consistent earnings beats from mega-cap leaders

Declining bond yields that support higher valuation multiples

Energy Upside Scenario

Oil prices establish a sustained uptrend

Inflation concerns re-emerge

Technology valuations compress

In the near term, technology remains the structural growth narrative, supported by AI infrastructure, cloud expansion, and software monetization. However, energy presents potential asymmetric upside if commodity dynamics shift in its favor.

Sector rotation is rarely abrupt. More often, it unfolds gradually through portfolio rebalancing rather than wholesale liquidation.

While tech continues to dominate leadership, energy’s relative valuation discount and strong cash generation could attract incremental capital if macro conditions evolve.

Key indicators to monitor:

Relative strength between the Energy Select Sector SPDR Fund and the Technology Select Sector SPDR Fund

Forward earnings revisions

Oil price trends

Bond yield movements

The critical question is not whether rotation will occur — but whether it is already quietly underway beneath the surface.

Google plans to increase capital expenditures to as much as $185 billion this year, significantly exceeding market expectations of around $120 billion. Robust growth in search advertising and Google Cloud has provided Alphabet with the financial flexibility to pursue this aggressive investment strategy. According to Morgan Stanley analysts, the sharp rise in spending signals that AI is driving higher engagement and improved monetisation across Google’s core businesses, with search revenue climbing 17% and cloud revenue surging 48% in the most recent quarter.

Meta conveyed a similar message after projecting annual capital expenditures of $135 billion, supported by evidence that AI is enhancing advertising effectiveness. However, not all technology giants have been able to convince investors that rising capital spending is justified. Microsoft, for example, saw its shares fall sharply—erasing more than $350 billion in market value—after its cloud performance disappointed, even as its own capital investment ramped up.

Amazon is also under pressure to sustain strong growth at AWS while continuing to expand data-center capacity. In contrast, Alphabet’s sharply rising cloud backlog highlights growing demand for AI infrastructure and tools, lending credibility to its aggressive spending plans.

The trade-off, however, is immediate. Morgan Stanley estimates that Alphabet’s free cash flow per share could decline by 58% in 2026 and by as much as 80% in 2027 as higher capital expenditures flow through the business. In effect, the company is sacrificing near-term cash returns in exchange for longer-term strategic positioning.

Alphabet now stands at a crossroads. Strong advertising and cloud growth point to early benefits from AI investments, but the sheer scale of spending increases execution risk. If the added capacity delivers sustained revenue growth, the strategy will appear well-timed. If growth slows, Alphabet could face a thinner cash buffer and heightened expectations. For now, the company is betting that leading with investment is essential to staying ahead—and the market will be watching closely to see whether returns keep pace.

Stifel downgrades Microsoft to Hold, says it’s “time to pause”

Microsoft (NASDAQ: MSFT) saw a rare Wall Street downgrade this week as Stifel analyst Brad Reback lowered the stock to Hold from Buy, cautioning that expectations for fiscal and calendar 2027 appear overly optimistic. He cited ongoing cloud capacity constraints, rising capital intensity, and intensifying AI competition as key concerns.

Reback cut Stifel’s price target to $392 from $540, saying the stock may need a breather after its strong run. Persistent limitations in Azure capacity remain a major headwind. Given well-known supply issues, along with strong results from Google’s GCP and Gemini platforms and increasing momentum at Anthropic, Reback believes meaningful near-term acceleration at Azure is unlikely.

He also noted that revenue tailwinds from overlapping product cycles that benefited fiscal 2026 should fade, limiting upside in subsequent years. Meanwhile, investment spending is expected to surge. Stifel raised its fiscal 2027 capex estimate to roughly $200 billion, about 40% growth and well above the Street’s $160 billion forecast. As a result, Reback lowered his FY27 gross margin outlook to around 63%, versus a consensus near 67%.

Operationally, Microsoft is entering what Reback described as a new — though still efficient — phase of elevated spending as it builds and monetizes proprietary AI platforms, a shift likely to weigh on operating margin leverage. While Stifel remains positive on Microsoft’s long-term strategic position, Reback said near-term visibility has become less clear, arguing the stock is unlikely to re-rate until capital spending moderates relative to Azure growth or cloud demand reaccelerates meaningfully.

DA Davidson cuts Amazon as AWS cedes cloud leadership

DA Davidson downgraded Amazon (NASDAQ: AMZN) to Neutral from Buy, warning that the company is losing its leadership position in cloud computing and showing early strategic strain in an AI-driven retail landscape. The firm lowered its price target to $175, arguing Amazon is now playing catch-up through increasingly aggressive investment.

Analyst Gil Luria said AWS continues to trail Microsoft Azure and Google Cloud. While AWS posted 24% year-over-year growth, Google Cloud accelerated to 48%, and Azure grew 39% despite capacity constraints. Luria highlighted Amazon’s lack of a frontier AI research lab and the absence of a flagship partnership like Microsoft’s alliance with OpenAI as factors driving customer preference toward rivals.

Falling behind, he warned, is forcing Amazon into heavier spending, pointing to more than $200 billion in projected capex. Luria suggested Amazon may ultimately need to pursue a $50 billion OpenAI investment to remain competitive in frontier AI models. He also raised concerns that Amazon’s retail business could face a structural disadvantage in a chat-centric internet dominated by Gemini and ChatGPT, where merchants embedded directly in leading AI platforms may gain superior traffic and advertising leverage.

Wolfe sees massive long-term upside in Tesla robotaxis, but near-term pressure

Wolfe Research said Tesla’s (NASDAQ: TSLA) robotaxi platform could become a major long-term growth engine, estimating the business could scale to $250 billion in annual revenue by 2035 as autonomous adoption expands. Analyst Emmanuel Rosner described 2026 as a catalyst-heavy year, with investor focus on robotaxi rollout, Optimus production, and the launch of unsupervised full self-driving.

Wolfe’s model assumes 30% autonomous penetration, a 50% market share for Tesla, and pricing of $1 per mile, which could support roughly $2.75 trillion in equity value, or about $900 billion on a discounted basis. Additional upside could come from Optimus and FSD licensing.

Despite the long-term optimism, Rosner remains cautious on near-term fundamentals, sitting below consensus earnings estimates for 2026 and 2027. He expects margin pressure from higher costs, pricing dynamics, and changes in FSD monetization, along with heavy AI-related investment weighing on earnings. Still, strong momentum in Tesla’s energy storage business provides some offset, and Wolfe remains tactically constructive given the steady flow of upcoming catalysts.

Truist tells investors to “buy the dip” in AMD

Truist Securities reiterated a bullish long-term view on AMD (NASDAQ: AMD), urging investors to buy the weakness after the stock fell more than 14% over the past week to its lowest level since October 2025. Analyst William Stein said AMD continues to compound earnings at roughly a 45% CAGR through 2030, while trading at just 11x estimated 2030 EPS.

Although fourth-quarter results benefited from a one-off China-related dynamic, AMD still reaffirmed its outlook for 60% data-center growth and 35% overall sales growth, which management believes could drive more than $20 in EPS by 2030. Stein cited strong customer engagement, accelerating adoption of Instinct MI350 GPUs, and solid demand for fifth-generation EPYC processors as key drivers. Truist raised its 2027 EPS forecast and lifted its price target to $283, arguing long-term fundamentals outweigh short-term noise.

Jefferies warns Palantir valuation still has room to fall

Jefferies said Palantir Technologies (NASDAQ: PLTR) remains vulnerable to further downside despite a steep year-to-date decline of roughly 27%. Analyst Brent Thill emphasized that the call is based on valuation rather than fundamentals, noting that even after compressing from 73x to about 31x forward revenue, Palantir still trades at nearly double the valuation of other large-cap software peers.

While acknowledging improving fundamentals, expanding addressable markets, and strengthening competitive positioning, Thill argued that valuation risk outweighs operational progress. The stock’s premium leaves it highly sensitive to shifts in AI sentiment and broader software sector trends. Jefferies believes cooling enthusiasm could push Palantir toward more sustainable valuation levels, reiterating its Underperform rating and $70 price target, even after strong quarterly results failed to justify the stock’s elevated multiple.

Uncertainty surrounding AI is driving market volatility on several fronts. Beyond accelerating layoffs as AI replaces certain roles, software stocks continue to sell off amid concerns that rapid AI deployment threatens all but companies with strong client-relationship moats. At the same time, surging demand for large-scale data centers has boosted memory chipmakers, while early winners in other semiconductor segments are now facing valuation pressure. Meanwhile, advances in quantum computing are gaining traction and could fundamentally reshape the landscape if fully realized—particularly in the area of security, where quantum systems are widely viewed as capable of breaking existing encryption methods, including those used in blockchain technology. Despite the turbulence, the longer-term outlook still points toward meaningful gains in labor productivity and improved corporate profit margins.

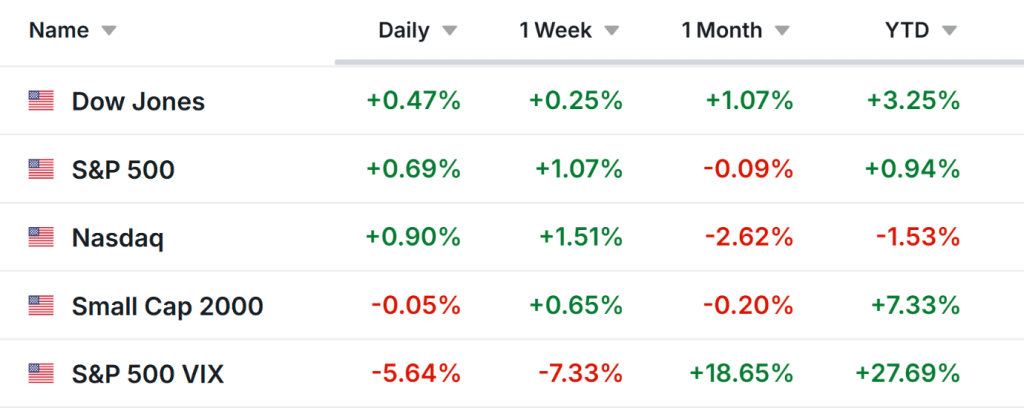

This morning, the Dow Jones Industrial Average and the equal-weighted S&P 500 are the only major indexes trading in positive territory. Both the NASDAQ and the “Magnificent Seven” are now negative year to date. While the S&P 500 is up 0.9% YTD, the equal-weighted S&P has gained 4.6%, highlighting the underperformance of mega-cap technology stocks. The Dow is up 3.2%, and the Russell 2000 continues to lead with a 6.3% gain YTD, despite a 0.5% decline over the past week. Market volatility remains elevated, with the VIX jumping to 19.1 at the open from 18 previously and currently holding near 18.8.

Sector performance year to date shows Financial Services (-2.3%), Technology (-1.3%), and Healthcare (-0.5%) as the only groups in negative territory. In contrast, Energy (+15.6%), Basic Materials (+11.8%), and Consumer Staples (+10.5%) are posting double-digit gains.

Interest rates are little changed, with the U.S. 2-year Treasury yield at 3.57% and the 10-year at 4.27%. International yields are similarly flat. The U.S. dollar index is higher by 0.25 at 97.55, up 1.3% over the past week.

Precious metals are experiencing sharp swings today, with gold climbing as high as $5,113 per ounce before retreating to $4,939, while silver fell from $92.0 to $86.5 per ounce. Copper prices declined 2.7% to $5.92 per ounce. Energy markets are relatively quiet, with crude oil trading flat near $63.20 per barrel.

Cryptocurrencies continue to weaken, as Bitcoin has fallen 3.7% to $73.9K and is now down 26.4% over the last twelve months. Ethereum is lower by 4.2% and down 31% LTM. Even with the prospect of clearer regulation, many investors remain cautious given the sector’s persistent volatility.

On the earnings front, AMD delivered solid top- and bottom-line beats, but weaker-than-expected data center revenue and rising costs weighed heavily on the stock. Shares are down a sharp 15.9%—their worst session in years—bringing performance to -4.9% YTD, though still up 70.4% LTM, and sending ripples through the broader hardware space. The semiconductor sector is down 3.9% on the day, including a 3.1% decline in NVIDIA. In contrast, Eli Lilly posted a strong earnings beat, exceeded expectations on both revenue and profit, and raised guidance. Its shares are up 9.8%, now +2.6% YTD and +33.7% LTM. Investors are also looking ahead to Alphabet’s results tonight and Amazon’s tomorrow.

As trading continues, the Dow Jones Industrial Average and the equal-weighted S&P 500 are holding onto gains, while the NASDAQ has slid more than 1% and the Magnificent Seven is down 0.9%. The S&P 500 has dipped below 6,900, off 0.3%, and the Russell 2000 is down 0.8%. The ongoing pullback in technology stocks reflects elevated valuations and persistently high interest rates. Even so, the Dow and the equal-weighted S&P remain near record highs, the broader trend is still positive, and a rebound in tech following this correction would not be unexpected.

Tech just suffered a selloff of a different kind. This was not about rates, recession fears, or a routine earnings disappointment. It was the market catching its own reflection in the AI mirror—and flinching.

When confidence cracks, the Nasdaq does not rotate. It drops the floor. The S&P followed along, dutifully diversified in theory, while tech still steers the wheel.

The trigger was AMD, but the message was broader. In a fully priced bull market, “good” results are not good enough when investors have already paid in advance for perfection. When expectations stretch into the stratosphere, even a strong quarter feels like a letdown. AMD was not punished for weakness—it was punished for failing to deliver magic commensurate with the valuation it carried.

What followed was less about fundamentals than positioning. This was the market unwinding a narrative that had become too tidy, too crowded, too self-assured. When everyone leans the same way, even a minor wobble turns into a shove.

And the shove traveled fast. Once the story lost its grip, selling turned indiscriminate. Yesterday’s AI champions were treated like stale trades. Hardware names sank alongside software darlings. Picks, shovels, and miners all landed in the same risk bucket as investors dumped exposure wholesale.

This was never just a chip story. The real fault line runs through software—and it is psychological. The market is now entertaining a new fear: not that AI lifts all boats, but that it punctures the hulls of those that assumed they were unsinkable.

Software cracked first because belief ran deepest there. It was the cleanest narrative in the market—AI as a quiet margin expander, a tailwind that boosted earnings without disrupting the underlying structure. That assumption is now being dismantled in real time.

The uncomfortable inversion is coming into focus. The companies that digitized the fastest may also be the most exposed. AI is not arriving as a polite consultant. It is entering as a tireless shadow workforce—one that never negotiates, never sleeps, and learns faster than corporate hierarchies can adapt. And it writes code, too.

That is why this moment feels like a break, not a revision. When markets stop debating how much something earns and start questioning why it exists, prices do not drift lower. They fracture.

You can see it in the tape. This is not a careful repricing—it is an exit rush. One day the debate is about margins; the next it is about whether the product becomes a feature inside a larger model.

Once that fear enters the room, it spreads quickly across anything tied to monetized knowledge work—data platforms, marketing software, legal tools, analytics, even media and advertising adjacencies. If AI does the work, who gets paid for it? That is the question markets are stress-testing in real time.

For years, software earned its margins by controlling workflow—owning the screen, the process, the friction. Humans did the thinking; software rented them the tools and charged a recurring toll. Predictable. Scalable. Defensible. That doctrine is now under review.

Bitcoin and gold sliding alongside tech is telling. When risk sentiment turns, speculative layers lose sponsorship first. It is not ideology—it is mechanics. When leverage gets pulled back, froth goes first.

This does not mean tech is finished. It means tech is being tested.

Every cycle follows the same arc: markets fall in love with innovation, price it as destiny, then recoil when destiny arrives with disruption and bills. AI is no longer just a growth story—it is a competitive weapon. That creates winners and losers, not a rising tide. The trade is shifting from owning the theme to owning the survivors.

This is what a regime change looks like within a sector. Euphoria gives way to scrutiny. Momentum yields to forensic analysis. Markets stop paying for possibility and start paying for proof.

Ironically, the most technologically advanced firms often feel the shock first—they sit closest to the blast radius. If your business automates knowledge work and a universal automation engine shows up, you do not get to pretend the rules stayed the same.

Panic, of course, is rarely precise. Markets swing the hammer before identifying the nail. These moments tend to overshoot because fear moves faster than analysis.

This looks less like the end of AI and more like a narrative reckoning. The market is re-evaluating who captures value, who loses the toll booth, and who gets displaced.

AI is not killing tech. It is forcing tech to prove it has a moat—not just a story.

When markets stop buying dreams, they start auditing business models.

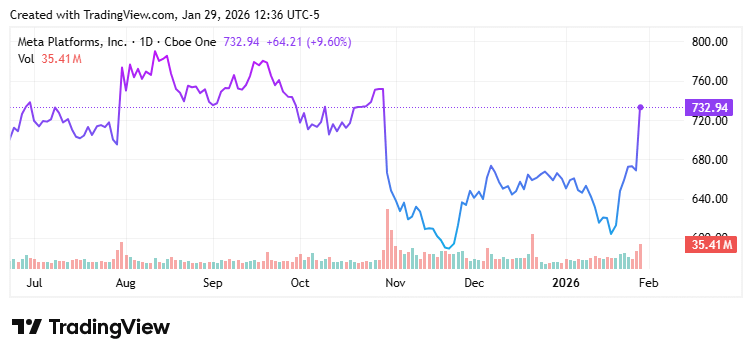

After spending months in the doldrums, Meta Platforms appears to have reshaped the narrative around its business. The Magnificent Seven stock slumped 11% in October following its third-quarter earnings release, as investors grew increasingly concerned about runaway spending on artificial intelligence.

That skepticism now looks to be fading after Meta’s fourth-quarter 2025 earnings report, released on Jan. 28. Shares climbed roughly 8% in after-hours trading by 7:00 p.m. ET, prompting investors to rethink the company’s outlook, with growth prospects increasingly overshadowing prior worries about spending.

Meta delivers strong earnings beat and upbeat guidance

In the fourth quarter, Meta reported revenue of $59.9 billion, representing growth of about 24% and comfortably exceeding expectations of $58.3 billion, or 21% growth. Adjusted earnings per share (EPS) came in at an impressive $8.88, up nearly 11% year over year and well above the consensus estimate of $8.16.

The standout highlight, however, was Meta’s guidance for the first quarter of fiscal 2026. At the midpoint, the company forecasts revenue of $55 billion, far surpassing analysts’ expectations of $51.3 billion.

This outlook implies quarterly revenue growth of roughly 30%, which would mark Meta’s fastest expansion rate since the third quarter of 2021. Such an acceleration is precisely what investors had been hoping for and offers further confirmation that the company’s investments in artificial intelligence are beginning to pay off.

Among Meta’s underlying performance metrics, growth in ad impressions delivered was particularly notable. The measure, which tracks the number of ads shown across Meta’s platforms, rose 18% during the quarter—its strongest pace in nearly two years. Chief Financial Officer Susan Li attributed this performance to robust user engagement and growth, highlighting that watch time on Instagram Reels increased 30% year over year, signaling a meaningful rise in platform engagement.

Stronger engagement is an encouraging signal for Meta, indicating that its AI-driven recommendation and ranking algorithms—responsible for determining what content users see and when—are becoming more effective. As these systems improve, users spend more time across Meta’s platforms, enabling the company to serve a greater volume of advertisements.

Markets shrug off higher-than-expected spending outlook

Expectations of sharply higher capital spending have been the key drag on Meta’s shares in recent months. Against that backdrop, the company’s latest CapEx guidance came in well above even elevated market expectations.

Meta now projects capital expenditures of $115 billion to $135 billion in 2026, compared with Wall Street estimates of roughly $110 billion. At the midpoint, this implies a 73% jump from 2025 CapEx of $72.2 billion.

In addition, Meta guided for total expenses of $162 billion to $169 billion in 2026, materially higher than consensus forecasts of around $150 billion.

Reading between the lines, however, reveals a crucial detail in Meta’s 2026 outlook. Management stated that “despite the meaningful step up in infrastructure investment, in 2026, we expect to deliver operating income that is above 2025 operating income.”

Since revenue equals operating income plus total expenses, this guidance allows for an implied revenue estimate. Meta generated $83.3 billion in operating income in 2025, and using the upper end of its 2026 expense guidance at $169 billion implies potential full-year revenue of roughly $252.3 billion.

That figure would represent about 25.5% growth from Meta’s 2025 revenue of $201 billion—well above the approximately 18.3% growth rate analysts had been projecting for 2026.

Growth eclipses spending concerns as Meta’s AI strategy gains traction

Although Meta’s expense guidance initially appeared to be the primary concern for investors, the company ultimately rose above those figures with exceptionally strong growth projections. While critics continue to argue that Meta has yet to produce a best-in-class general-purpose AI model, the company’s financial performance tells a compelling story.

Meta’s AI strategy is proving effective, driving faster growth in its core business of social media advertising. After a challenging stretch, Meta Platforms appears to have delivered precisely what was needed to restore investor confidence.

U.S. stock index futures slipped slightly on Thursday evening after Wall Street ended mostly lower, as weaker-than-expected results from Microsoft rekindled doubts over the returns on heavy AI spending, while investors absorbed a wave of other corporate earnings.

S&P 500 futures dipped 0.3% to 6,975.0 points, Nasdaq 100 futures declined 0.3% to 25,916.75 points, and Dow Jones futures also fell 0.3% to 49,049.0 points by 19:36 ET (00:36 GMT).

Wall Street dips as Microsoft’s slide weighs; Apple earnings take center stage

The S&P 500 and NASDAQ Composite closed Thursday’s regular session on a weak note, with technology stocks among the session’s biggest laggards.

Shares of Microsoft Corporation (NASDAQ:MSFT) plunged 10% after the company’s quarterly earnings highlighted slower cloud revenue growth and record AI-related spending, failing to reassure investors about near-term returns.

Microsoft’s selloff dragged down broader technology sentiment, with software peers including ServiceNow Inc (NYSE:NOW) and SAP (NYSE:SAP) also posting steep declines following disappointing earnings and outlooks.

Investors were also focused on Apple Inc.’s (NASDAQ:AAPL) earnings released after the close, which topped expectations as strong iPhone demand and a recovery in Greater China boosted both revenue and profit.

Apple reported roughly $143.8 billion in revenue and earnings per share well above consensus estimates, sending its shares up nearly 1% in after-hours trading.

SanDisk jumps on earnings beat; Trump backs spending agreement

Elsewhere on the earnings front, shares of SanDisk Corporation (NASDAQ:SNDK) jumped 16% in after-hours trading after the storage-chip maker posted a strong profit beat and lifted its outlook, driven by stronger-than-expected demand for data-center and AI-focused memory products.

By contrast, Visa (NYSE:V) shares edged lower despite surpassing first-quarter earnings and revenue forecasts, as investors focused on weaker-than-expected transaction volumes and ongoing caution surrounding broader consumer spending.

On the political side, President Donald Trump voiced support for a bipartisan spending agreement crafted by Senate Republicans and Democrats aimed at avoiding an imminent government shutdown, expressing his backing on Truth Social and calling for cooperation.

The deal would provide funding for most federal agencies while deferring divisive immigration issues for future negotiations.

Jefferies says Microsoft’s recent pullback presents an attractive entry opportunity

Jefferies analyst Brent Thill wrote this week that the recent pullback in Microsoft Corporation (NASDAQ: MSFT) shares has created an attractive buying opportunity. He highlighted the company’s expanding backlog, deepening AI partnerships, and continued strength in cloud computing as the foundations of a robust multi-year growth outlook among large-cap technology names.

Thill noted that the stock has declined about 18% since the first fiscal quarter, despite Microsoft disclosing roughly $250 billion in commitments to OpenAI and an additional $30 billion linked to Anthropic. He added that Microsoft’s current valuation—around 23 times calendar-year 2027 earnings—now trades below that of Amazon and Google, even though Microsoft offers what he sees as superior earnings visibility.

According to Thill, Microsoft’s record level of contractual commitments is the primary catalyst for buying at current prices. He expects second-quarter remaining performance obligations to show the largest sequential increase on record, driven largely by the OpenAI and Anthropic agreements, which he says provide “unprecedented multi-year demand visibility.”

Azure remains a central source of upside. Thill described Azure demand as constrained by supply rather than demand, noting that Microsoft plans to double its data-center capacity over the next two years. After beating Azure revenue guidance for three straight quarters, he believes that execution on new capacity alone could push results above consensus expectations for both fiscal second-quarter Azure performance and full-year 2026 forecasts.

The analyst also pointed to accelerating AI monetisation from Copilot and other first-party products. With Azure representing roughly 30% of total revenue, he said sustained outperformance in the cloud business could push overall revenue growth into the high-teens.

Although Thill acknowledged ongoing capacity constraints and elevated capital expenditures, he believes Microsoft is well positioned to generate meaningful upside to both revenue and earnings through fiscal 2026.

Analyst upgrades Google to Strong Buy as AI stack accelerates

Earlier this week, Raymond James upgraded Google parent Alphabet (NASDAQ: GOOGL) to Strong Buy, arguing that the company is entering a phase in which its AI stack is “shifting into high gear,” creating the conditions for meaningful upward revisions to medium-term forecasts.

Analyst Josh Beck said updated bottom-up analysis across Search and Google Cloud Platform (GCP) led him to raise his 2026 and 2027 estimates, with his 2027 revenue projection now exceeding broader Street expectations. He believes Alphabet is “entering a cycle of strengthening AI stack momentum and upward estimate revisions that could produce one of the highest-quality top-line AI acceleration stories in the public markets.”

Beck added that in 2026, the AI stack narrative and related forecast upgrades are likely to become the primary performance drivers among mega-cap internet stocks, rather than a simple mean-reversion trade.

Within Cloud, Beck projects GCP revenue growth of 44% in 2026 and 36% in 2027, ahead of consensus. He attributes this to strong momentum in infrastructure and platform services, underpinned by large-scale TPU and GPU deployments and increasing adoption of the Gemini API and Vertex AI.

By the end of 2027, Beck estimates that GCP could generate approximately $25 billion in annualised revenue from TPUs, around $20 billion from GPUs, about $10 billion from the Gemini API, and roughly $2.5 billion from Vertex AI.

In Search, Beck projects revenue growth of 13% in both 2026 and 2027—above broader Street expectations—as softness in core search is offset by the expanding adoption of AI Overviews, AI Mode, and Gemini. He expects AI-driven queries to drive stronger cost-per-click growth as improved context and conversion rates enhance monetisation.

Stifel starts Micron at Outperform, citing a multi-year memory market upturn

Brokerage firm Stifel initiated coverage of Micron Technology with an Outperform rating, arguing that the memory industry is entering a multi-year upcycle driven by structural AI demand and persistently tight supply conditions.

Stifel believes Micron is well positioned to benefit from rising average selling prices and a favorable mix shift toward higher-margin products, as memory increasingly becomes a critical constraint within AI systems. “Access to memory has emerged as a key bottleneck in AI racks and systems, boosting demand for higher-performance, higher-bandwidth memory solutions,” the firm said.

With supply expected to remain constrained through 2027, Stifel sees an environment supportive of sustained pricing power and margin expansion. Against this backdrop, the firm expects Micron to capture significant ASP growth and expand margins, forecasting non-GAAP EPS growth of more than 275% over the next two years.

High-bandwidth memory (HBM) is central to Micron’s growth thesis, according to Stifel. As AI models become more complex and require faster access to larger data sets, next-generation chips are incorporating more HBM, increasing memory’s share of overall AI infrastructure spending. As the industry’s number-two player, Micron is expected to see HBM revenue grow 164% in fiscal 2026 and a further 40% in fiscal 2027, with DDR and QLC NAND also benefiting from AI-driven demand.

Stifel also highlighted several risks, including the potential re-emergence of Samsung as a more formidable HBM competitor, elevated capital spending that could shift value toward equipment suppliers, a possible easing in DRAM supply-demand dynamics, and the risk that chipmakers design their own base logic dies.

On valuation, Stifel noted that Micron trades at roughly 9.7 times calendar 2026 earnings, modestly below historical averages. “While valuation increasingly reflects significant growth expectations, we believe the shares can continue to perform on the back of a multi-year, AI-driven product cycle characterized by tight supply,” the firm concluded.

Mizuho says Arm selloff presents a buying opportunity

Mizuho analyst Vijay Rakesh said investors should take advantage of the recent pullback in Arm Holdings shares to build positions, arguing that market concerns around handset demand have become excessively pessimistic.

Arm’s stock has declined roughly 30% since November, even as the Philadelphia Semiconductor Index has risen about 10%. Rakesh described the selloff as “overdone,” adding that Mizuho would “be buyers of ARM on the approximately 30% pullback.”

According to Rakesh, Arm’s growth drivers extend well beyond smartphones. While mobile royalties account for about 50% of revenue, he noted that Arm has historically outpaced handset market growth and is projected to expand at annual rates of 7% to 31% between 2021 and 2027.

A key catalyst is the ongoing transition to Arm’s v9 architecture, which delivers roughly double the average selling price per core compared with v8, providing a structural uplift to royalty revenue. Rakesh also highlighted rising interest in custom silicon, noting that potential ASIC and CPU ramps in 2027 and 2028 could contribute more than $1 billion in incremental revenue.

He further pointed to opportunities tied to AI-focused custom chips, including a potential training and inference ASIC associated with OpenAI and SoftBank. That initiative alone, he said, could conservatively generate around $1 billion in revenue during the 2027–2028 period.

Beyond mobile, Arm is gaining traction in data centers as hyperscalers increasingly adopt its architectures. Rakesh cited platforms such as AWS Graviton, Microsoft Cobalt, Meta’s planned CPU, and Nvidia’s Grace and Vera as evidence of a growing custom silicon customer base and an improving royalty mix.

Rakesh reiterated Mizuho’s Outperform rating and $190 price target, saying Arm remains “well positioned as the broadest global semiconductor platform.”

Morgan Stanley grows more positive on European semiconductor stocks

Morgan Stanley upgraded the European semiconductor sector to Overweight this week, arguing that the group offers an attractive environment for selective stock picking as diversification inflows gather pace, valuation dynamics improve, and semiconductor equipment companies stand to benefit from the next phase of the AI capital expenditure cycle.

The firm’s strategists noted that European equities are attracting increased diversification inflows while beginning to emerge from a long-standing valuation discount to U.S. markets. Within this context, semiconductors stand out as a sector where strengthening bottom-up fundamentals are increasingly driving top-down performance. Morgan Stanley said its preferred expression of this view remains analyst-led stock selection rather than broad factor exposure.

“While European equities already appear highly idiosyncratic, we see further scope for stock-level dispersion in Europe to rise toward cycle highs,” the strategists wrote.

The upgrade is anchored in the semiconductor equipment segment. Morgan Stanley highlighted ASML as the dominant contributor to European Top Picks performance year to date, accounting for more than half of weighted gains. ASML also represents roughly 80% of the MSCI Europe Semiconductors and Semiconductor Equipment index.

Looking ahead, the bank said risks in the AI investment cycle are shifting away from demand and toward execution and transition. “For 2026, the key risk in the AI capex cycle is execution and transition, not demand,” the strategists wrote, arguing that this dynamic favors European semiconductor equipment exposure—particularly companies tied to extreme ultraviolet lithography.

Morgan Stanley expects upcoming order intake to confirm higher foundry and memory capital spending through 2027, alongside stronger-than-expected demand from China.

From a portfolio construction standpoint, the firm said it adjusted its sector model to reflect improving earnings momentum and broader price-target revisions for European semiconductors, while neutralising accrual factors and reducing China exposure. These changes lifted the sector to second place in Morgan Stanley’s internal rankings, just behind banks.

At the stock level, ASML and ASM International remain Morgan Stanley’s Top Picks, with BE Semiconductor Industries also highlighted as an Overweight-rated beneficiary of the same themes.

TSMC (NYSE: TSM) reported a better-than-anticipated net profit for the fourth quarter on Thursday, as the global leader in contract chip manufacturing continued to capitalize on strong demand for its advanced chips driven by artificial intelligence.

The company also announced a significantly increased capital expenditure outlook for 2026, aiming to rapidly expand production capacity to keep up with growing AI-related demand.

TSMC’s CFO, Wendell Huang, revealed in a post-earnings call that the company expects its capital expenditure for 2026 to range between $52 billion and $56 billion, a substantial increase from $40.9 billion in 2025.

Huang also cautioned that TSMC’s mid- to long-term profit margins are likely to decline as the company continues expanding its production capacity, particularly in overseas locations. CEO C.C. Wei echoed these concerns, highlighting “significantly higher” capital spending and costs in the years ahead.

For the quarter ending December 31, TSMC posted a record net profit of T$505.74 billion ($16 billion), surpassing Bloomberg’s estimate of T$467 billion and significantly up from T$374.68 billion the previous year.

The company’s quarterly revenue, previously disclosed, rose to T$1.046 trillion ($33 billion), up from T$868.46 billion a year earlier. Huang forecasted first-quarter 2026 revenue between $34.6 billion and $35.8 billion.

TSMC’s strong performance was driven by robust demand for its advanced chips, with its 3-nanometer products contributing over 25% of revenue from its wafer segment.

CEO C.C. Wei indicated that the strong AI-driven demand is expected to continue in the coming years, with positive feedback from TSMC’s largest customers. He emphasized that the “AI megatrend” remains firmly in place.

While TSMC’s high-performance computing segment continues to be its primary revenue source, the smartphone chip division’s contribution increased slightly to 32% in Q4, up from 30% the previous quarter. This growth was likely boosted by Apple Inc., which incorporated new TSMC-made chips in its iPhone 17 lineup.

TSMC is also a crucial supplier of advanced AI processors to NVIDIA Corporation, a partnership that has significantly boosted its earnings and market value over the past two years.

The company has benefited greatly from a surge among major tech firms to expand data center infrastructure supporting AI development, as advanced processors are vital for handling AI models’ intense computing demands.

Last year, TSMC announced a $165 billion investment in the U.S., mainly targeting increased production capacity at its Arizona facility. This move also appears aimed at addressing the Trump administration’s push for more domestic manufacturing.

On Thursday, TSMC signaled plans to further expand U.S. production, with a goal of allocating 20% to 30% of its overall capacity to the Arizona plant.

TSMC is broadly seen as a key indicator of chip demand and the AI market trends.

The self-driving car industry has experienced a cycle of high hopes, costly setbacks, and ongoing delays. From Tesla’s (NASDAQ:TSLA) frequent missed deadlines to General Motors (NYSE:GM) shutting down its Cruise autonomous division following a pedestrian accident, achieving fully autonomous vehicles has been much tougher than early developers expected.

However, a fresh wave of innovation driven by artificial intelligence and strategic collaborations is revitalizing this groundbreaking technology.

At the forefront of this resurgence is Nvidia (NASDAQ:NVDA), the chipmaker whose leadership in AI computing is now expanding into the automotive sector, providing Western car manufacturers with a potential way to rival China’s rapidly progressing autonomous driving advancements.

The Present State of Autonomous Driving in the U.S.

The U.S. self-driving industry is currently at a critical juncture, with only a few companies still seriously competing. In 2019, Tesla CEO Elon Musk confidently predicted that a million autonomous vehicles would be on the roads within a year. However, the company only rolled out a limited robotaxi pilot program in late 2025, falling six years behind schedule. A major challenge has been the countless unpredictable scenarios, known as edge cases, that can confuse autonomous systems.

Traditional automakers have mostly pulled back from the sector. General Motors shut down its Cruise autonomous division following a serious incident where one of its vehicles hit and dragged a pedestrian.

Similarly, Ford Motor ceased its internal autonomous vehicle projects, choosing to withdraw from the capital-heavy competition. Alphabet’s (NASDAQ:GOOGL) Waymo remains the only company maintaining consistent operations, currently offering Level 4 robotaxi services in several U.S. cities.

At the same time, China has made significant advances supported by strong government backing and rapid deployment. Chinese automakers now account for about seventy percent of global electric vehicle production, while companies such as BYD, Baidu, and Pony.ai are growing their robotaxi services throughout Asia and the Middle East.

The Chinese government recently authorized two vehicles with Level 3 autonomous driving capabilities, permitting hands-free driving. This regulatory endorsement, along with better network infrastructure and more affordable costs, has established China as a rising leader in autonomous technology.

Nvidia’s Self-Driving Platform: Revolutionizing the Industry

At CES 2026 in Las Vegas, Nvidia introduced its solution to the autonomous driving challenge: the Alpamayo platform. Simply put, Alpamayo is a comprehensive toolkit that enables automakers to develop self-driving systems without starting from zero.

The platform features reasoning models that help vehicles interpret and respond to their environment, simulation tools for safely testing various scenarios, and datasets for training the AI. It can process data from cameras and radar sensors to make decisions on steering, braking, and acceleration while also providing explanations for its choices.

What makes Alpamayo especially noteworthy is that Nvidia has made it open-source, allowing any company to use and adapt it freely. This approach contrasts sharply with Tesla’s proprietary model.

Industry experts liken this to the smartphone battle between Apple’s (NASDAQ:AAPL) closed ecosystem and Android’s open platform. By offering a shared foundation, Nvidia empowers automakers to concentrate on differentiating their products rather than reinventing fundamental technology, potentially speeding up the entire industry’s development.

The platform is quickly gaining momentum. Mercedes-Benz revealed that its upcoming CLA model will incorporate AI-driven driving features powered by Nvidia’s technology, set to hit U.S. roads later this year. Additionally, a robotaxi partnership involving Lucid Group, Nuro, and Uber plans to leverage Nvidia’s chips and platform.

Ali Kani, Nvidia’s general manager of the automotive division, expressed optimism that recent fundamental AI improvements have resolved critical issues that once hindered self-driving technology, indicating the industry might be nearing a major breakthrough.

NVDA Share Forecast and What Investors Should Know

Nvidia’s stock mirrors its leading position in several AI-driven markets. As of January 2026, NVDA shares are trading around $185 each, with a market cap near $4.5 trillion, ranking it among the world’s most valuable companies.

The stock has delivered remarkable returns, rising more than 32% in the past year and an impressive 1,297% over five years, significantly outperforming the S&P 500’s 81% gain during the same timeframe.

Despite its high valuation, key financial indicators remain strong. In Q3 FY26, Nvidia reported revenues of $57 billion and earnings of $31.8 billion, surpassing analyst expectations for earnings per share by four cents.

The trailing price-to-earnings (P/E) ratio stands at about 46, while the forward P/E is 24, reflecting the market’s high growth expectations. However, a PEG ratio of 0.70 indicates that the stock’s valuation could be reasonable relative to its anticipated earnings growth. Nvidia continues to demonstrate strong profitability, with a profit margin above 53% and a return on equity exceeding 100%.

Analysts generally hold a positive outlook on Nvidia’s future. The average price target of $252 suggests about a 36% potential increase from current levels, with forecasts ranging from $140 on the low side to $352 at the high end. Most analysts have Buy or Strong Buy ratings, highlighting sustained strong demand for AI infrastructure.

While Nvidia’s automotive division offers a growing avenue beyond its core data center business, investors should be aware that the stock exhibits high volatility, with a beta of 2.31. The upcoming earnings report on February 25, 2026, is expected to shed more light on the company’s progress.

Bank of America has unveiled its latest list of high-conviction U.S. stock ideas for Q1 2026, featuring nine Buy-rated names and one Underperform recommendation.

Bank of America’s quarterly lineup features companies identified as having “significant market and business-related catalysts in the quarter ahead,” according to BofA strategist Anthony Cassamassino.

The Buy recommendations cover nine industries and include Amazon, Boeing, Cigna, Constellation Energy, Dollar General, Equinix, Merck, Spotify, and Vertex Pharmaceuticals. The only Underperform rating goes to homebuilder Lennar.

The bank emphasized that this list targets short-term opportunities and will be updated only at the start of each quarter unless there are rating changes.

While artificial intelligence remains a key theme, BofA noted that “the drivers for the broader list are more diverse.” Legislative developments could act as a catalyst for Cigna, while Merck stands out due to its “attractive valuation.”

Dollar General may benefit from “higher-than-expected tax refunds in the first quarter of 2026.”

Amazon tops BofA’s large-cap internet stock picks, given its exposure to AI through AWS and the bank’s expectation of accelerating AWS revenue growth into 2026.

“For Boeing, we expect the first quarter to focus on commercial production rates,” Cassamassino added. “Stable production is crucial for investor confidence and the company’s momentum this year.”

For the broader market, BofA’s U.S. equity strategist Savita Subramanian cautioned that “there is no way to sugar coat it – the S&P 500 is expensive.”

However, she highlighted Health Care, Information Technology, and Real Estate as sectors that “screen attractive near-term.”