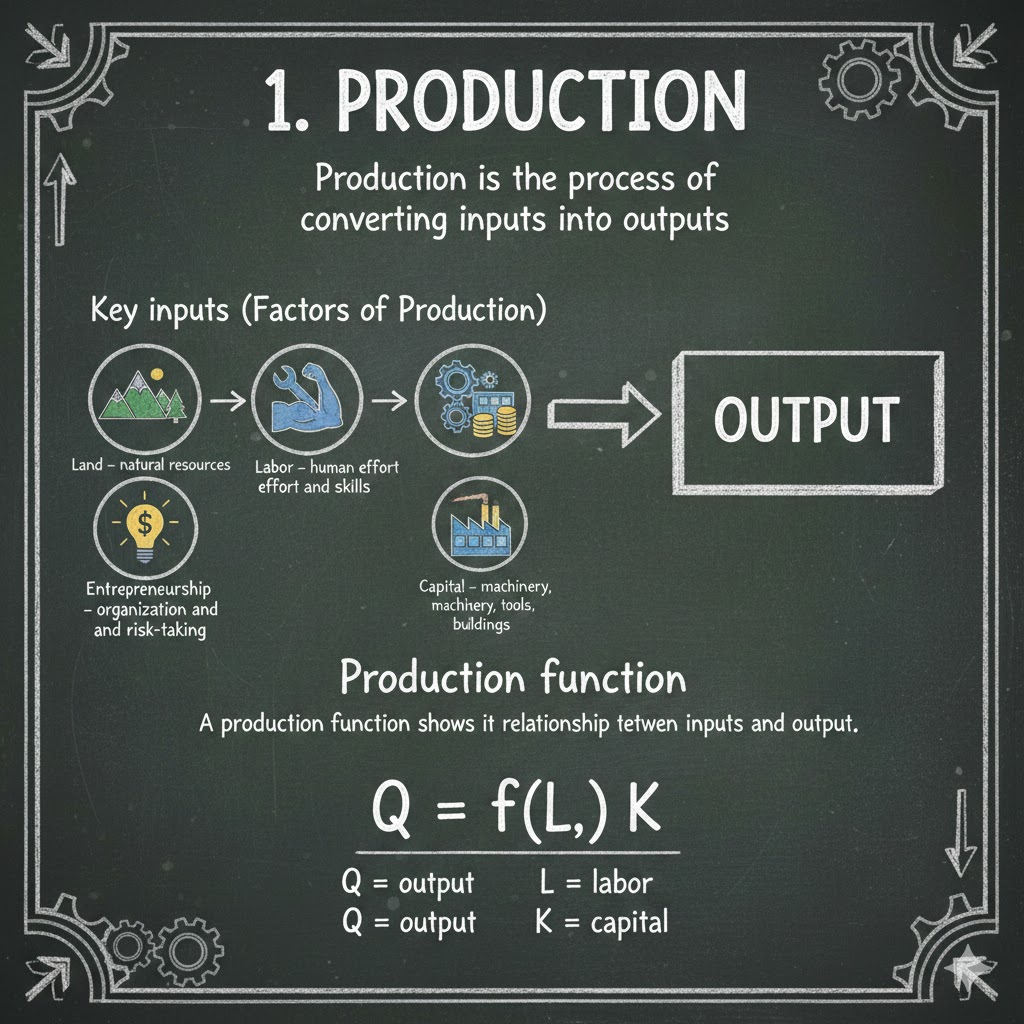

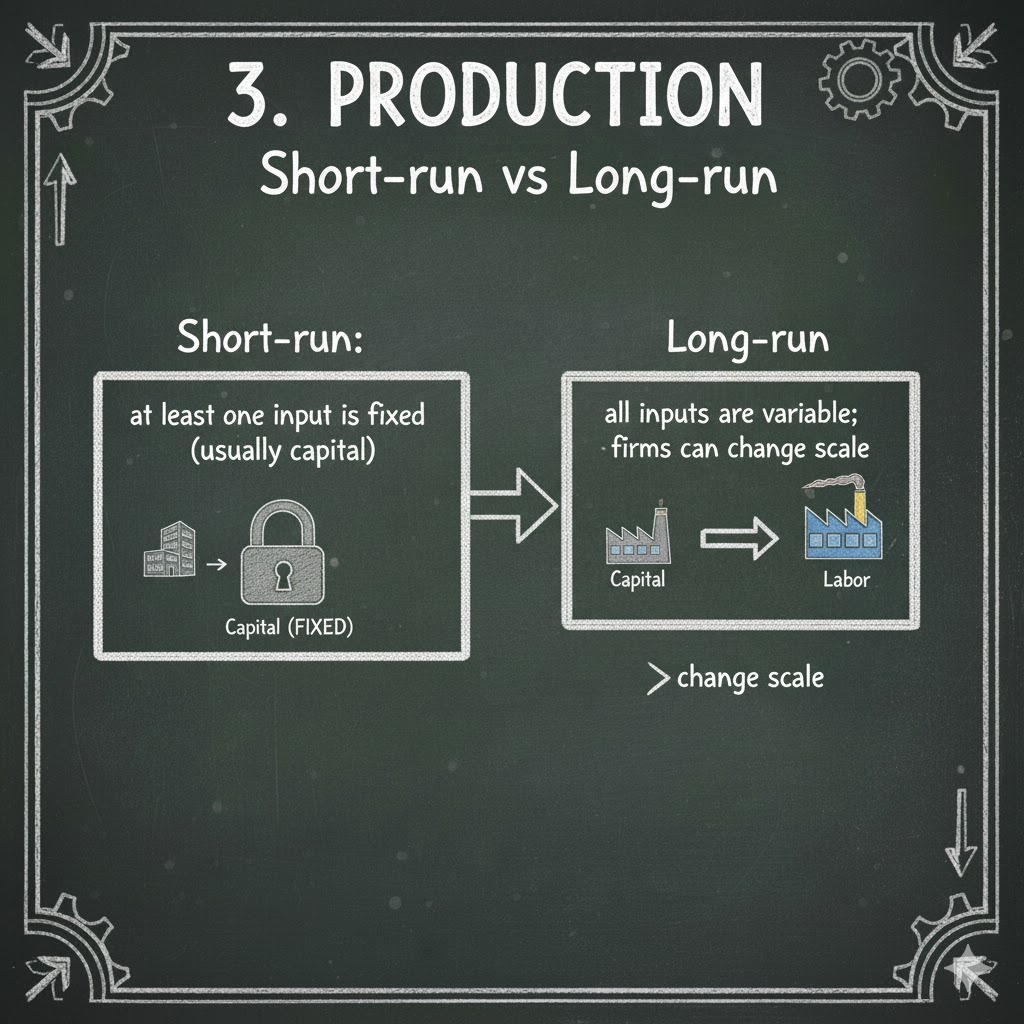

Production and cost describe how firms transform inputs into goods or services and the expenses incurred in that process. Understanding this relationship helps explain pricing, profitability, efficiency, and business decisions.

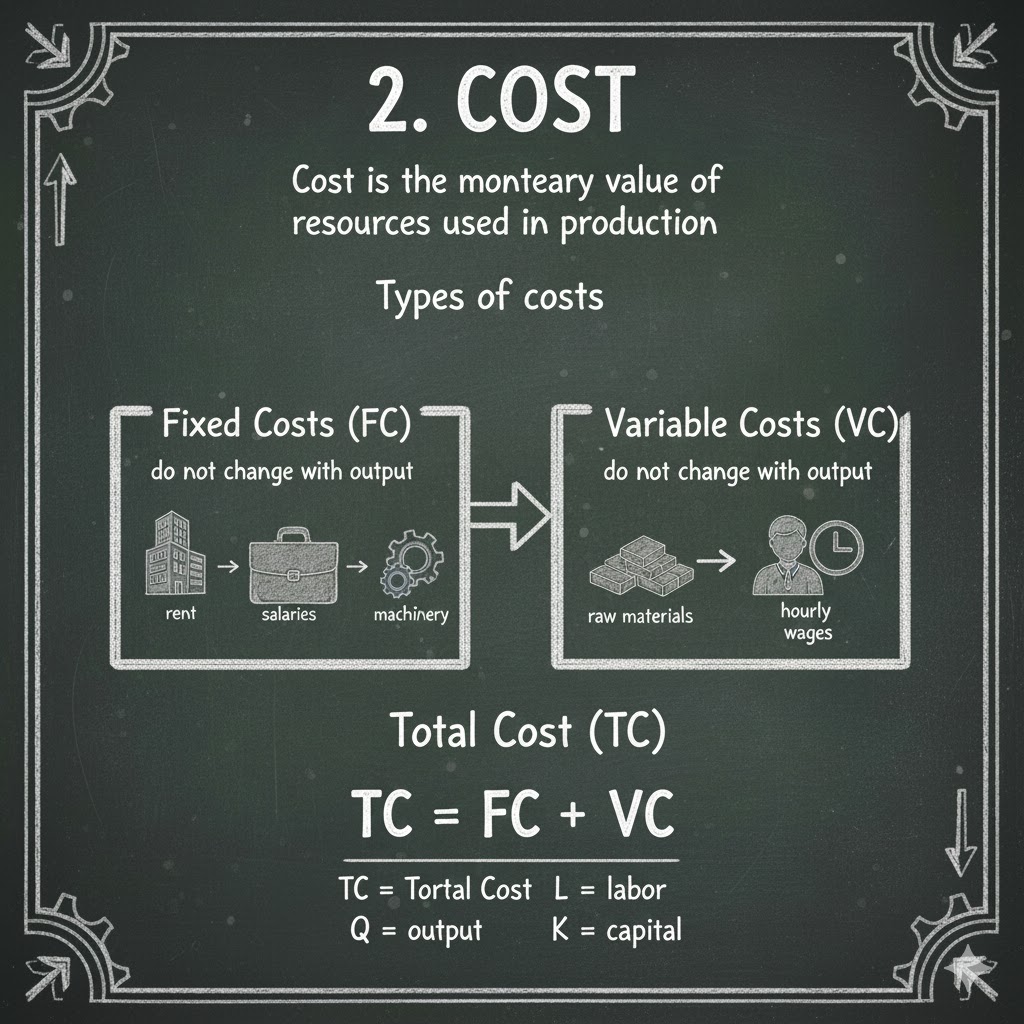

Cost measures

- Average Cost (AC) AC=QTC

- Marginal Cost (MC): cost of producing one more unit: MC=ΔQΔTC

📌 Marginal cost is crucial for production decisions and pricing.

Production, cost, and profit

- Profit = Total Revenue (TR) − Total Cost (TC)

- Firms maximize profit where:

MR=MC

(Marginal Revenue equals Marginal Cost)

Key takeaway

Efficient production minimizes cost and maximizes profit.

Understanding cost structures helps firms decide how much to produce, at what price, and at what scale.