U.S. stock index futures were largely unchanged late Tuesday as investors remained cautious ahead of the Federal Reserve’s interest rate decision and a busy earnings schedule featuring major technology leaders.

S&P 500 futures edged up 0.1% to 7,017.50, while Nasdaq 100 futures rose 0.3% to 26,155.75 by 20:10 ET (00:10 GMT). Dow Jones futures were flat at 49,154.0.

S&P 500 closes at a record as Dow edges lower on Medicare concerns

During Tuesday’s regular session, the S&P 500 climbed 0.4% to a record closing high, extending its advance as investors rotated back into growth stocks and responded positively to broadly solid earnings results. Gains in technology shares led the move, pushing the benchmark to a fresh peak.

The Nasdaq Composite jumped 0.9%, driven by strength in megacap stocks.

Meanwhile, the Dow Jones Industrial Average fell 0.8%, weighed down by steep declines in healthcare and insurance shares. Major health insurers came under pressure after the U.S. government released a Medicare Advantage payment plan that the market perceived as less favorable than anticipated.

Markets focus on Fed decision and megacap earnings

Investor focus has shifted squarely to the Federal Reserve, which kicked off its two-day policy meeting on Tuesday. The central bank is widely expected to leave interest rates unchanged when it delivers its decision on Wednesday, with markets pricing in a pause as policymakers assess easing but still-elevated inflation alongside signs of steady economic growth and a resilient labor market.

Close attention will be paid to Fed Chair Jerome Powell’s remarks for indications on how long rates may remain at current levels and when eventual cuts could begin.

“The key will be any dissent and the Fed’s communication, particularly around questions of central bank independence,” ING analysts said, adding that the decision will also be overshadowed by President Trump’s upcoming nomination of a new Fed chair.

Corporate earnings are another major catalyst this week, with four members of the so-called “Magnificent Seven” technology group set to report. Tesla, Meta Platforms and Microsoft are scheduled to post results on Wednesday, followed by Apple on Thursday.

Given their heavy weighting in major equity indexes, guidance from these companies on artificial intelligence investment, cloud demand and consumer trends is expected to play a key role in shaping near-term market direction.

President Donald Trump once again surprised markets by announcing an increase in tariffs on South Korea to 25% from 15%, citing Seoul’s failure to implement a trade agreement reached last July. The move targets sectors such as autos, lumber, and pharmaceuticals, yet South Korean equities ended up surging 2% to fresh record highs. The KOSPI initially slid more than 1%, but the dip quickly attracted buyers seeking exposure to Asia’s strongest-performing equity market of 2025.

With South Korea’s industry minister set to travel to Washington, investors appear to be betting on a negotiated climbdown, reviving the popular “TACO” trade—Trump Always Chickens Out. Few are surprised that Seoul has been reluctant to commit massive U.S. investments while the risk of abrupt tariff threats remains a defining feature of the administration.

Tariff uncertainty also boosted demand for precious metals, pushing gold and silver back toward record levels. Gold rose 1% to $5,063 an ounce, while silver jumped 5% to $109 an ounce.

Asian equities were broadly firmer, supported by optimism that blockbuster earnings from the U.S. “Magnificent Seven,” beginning with Meta, Microsoft and Tesla later this week, will help sustain the global equity rally into 2026. MSCI’s Asia-Pacific index excluding Japan climbed 1% to a new high, while Japan’s Nikkei added 0.7%, even as the yen hovered near a two-month peak—normally a headwind for exporters.

European equities are poised for a firmer open, with EURO STOXX 50 futures up 0.3%. U.S. futures are also higher, as Nasdaq futures climb nearly 0.6% and S&P 500 futures rise 0.3%. The global economic calendar remains relatively quiet ahead of Wednesday’s Federal Reserve policy decision, at which interest rates are widely expected to be left unchanged. Nevertheless, the meeting is likely to be dominated by the Justice Department’s investigation into Fed Chair Jerome Powell, adding extra scrutiny to his post-meeting press conference. Any indication that Powell may choose to remain on the Fed’s board after his term ends in May—a move permitted under Fed rules—could provoke an unpredictable reaction from President Trump.

The year ahead offers a clear divide between bullish and bearish outcomes for investors. Will 2026 deliver another period of above-average returns, or mark a turning point toward disappointment? Optimists contend that the foundations for a sustained rally remain intact. A robust technology cycle, heavy corporate investment, and supportive policy settings all suggest further upside. Pessimists, however, warn that key growth drivers are losing momentum, market leadership has become uncomfortably narrow, and underlying economic stress is increasingly evident.

After a strong 2025, investors are entering a shifting market environment. Liquidity is still plentiful, but concerns over stretched valuations, labor-market pressure, and consumer resilience are mounting. Much hinges on how long optimism can outweigh economic realities, and whether expected gains from artificial intelligence and capital spending arrive quickly enough to counteract the drag from debt burdens, interest costs, and widening inequality.

Sentiment remains broadly constructive, though far from unanimous. Equity strategists are split, while bond markets reflect expectations of rate cuts alongside rising recession risk. Fiscal stimulus may postpone a downturn, but it also exacerbates longer-term imbalances. For investors, the central challenge is maintaining objectivity. Both the bullish and bearish narratives are credible, and timing will be decisive. In fact, 2026 could validate elements of both cases, making adaptability the most valuable strategy.

Below, we examine the bullish and bearish scenarios for 2026 in detail, assessing the macroeconomic and market forces behind each view. By translating these dynamics into practical portfolio considerations, investors can prepare for either outcome. Ultimately, success in 2026 will hinge less on forecasting accuracy and more on disciplined risk management.

The Bullish Case

The bullish thesis rests on several core pillars: a fresh surge in technology-led investment, accommodative fiscal policy, improving liquidity conditions, and the ongoing strength of both corporate balance sheets and consumer activity. Together, these forces have propelled markets higher, and proponents argue they will continue to support gains through 2026.

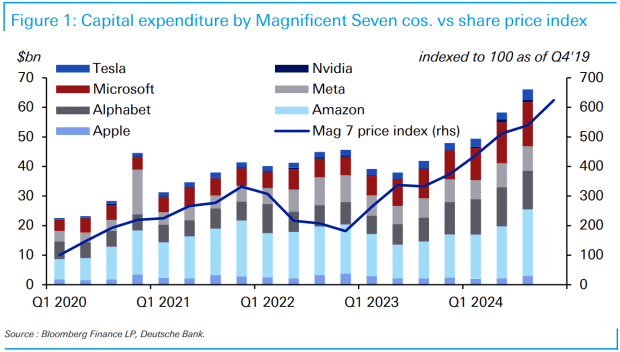

Central to the bull case is the rise of a potentially transformative technology cycle driven by artificial intelligence and large-scale infrastructure upgrades. Unlike earlier tech booms fueled primarily by optimism, this cycle is already translating into substantial capital spending. The so-called “Magnificent Seven” have collectively pledged over $600 billion toward data centers, semiconductor capacity, and AI-related services. This investment is rippling across software, energy, and industrial supply chains. Should the anticipated productivity improvements materialize, corporate earnings could accelerate, providing fundamental support for elevated valuations.

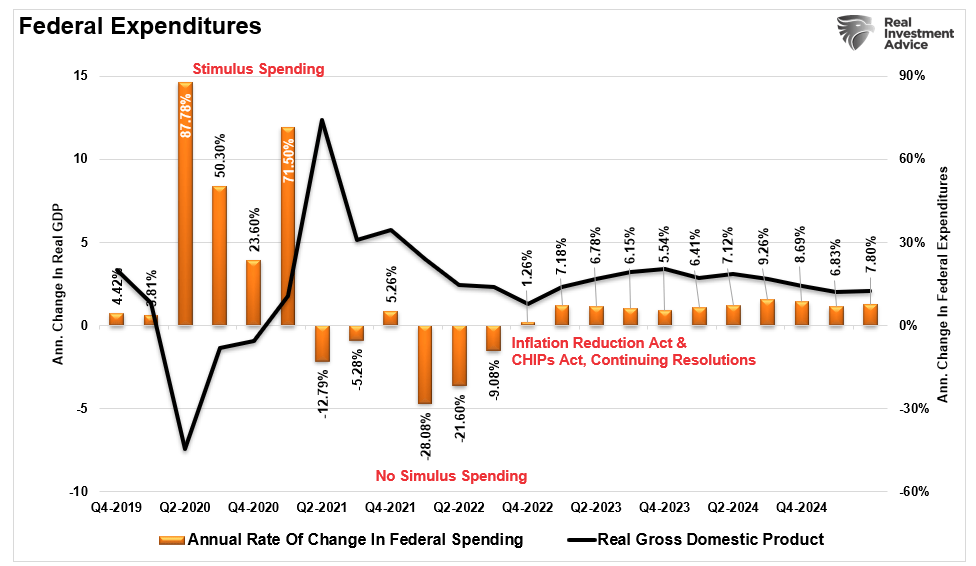

Fiscal policy is also positioned to support growth. Under a Trump-led administration, proposed tax cuts and direct transfers are expected to bolster both corporate activity and consumer spending. While $2,000 stimulus checks may not appear dramatic on their own, they can meaningfully lift short-term consumption and provide relief to small businesses. When paired with income tax reductions, these initiatives create a favorable backdrop for GDP growth and market sentiment. As recent history shows, following the 2022 market correction and widespread recession concerns, ongoing fiscal support has continued to play a stabilizing role in economic expansion.

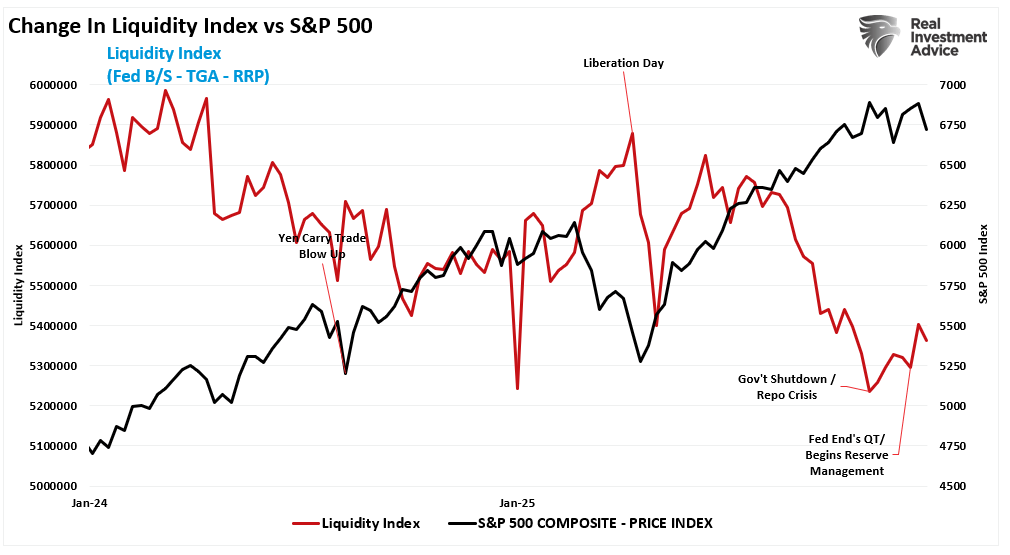

The monetary environment is also turning more supportive for bulls. Quantitative tightening concluded in December 2025, and the Federal Reserve has since shifted toward what many describe as “QE Lite,” combining rate cuts with monthly purchases of roughly $40 billion in short-term Treasuries. Officially framed as “reserve management,” the objective is to maintain ample liquidity within the financial system. As interest rates decline, credit conditions are likely to loosen, providing a favorable backdrop for risk assets. Rising liquidity has historically supported higher equity valuations, with technology and growth stocks typically benefiting the most from this dynamic.

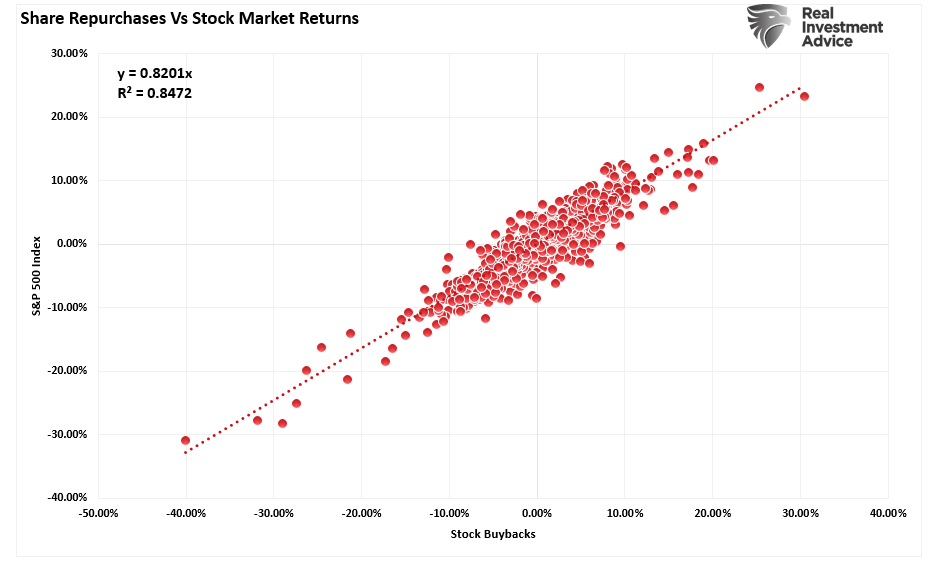

Corporate actions further reinforce the bullish narrative. Share buyback authorizations are projected to reach a new record of more than $1.2 trillion in 2026. Although often framed as a “capital return strategy”—a characterization that misses the point—buybacks have shown a strong correlation with equity market performance. Notably, since 2000, corporate repurchases have accounted for nearly all net equity demand, underscoring their outsized influence on stock prices.

Importantly, the notion that buybacks signal management’s confidence in future earnings is misleading. In practice, repurchases are frequently used as a form of financial engineering to boost per-share results and beat Wall Street expectations. This dynamic is likely to intensify in 2026, further supporting reported earnings growth and reinforcing the bullish case.

Finally, deregulation tied to the so-called “Big Beautiful Bill” is expected to relax capital requirements for banks, enabling them to hold a greater amount of collateral. While this should support the Treasury market, it also expands overall lending capacity. Much of that capacity is likely to flow into leverage for hedge funds and Wall Street trading desks, as looser regulatory constraints encourage greater risk-taking.

The bullish thesis ultimately rests on a reinforcing feedback loop: innovation spurs capital investment, rising investment lifts earnings, policy measures inject liquidity, and investors respond by increasing risk exposure. As long as each link in this chain remains intact, the upward trend can persist.

The Bearish Case

The bearish case starts with a key observation: many of the forces that powered the 2025 rally are now fading or already fully reflected in prices. Elevated valuations, softening economic data, and rising speculative excesses suggest that current market momentum may be masking deeper structural vulnerabilities. With that in mind, it is worth examining several of these risks more closely.

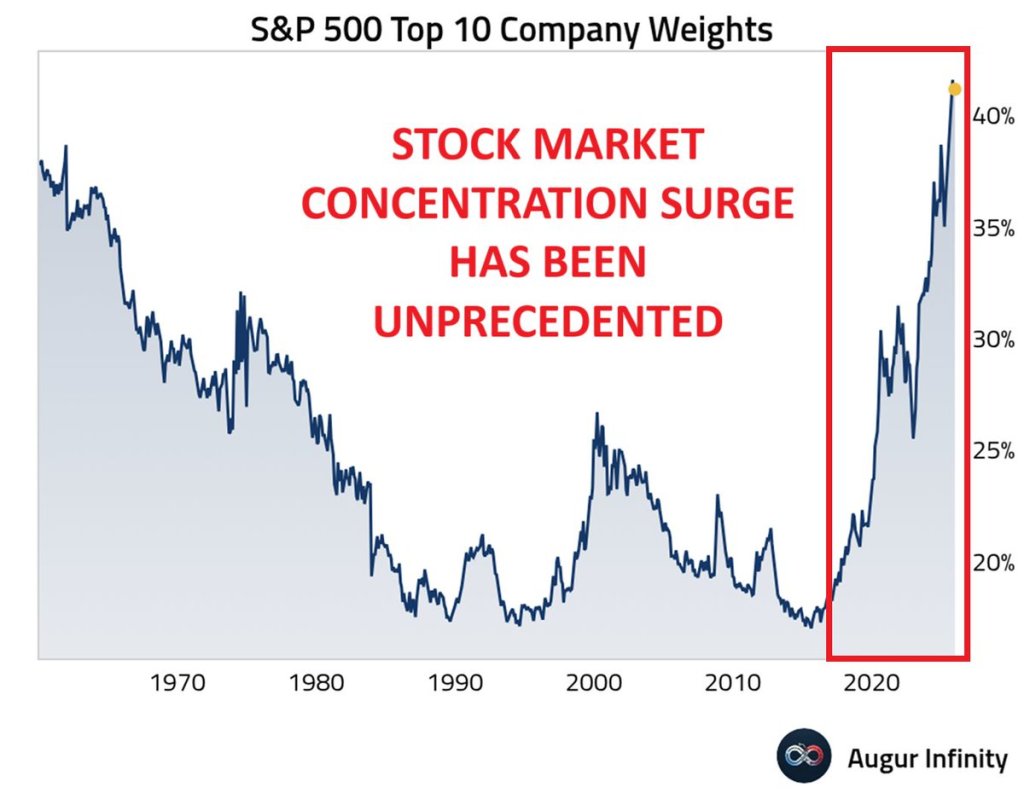

One of the most visible concerns is market concentration. In 2025, the bulk of equity gains came from just 10 companies on a market-capitalization-weighted basis, a dynamic amplified by the continued shift into passive ETF investing.

Passive investing has evolved from a niche approach into the dominant force shaping equity markets. Index funds and ETFs now represent more than half of U.S. equity ownership. Because these vehicles allocate capital according to market capitalization rather than valuation, fundamentals, or business quality, the largest companies attract a disproportionate share of inflows. This has created a powerful feedback loop in which rising prices draw in more capital, and those inflows, in turn, push prices even higher.

This narrow leadership is inherently fragile. Should investor flows into ETFs reverse, a disproportionate share of selling—roughly 40%—would be concentrated in the same 10 stocks. History shows that when market performance depends on a small handful of names, volatility tends to increase and drawdowns can be sharp.

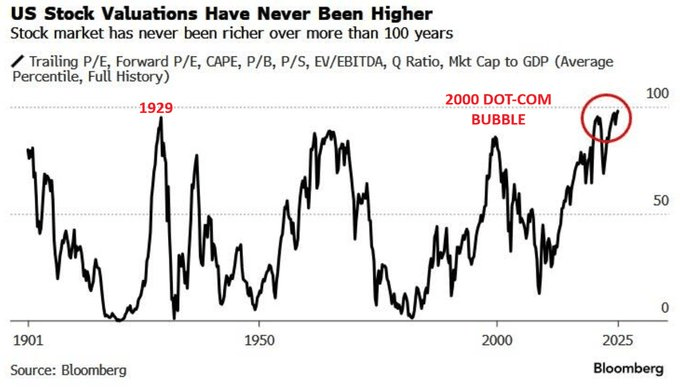

Valuations present another clear risk. Price-to-earnings multiples on the S&P 500 remain near cycle peaks, leaving little room for error. Growth assumptions are ambitious, and even modest earnings disappointments could trigger a meaningful repricing. While enthusiasm around AI has driven a surge in investment, much of this spending is circular—companies are investing in AI largely to produce and sell AI-related products. That dynamic may prove self-limiting over time, particularly if end demand weakens or costs begin to outstrip returns.

A significant portion of the current investment cycle is also being financed with debt, as companies borrow to fund capital spending, repurchase shares, and sustain dividend payouts. If interest rates remain high or credit conditions deteriorate, rising debt-servicing costs could quickly erode earnings gains.

The broader economic risk is that the reallocation of capital toward technology and automation could sideline large segments of the workforce. While the buildout of data centers may employ thousands during construction, only a fraction of those jobs—perhaps a few hundred—remain once operations begin. Over time, this dynamic could weigh on employment growth, increase the risk of demand destruction, and may already be showing early warning signs.

This dynamic underpins the concept of a “K-shaped economy.” While high-income households and asset owners continue to prosper, lower-income consumers are facing increasing strain. Consumption patterns are diverging as financially pressured households cut back, leaving the top 20% of earners responsible for nearly half of total consumer spending. Signs of stress are already emerging, with rising auto loan and credit card delinquencies, stagnant real wages for many workers, and persistently high costs for housing and essential goods.

At the same time, risks within the credit system—particularly in private markets—are growing. Private credit has expanded rapidly in recent years, yet limited transparency makes it difficult to fully assess systemic vulnerabilities. Regulators have begun to pay closer attention, and default rates in middle-market lending are climbing. Should these stresses intensify, the fallout could extend across banks, hedge funds, and pension portfolios.

The bearish argument is not one of an imminent crash, but of growing fragility. Beneath the headline gains, the market appears increasingly exposed to earnings disappointments, tighter credit conditions, and weakening consumer demand.

The key takeaway is that 2026 may validate elements of both the bullish and bearish narratives. Preparation, rather than prediction, will be essential.

Navigating Whatever Comes Our Way

Investors should treat 2026 as a year in which both the bullish and bearish narratives may ultimately be validated. In the first half, bullish momentum is likely to persist, supported by strong sentiment, ample liquidity, and continued growth in corporate investment. Optimism around AI, fiscal support, and a potential pause in monetary tightening could propel equity indexes higher.

By the second half, however, underlying vulnerabilities may begin to surface. Elevated valuations increase sensitivity to earnings disappointments, while widening economic inequality could weigh on the outlook for consumer demand and corporate revenues. Should these pressures intensify, market sentiment could shift rapidly.

Navigating such a divided year will require a tactical approach—participating in early upside while avoiding excessive exposure to risks that may materialize later in the year.

Early 2026: Participate in Momentum, but Manage Exposure

Overweight sectors poised to benefit from capital spending and ample liquidity, including technology, industrials, and energy.

Prioritize high-quality growth companies with durable earnings and strong cash-flow generation, rather than momentum-driven narratives.

Implement trailing stop-loss strategies to protect gains if market sentiment shifts.

Use periods of volatility to add selectively, while scaling back position sizes as valuations become more stretched.

Avoid excessive concentration in AI-related stocks, even during strong rallies, as crowding increases dispersion and downside risk.

Mid-to-Late 2026: Emphasize Defense and Cash-Flow Stability

Gradually rotate toward defensive, value-oriented sectors such as healthcare, consumer staples, and utilities.

Increase exposure to dividend-paying companies with strong balance sheets and resilient cash flows.

Raise cash allocations or shift into short-duration Treasuries to preserve flexibility.

Allocate selectively to high-quality credit while reducing exposure to private credit and high-yield debt.

Monitor consumer credit conditions, labor-market trends, and bank earnings for early signs of financial stress.

Throughout the Year: Maintain Discipline and Objectivity

Adhere to valuation discipline regardless of shifts in market narratives.

Keep portfolios well diversified to withstand both volatility and sector rotation.

Let data—not headlines—drive allocation decisions.

Rebalance regularly, particularly if strong first-half performance leads to excessive concentration in certain sectors.

In 2026, tactical flexibility, risk awareness, and discipline are likely to matter more than adopting a purely bullish or bearish stance. It is a year in which both camps could be partially wrong. Markets rarely move in straight lines, but a sound investment process should remain consistent throughout.

The year ahead is likely to test investors with heightened volatility, as both the bullish and bearish arguments carry real weight. A new technology cycle may generate genuine economic momentum, yet it also introduces risks tied to elevated valuations, debt-fueled growth, and widening inequality. With markets effectively pricing in near-perfection, history suggests outcomes often fall short of expectations.

Whether 2026 delivers further gains or a sharp correction, performance will hinge on effective risk management. Avoid anchoring to any single narrative. Let data guide decisions, respect your signals, and remain willing to adjust as conditions evolve.

Ultimately, the objective is not to chase short-term returns, but to endure—and compound—across full market cycles.

U.S. stock index futures showed minimal movement on Monday night, with Dow futures edging lower after a policy proposal from the Trump administration, as investors stayed cautious ahead of an important Federal Reserve decision and major tech earnings.

S&P 500 futures hovered near flat at 9,982.0, while Nasdaq 100 futures rose 0.2% to 25,898.2 by 19:54 ET (00:54 GMT). Meanwhile, Dow Jones futures slipped 0.3% to 49,409.0.

Wall Street ended higher, with the Dow up 0.6%, the S&P 500 gaining 0.5%, and the Nasdaq rising 0.4%.

The Trump administration proposed flat-rate payments for Medicare Advantage.

Dow futures edged lower after major health insurers slumped in late trading, following a Trump administration proposal to keep Medicare Advantage payment rates nearly flat, below market expectations. Shares of UnitedHealth, Humana, and CVS fell sharply on concerns that weaker reimbursement growth would squeeze margins amid rising medical costs. Separately, President Trump announced a hike in tariffs on South Korean imports to 25%, citing Seoul’s failure to ratify a trade deal.

Investors await the Fed decision and key megacap earnings.

Markets are in wait-and-see mode ahead of the Fed meeting, with rates expected to stay unchanged and focus on signals about future cuts. Attention is also on earnings from the “Magnificent Seven,” with results from Microsoft, Meta, Tesla, and Apple likely to shape sentiment, especially around AI investment, demand trends, and margins.

Wednesday brings the FOMC meeting and Chair Powell’s press conference, and it wouldn’t be surprising if President Trump chose that moment—ideally around 2:30 p.m. ET—to announce his pick for the next Fed chair. Such timing would dominate headlines, catch financial media off guard, and inject maximum uncertainty into markets.

That said, the Fed is not expected to cut rates at this meeting, which should keep the event relatively uneventful. In the bigger picture, what the Fed does between now and May may prove less important, particularly if a new chair is appointed and moves quickly toward easing.

Markets appear to be dialing back expectations for aggressive rate cuts. Current pricing suggests the fed funds rate settles near 3.25% by December, with little additional easing beyond that. To meaningfully shift those expectations, the nominee would likely need to be notably dovish—something markets already anticipate, given the widespread assumption that Trump will select a policy-leaning accommodator.

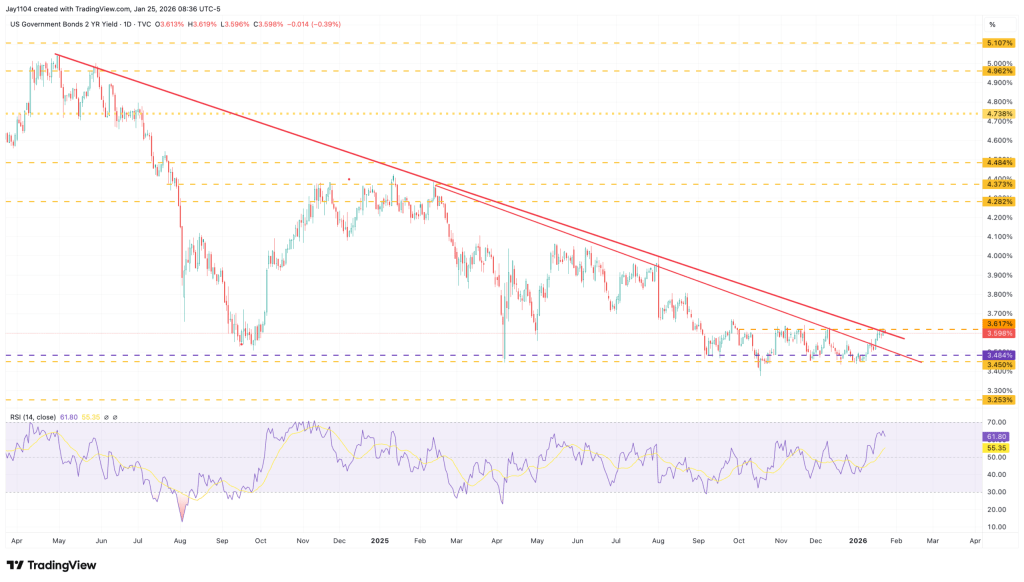

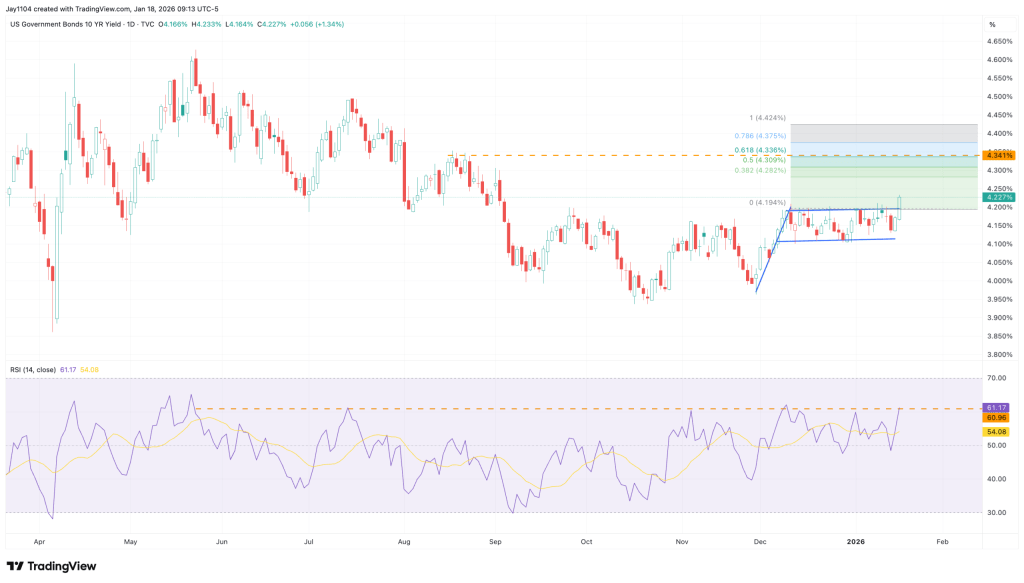

As a result, the risk of a breakout in the 2-year Treasury yield appears increasingly credible, with initial resistance near 3.62%. Beyond that, a move back toward the 4% level cannot be ruled out. From a technical perspective, the setup supports this view: the 2-year yield has formed multiple bottoms in recent months, and the RSI has begun to turn higher, signaling building upside momentum.

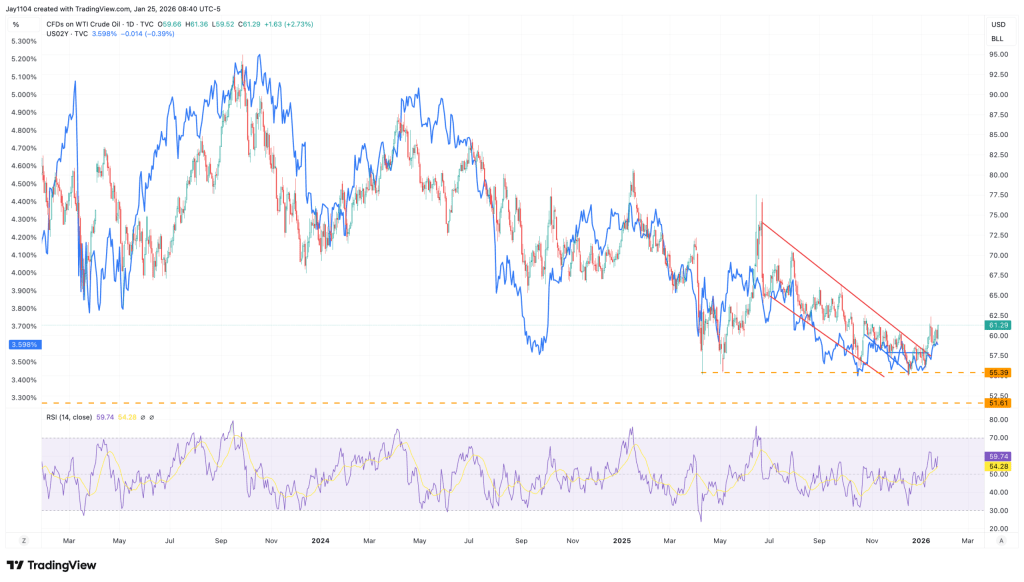

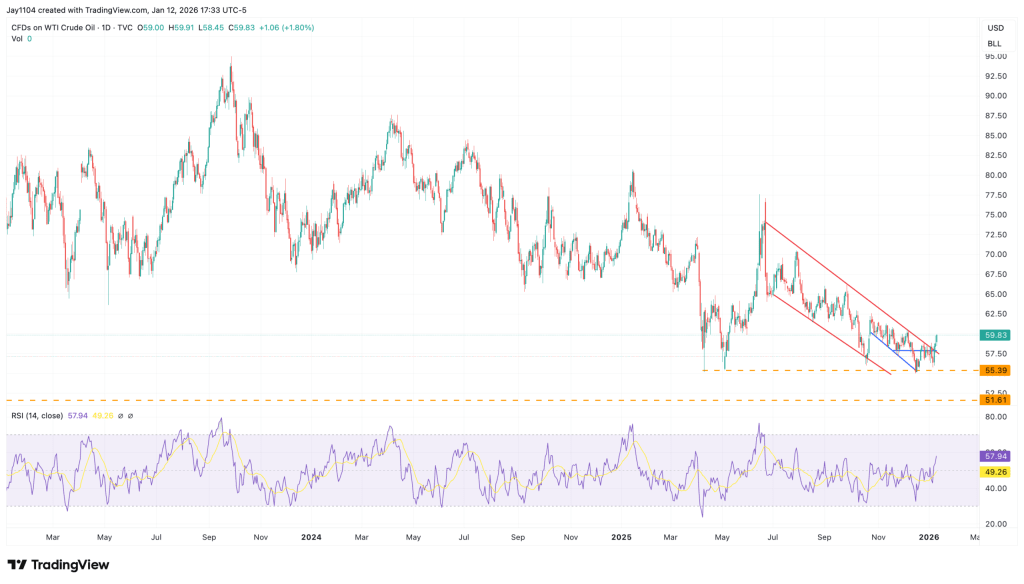

The direction of the 2-year yield may ultimately be more closely linked to oil prices. With inflation still hovering near 3% and crude having fallen to around $60 from highs in the $120s, the message is clear: a rebound in oil prices could quickly reignite inflation pressures. That dynamic likely explains why the price action in oil and the 2-year yield charts has begun to look strikingly similar.

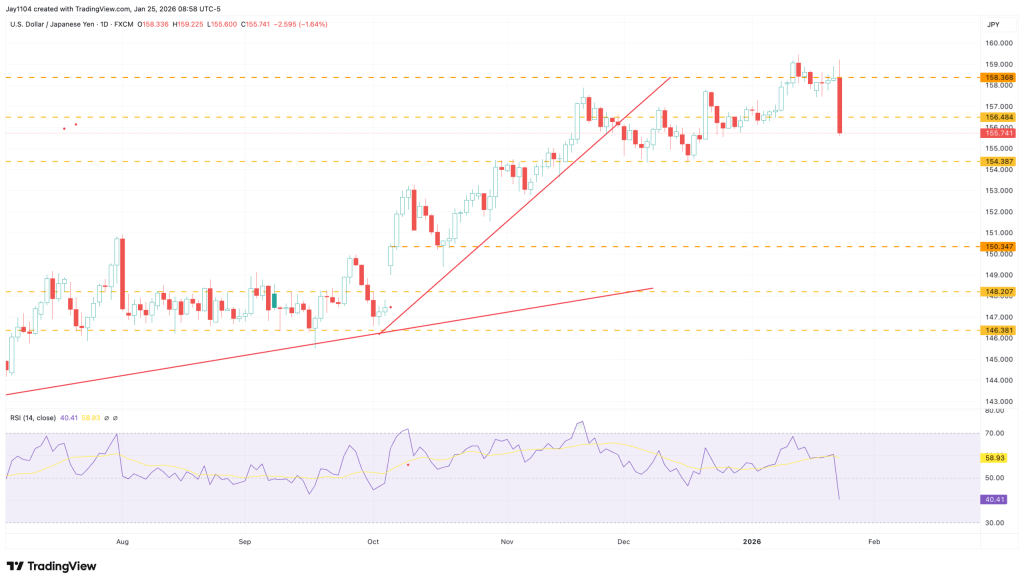

The Bank of Japan once again chose to kick the can down the road, leaving rates unchanged and, in my view, offering little in the way of a clear policy roadmap. The yen’s strength on Friday appeared to be driven solely by reports of a possible “rate check” by the New York Fed on behalf of the U.S. Treasury—widely interpreted as a warning signal that currency intervention could be imminent. Perhaps the strategy is to keep markets stable until after the snap election in February. It’s hard to say, but it should be telling to see how markets react once Japan reopens on Monday.

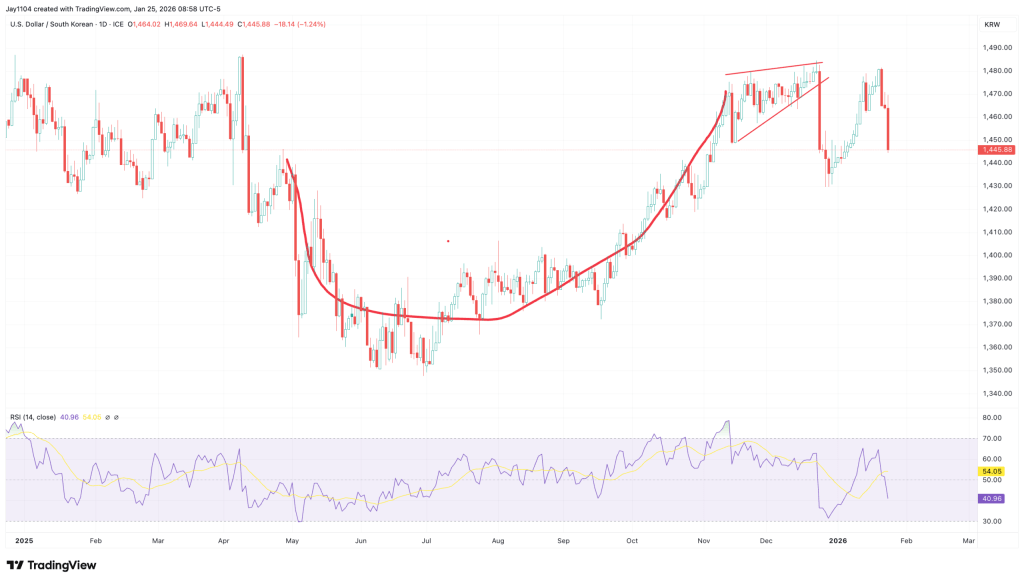

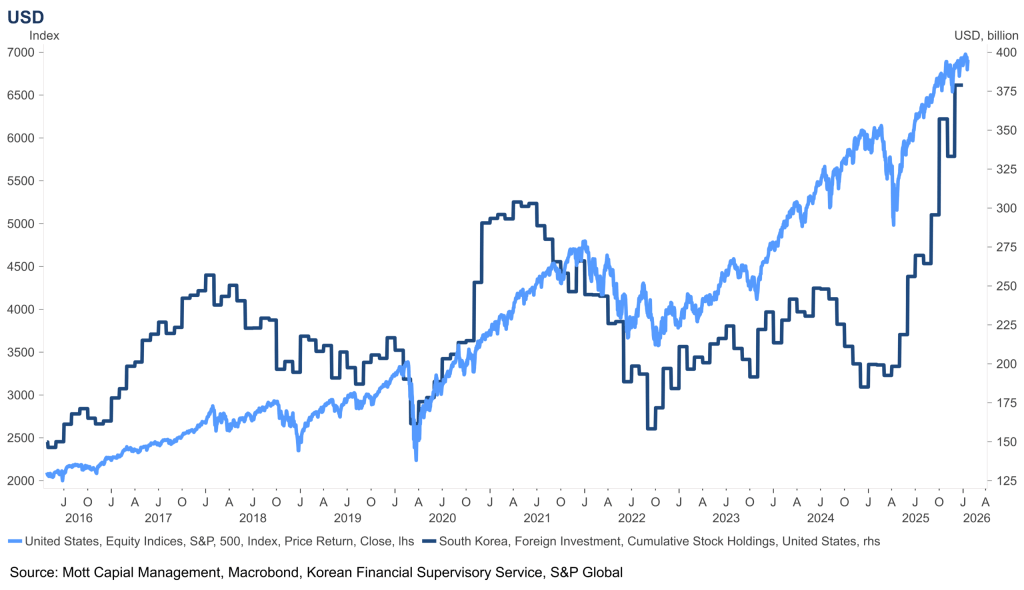

The Korean won also strengthened notably against the U.S. dollar on Friday. In recent weeks, there has been growing chatter that the KRW had become excessively weak, so it’s likely the currency took the developments around the yen as a warning signal and moved to reprice accordingly.

The Korean won likely matters more than many investors realize, given the sizable exposure South Korean investors have built up in U.S. equities. That dynamic is probably one of the reasons the KRW has weakened so significantly in the first place—buying U.S. stocks requires selling won for dollars.

If the KRW begins to strengthen from here, it could start to put pressure on that trade. For investors who are unhedged on the currency side, a stronger won increases the risk of FX-related losses on their U.S. equity holdings, potentially prompting position adjustments.

Of course, this week also brings major earnings reports from Microsoft, Apple, Tesla, and Meta. From what I can see, all four stocks are currently sitting in positive gamma with positive delta positioning. Implied volatility typically builds into earnings because of the event risk, which sets up a familiar dynamic: unless a company delivers truly blowout results, the reaction can easily turn into a sell-the-news move. Once earnings are released, implied volatility collapses and hedges are unwound as delta decays, potentially putting pressure on the shares.

This week’s spotlight will be on the Fed’s FOMC meeting, Chair Powell’s press conference, major Big Tech earnings, and the looming U.S. government shutdown deadline. Apple is set to report earnings after Thursday’s close, with expectations rising for a beat-and-raise quarter. Meanwhile, Starbucks looks like a sell, as profit growth continues to slow and a weaker outlook is anticipated.

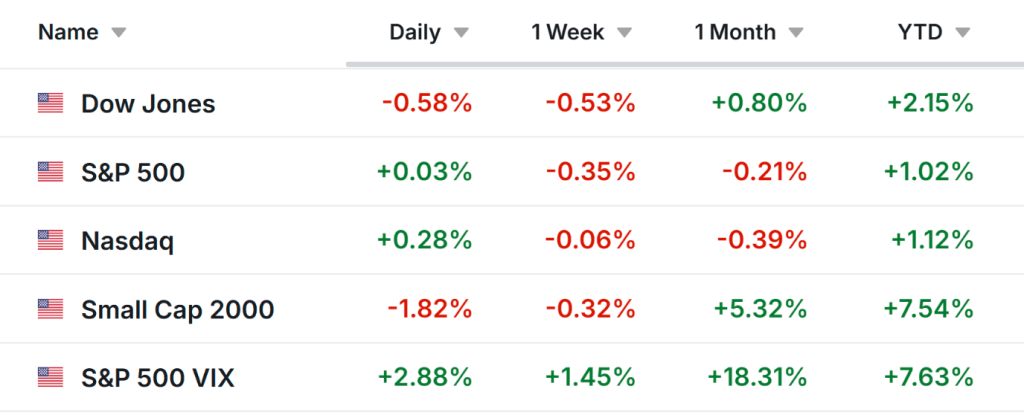

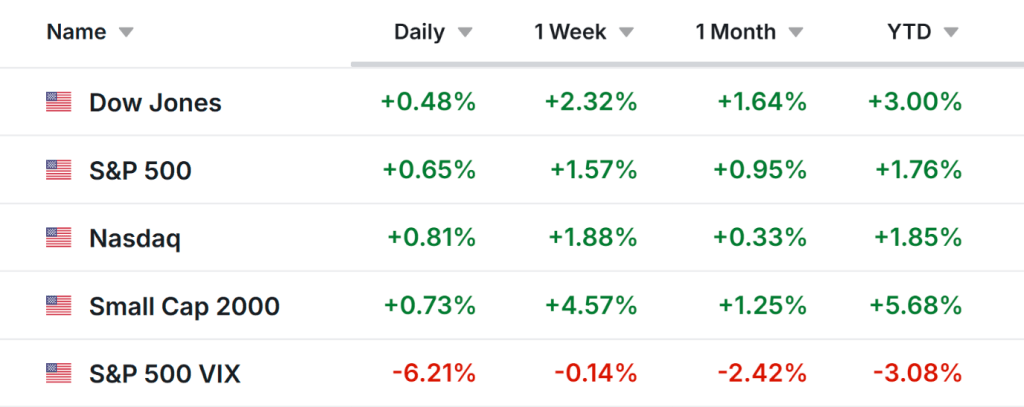

The stock market finished Friday on a mixed note, as both the S&P 500 and Nasdaq Composite recorded their second consecutive weekly declines.

The Dow Jones Industrial Average slipped 0.5% for the week, while the S&P 500 edged down about 0.4%. The tech-heavy Nasdaq fell by less than 0.1%, and the small-cap Russell 2000 lost 0.3%.

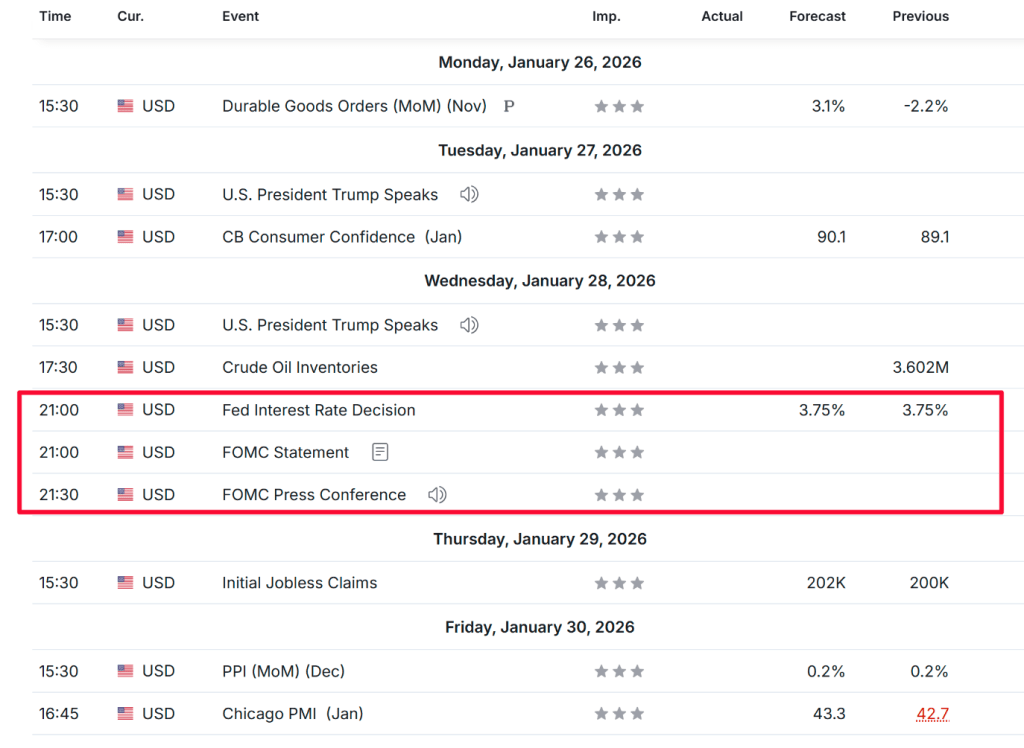

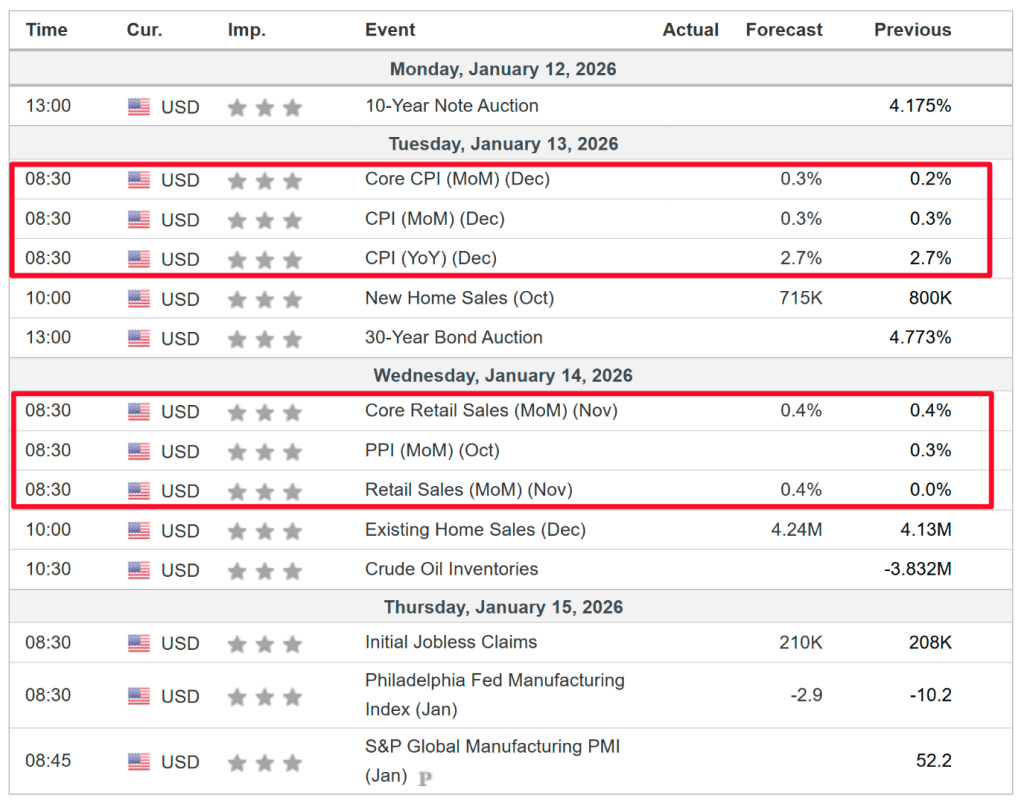

Looking ahead, the coming week is set to be a blockbuster, packed with potential market catalysts. Investors will be watching a crucial Federal Reserve policy meeting alongside a wave of earnings from major technology companies.

The Fed is widely expected to hold interest rates steady on Wednesday, though markets could see volatility as Chair Jerome Powell addresses the media in his post-meeting press conference.

Other key economic releases on the calendar include durable goods orders on Monday and The Conference Board’s Consumer Confidence Index for January on Tuesday. Friday will also bring the release of the December producer price index.

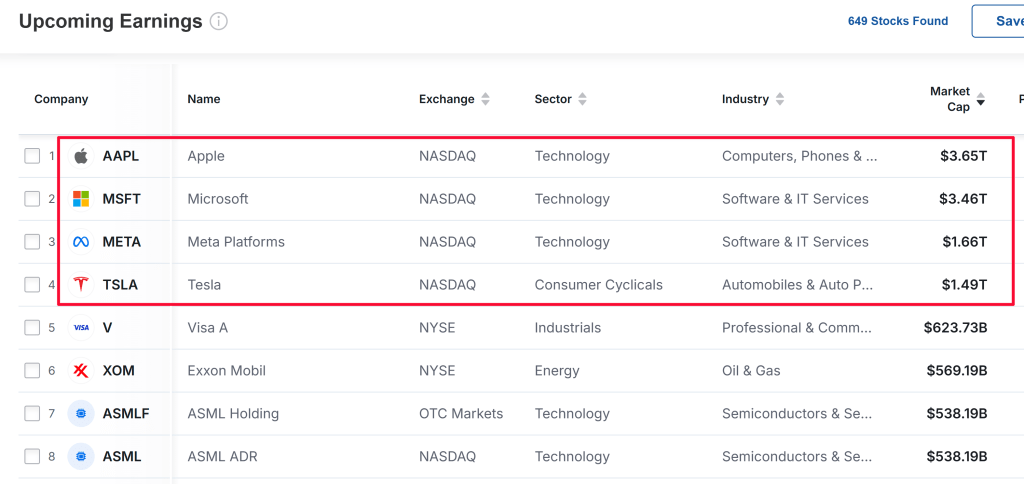

At the same time, earnings season ramps up sharply, with four members of the “Magnificent Seven” set to report this week. Microsoft (NASDAQ:MSFT), Tesla (NASDAQ:TSLA), and Meta Platforms (NASDAQ:META) are scheduled to announce results Wednesday evening, followed by Apple (NASDAQ:AAPL) after the close on Thursday.

These mega-cap names will be joined by a long list of other major companies, including IBM (NYSE:IBM), ASML (NASDAQ:ASML), SanDisk, Exxon Mobil (NYSE:XOM), Chevron (NYSE:CVX), Visa (NYSE:V), Mastercard (NYSE:MA), American Express (NYSE:AXP), SoFi Technologies (NASDAQ:SOFI), UnitedHealth Group (NYSE:UNH), Boeing (NYSE:BA), UPS (NYSE:UPS), Caterpillar (NYSE:CAT), General Motors (NYSE:GM), Verizon (NYSE:VZ), AT&T (NYSE:T), Starbucks (NASDAQ:SBUX), American Airlines (NASDAQ:AAL), RTX (NYSE:RTX), and Lockheed Martin (NYSE:LMT).

Adding to the uncertainty, Congress faces a Friday deadline to fund the government once again, with the risk of a prolonged shutdown looming.

No matter how markets ultimately move, I outline below one stock that could attract strong buying interest and another that may face renewed downside pressure. Keep in mind, this outlook is strictly for the week ahead, from Monday, January 26 through Friday, January 30.

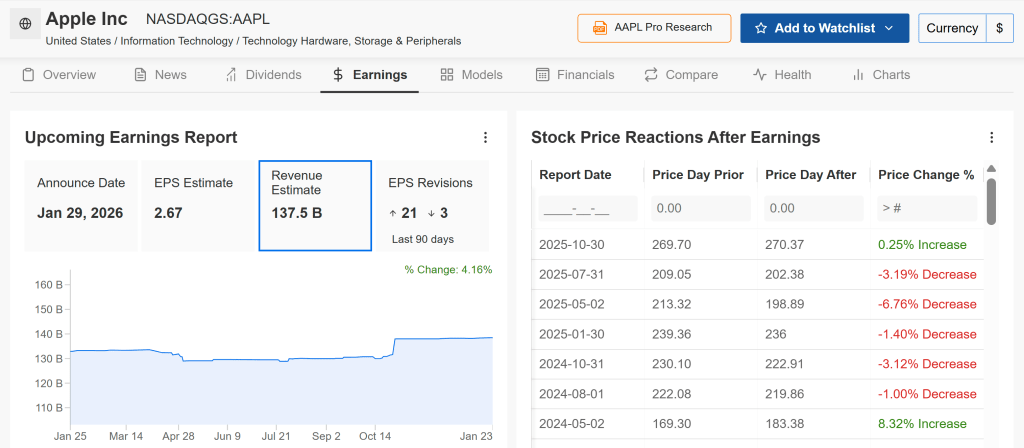

Stock to Buy: Apple

Apple is scheduled to report earnings after the market closes on Thursday, with conditions lining up for a possible upside surprise. Wall Street is increasingly calling for a beat-and-raise quarter, as consensus forecasts point to double-digit revenue growth fueled by steady iPhone demand and continued expansion in services.

Options markets are pricing in a post-earnings move of roughly plus or minus 4%. Meanwhile, earnings expectations have turned more optimistic, with profit estimates revised higher 21 times in recent weeks versus just three downward revisions, according to InvestingPro data—underscoring the growing bullish sentiment surrounding Apple’s results.

Apple is expected to post adjusted earnings of $2.67 per share, representing an 11.2% increase from a year ago, while revenue is projected to climb 10.6% year over year to $137.5 billion. Analysts are looking to the iPhone and Services segments to lead the charge, pointing to double-digit growth and a strong pipeline of upcoming products, including a foldable iPhone and an AI-enhanced Siri.

With sentiment leaning bullish, the market appears positioned for a positive surprise. Price targets reaching as high as $350—implying roughly 41% upside—suggest that even a modest earnings beat could be enough to trigger a rebound in the stock.

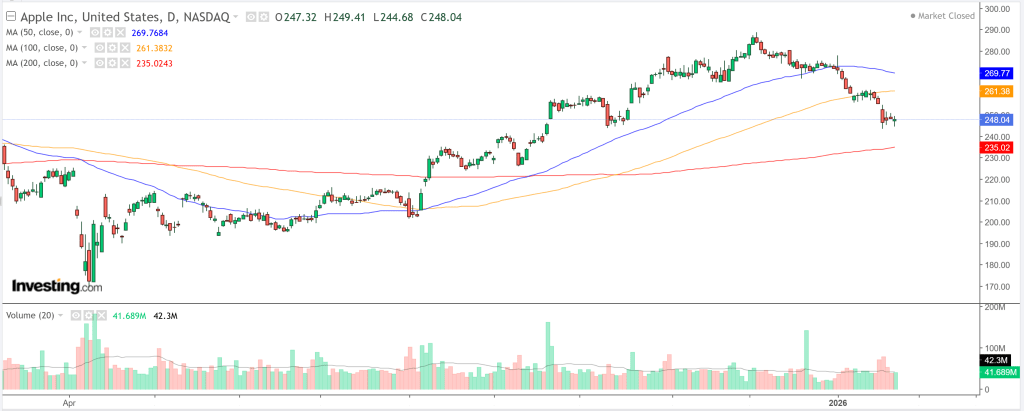

So far in 2026, Apple shares have struggled, falling roughly 9% year to date to finish Friday at $248.04. The decline has mirrored broader volatility across the tech sector, alongside investor concerns that Apple’s AI strategy may be lagging rivals such as Alphabet.

That said, the recent pullback is shaping up as a potential buying opportunity. The stock is trading in deeply oversold territory, and while daily technical indicators still signal a “Strong Sell,” key support sits near $247.53 (pivot S1). A decisive move above resistance at $248.87 could open the door to a rebound toward $260 or higher, particularly if earnings guidance exceeds expectations.

Trade Setup:

Entry: $248 (pre-earnings)

Target: $265 (gain ~7%)

Stop-Loss: $240 (risk ~3%)

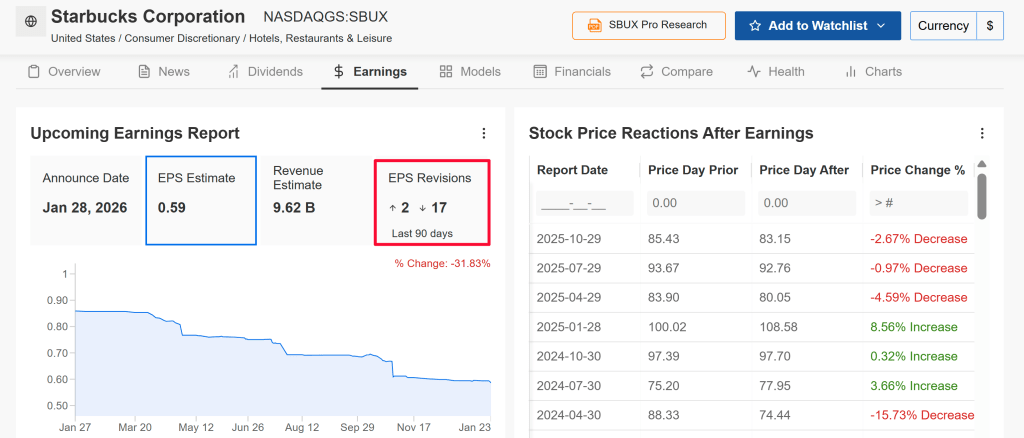

Stock to Sell: Starbucks

Starbucks is set to report earnings Wednesday morning, but unlike Apple, it heads into the week on much shakier footing. The coffee chain is grappling with slowing same-store sales in core markets, intensifying competition, changing consumer spending habits, and persistent cost pressures from labor and commodities.

Options markets are pricing in a post-earnings move of about plus or minus 6.4%, highlighting elevated downside risk. Sentiment has also turned notably bearish, with 17 of the 19 analysts tracked by InvestingPro cutting their EPS forecasts over the past three months ahead of the report.

Wall Street is bracing for a difficult quarter, with earnings per share projected to fall 15.9% year over year to $0.59, even as revenue is expected to edge up 2.5% to $9.62 billion.

Starbucks is also contending with intensifying competition from value-focused fast-food chains such as McDonald’s and Dunkin’, alongside pressure from local coffee shops. At the same time, its China growth narrative—once a major upside driver—has increasingly become a source of investor concern.

Looking ahead, expectations are building that CEO Brian Niccol may caution about continued near-term weakness, citing softer customer traffic, higher operating costs, and lingering uncertainty around the company’s turnaround efforts.

So far in 2026, Starbucks has been one of the stronger performers, climbing roughly 16% year to date and closing Friday at $97.62. However, the technical setup suggests the stock may be overextended heading into earnings.

Key pivot support lies near $96.25, with resistance around $97.84. A downside break below support could open the door to a pullback toward the $90 level if earnings or guidance disappoint.

Asian equities traded mixed on Monday as investors positioned ahead of a pivotal Federal Reserve policy meeting later this week and awaited major technology earnings, while Japanese shares fell sharply as the yen strengthened.

U.S. stock indexes ended last week lower, and futures linked to Wall Street declined further during Asian trading on Monday.

Nikkei tumbles as yen surges

Japan’s Nikkei 225 fell nearly 2%, deepening losses in exporter stocks as the yen strengthened sharply against the U.S. dollar amid speculation that Japanese and U.S. officials could intervene in currency markets to support the battered currency.

A firmer yen typically weighs on Japanese exporters’ overseas earnings, reinforcing risk-off sentiment in Tokyo. Meanwhile, gold surged to record highs as safe-haven demand intensified, underscoring investor caution ahead of major global policy decisions.

Elsewhere in Asia, South Korea’s KOSPI slipped nearly 1% after touching an intraday record of 5,023.76 points, while China’s Shanghai Composite was little changed.

Australia’s S&P/ASX 200 added 0.1%, while Singapore’s Straits Times Index fell 0.4%.

Indian markets were closed for a public holiday.

Fed meeting and packed tech earnings slate in focus

Traders are firmly focused on this week’s Federal Reserve meeting, where officials are broadly expected to keep interest rates unchanged, with markets closely watching for any adjustment in forward guidance on future policy moves as inflation pressures persist. Remarks from Fed Chair Jerome Powell and other policymakers later in the week are likely to influence sentiment across global risk assets.

Investor attention is also fixed on a packed earnings calendar, featuring quarterly results from most of the so-called “Magnificent Seven” technology heavyweights, including Microsoft Corp (NASDAQ:MSFT), Meta Platforms Inc (NASDAQ:META), Tesla Inc (NASDAQ:TSLA) and Apple Inc (NASDAQ:AAPL), whose results often set the tone for wider markets.

In Asia, major technology names such as Samsung Electronics (KS:005930) and SK Hynix Inc (KS:000660) are also scheduled to report earnings.

Caution around AI-related stocks remains, with technology shares underperforming in some sessions amid growing concerns over elevated valuations and rising costs.

Overall, market participants remain guarded ahead of key policy and earnings catalysts, weighing optimism over artificial-intelligence-driven long-term growth against near-term macroeconomic and currency risks.

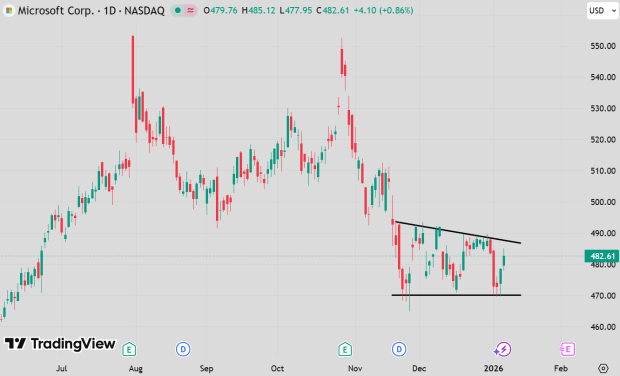

Jefferies says Microsoft’s recent pullback presents an attractive entry opportunity

Jefferies analyst Brent Thill wrote this week that the recent pullback in Microsoft Corporation (NASDAQ: MSFT) shares has created an attractive buying opportunity. He highlighted the company’s expanding backlog, deepening AI partnerships, and continued strength in cloud computing as the foundations of a robust multi-year growth outlook among large-cap technology names.

Thill noted that the stock has declined about 18% since the first fiscal quarter, despite Microsoft disclosing roughly $250 billion in commitments to OpenAI and an additional $30 billion linked to Anthropic. He added that Microsoft’s current valuation—around 23 times calendar-year 2027 earnings—now trades below that of Amazon and Google, even though Microsoft offers what he sees as superior earnings visibility.

According to Thill, Microsoft’s record level of contractual commitments is the primary catalyst for buying at current prices. He expects second-quarter remaining performance obligations to show the largest sequential increase on record, driven largely by the OpenAI and Anthropic agreements, which he says provide “unprecedented multi-year demand visibility.”

Azure remains a central source of upside. Thill described Azure demand as constrained by supply rather than demand, noting that Microsoft plans to double its data-center capacity over the next two years. After beating Azure revenue guidance for three straight quarters, he believes that execution on new capacity alone could push results above consensus expectations for both fiscal second-quarter Azure performance and full-year 2026 forecasts.

The analyst also pointed to accelerating AI monetisation from Copilot and other first-party products. With Azure representing roughly 30% of total revenue, he said sustained outperformance in the cloud business could push overall revenue growth into the high-teens.

Although Thill acknowledged ongoing capacity constraints and elevated capital expenditures, he believes Microsoft is well positioned to generate meaningful upside to both revenue and earnings through fiscal 2026.

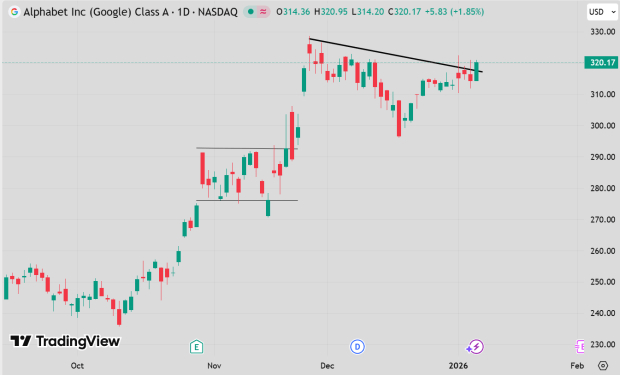

Analyst upgrades Google to Strong Buy as AI stack accelerates

Earlier this week, Raymond James upgraded Google parent Alphabet (NASDAQ: GOOGL) to Strong Buy, arguing that the company is entering a phase in which its AI stack is “shifting into high gear,” creating the conditions for meaningful upward revisions to medium-term forecasts.

Analyst Josh Beck said updated bottom-up analysis across Search and Google Cloud Platform (GCP) led him to raise his 2026 and 2027 estimates, with his 2027 revenue projection now exceeding broader Street expectations. He believes Alphabet is “entering a cycle of strengthening AI stack momentum and upward estimate revisions that could produce one of the highest-quality top-line AI acceleration stories in the public markets.”

Beck added that in 2026, the AI stack narrative and related forecast upgrades are likely to become the primary performance drivers among mega-cap internet stocks, rather than a simple mean-reversion trade.

Within Cloud, Beck projects GCP revenue growth of 44% in 2026 and 36% in 2027, ahead of consensus. He attributes this to strong momentum in infrastructure and platform services, underpinned by large-scale TPU and GPU deployments and increasing adoption of the Gemini API and Vertex AI.

By the end of 2027, Beck estimates that GCP could generate approximately $25 billion in annualised revenue from TPUs, around $20 billion from GPUs, about $10 billion from the Gemini API, and roughly $2.5 billion from Vertex AI.

In Search, Beck projects revenue growth of 13% in both 2026 and 2027—above broader Street expectations—as softness in core search is offset by the expanding adoption of AI Overviews, AI Mode, and Gemini. He expects AI-driven queries to drive stronger cost-per-click growth as improved context and conversion rates enhance monetisation.

Stifel starts Micron at Outperform, citing a multi-year memory market upturn

Brokerage firm Stifel initiated coverage of Micron Technology with an Outperform rating, arguing that the memory industry is entering a multi-year upcycle driven by structural AI demand and persistently tight supply conditions.

Stifel believes Micron is well positioned to benefit from rising average selling prices and a favorable mix shift toward higher-margin products, as memory increasingly becomes a critical constraint within AI systems. “Access to memory has emerged as a key bottleneck in AI racks and systems, boosting demand for higher-performance, higher-bandwidth memory solutions,” the firm said.

With supply expected to remain constrained through 2027, Stifel sees an environment supportive of sustained pricing power and margin expansion. Against this backdrop, the firm expects Micron to capture significant ASP growth and expand margins, forecasting non-GAAP EPS growth of more than 275% over the next two years.

High-bandwidth memory (HBM) is central to Micron’s growth thesis, according to Stifel. As AI models become more complex and require faster access to larger data sets, next-generation chips are incorporating more HBM, increasing memory’s share of overall AI infrastructure spending. As the industry’s number-two player, Micron is expected to see HBM revenue grow 164% in fiscal 2026 and a further 40% in fiscal 2027, with DDR and QLC NAND also benefiting from AI-driven demand.

Stifel also highlighted several risks, including the potential re-emergence of Samsung as a more formidable HBM competitor, elevated capital spending that could shift value toward equipment suppliers, a possible easing in DRAM supply-demand dynamics, and the risk that chipmakers design their own base logic dies.

On valuation, Stifel noted that Micron trades at roughly 9.7 times calendar 2026 earnings, modestly below historical averages. “While valuation increasingly reflects significant growth expectations, we believe the shares can continue to perform on the back of a multi-year, AI-driven product cycle characterized by tight supply,” the firm concluded.

Mizuho says Arm selloff presents a buying opportunity

Mizuho analyst Vijay Rakesh said investors should take advantage of the recent pullback in Arm Holdings shares to build positions, arguing that market concerns around handset demand have become excessively pessimistic.

Arm’s stock has declined roughly 30% since November, even as the Philadelphia Semiconductor Index has risen about 10%. Rakesh described the selloff as “overdone,” adding that Mizuho would “be buyers of ARM on the approximately 30% pullback.”

According to Rakesh, Arm’s growth drivers extend well beyond smartphones. While mobile royalties account for about 50% of revenue, he noted that Arm has historically outpaced handset market growth and is projected to expand at annual rates of 7% to 31% between 2021 and 2027.

A key catalyst is the ongoing transition to Arm’s v9 architecture, which delivers roughly double the average selling price per core compared with v8, providing a structural uplift to royalty revenue. Rakesh also highlighted rising interest in custom silicon, noting that potential ASIC and CPU ramps in 2027 and 2028 could contribute more than $1 billion in incremental revenue.

He further pointed to opportunities tied to AI-focused custom chips, including a potential training and inference ASIC associated with OpenAI and SoftBank. That initiative alone, he said, could conservatively generate around $1 billion in revenue during the 2027–2028 period.

Beyond mobile, Arm is gaining traction in data centers as hyperscalers increasingly adopt its architectures. Rakesh cited platforms such as AWS Graviton, Microsoft Cobalt, Meta’s planned CPU, and Nvidia’s Grace and Vera as evidence of a growing custom silicon customer base and an improving royalty mix.

Rakesh reiterated Mizuho’s Outperform rating and $190 price target, saying Arm remains “well positioned as the broadest global semiconductor platform.”

Morgan Stanley grows more positive on European semiconductor stocks

Morgan Stanley upgraded the European semiconductor sector to Overweight this week, arguing that the group offers an attractive environment for selective stock picking as diversification inflows gather pace, valuation dynamics improve, and semiconductor equipment companies stand to benefit from the next phase of the AI capital expenditure cycle.

The firm’s strategists noted that European equities are attracting increased diversification inflows while beginning to emerge from a long-standing valuation discount to U.S. markets. Within this context, semiconductors stand out as a sector where strengthening bottom-up fundamentals are increasingly driving top-down performance. Morgan Stanley said its preferred expression of this view remains analyst-led stock selection rather than broad factor exposure.

“While European equities already appear highly idiosyncratic, we see further scope for stock-level dispersion in Europe to rise toward cycle highs,” the strategists wrote.

The upgrade is anchored in the semiconductor equipment segment. Morgan Stanley highlighted ASML as the dominant contributor to European Top Picks performance year to date, accounting for more than half of weighted gains. ASML also represents roughly 80% of the MSCI Europe Semiconductors and Semiconductor Equipment index.

Looking ahead, the bank said risks in the AI investment cycle are shifting away from demand and toward execution and transition. “For 2026, the key risk in the AI capex cycle is execution and transition, not demand,” the strategists wrote, arguing that this dynamic favors European semiconductor equipment exposure—particularly companies tied to extreme ultraviolet lithography.

Morgan Stanley expects upcoming order intake to confirm higher foundry and memory capital spending through 2027, alongside stronger-than-expected demand from China.

From a portfolio construction standpoint, the firm said it adjusted its sector model to reflect improving earnings momentum and broader price-target revisions for European semiconductors, while neutralising accrual factors and reducing China exposure. These changes lifted the sector to second place in Morgan Stanley’s internal rankings, just behind banks.

At the stock level, ASML and ASM International remain Morgan Stanley’s Top Picks, with BE Semiconductor Industries also highlighted as an Overweight-rated beneficiary of the same themes.

When Tesla introduced the Semi in 2017, it billed the vehicle as a game-changer for the heavy-duty trucking industry. Almost ten years on, however, only a limited fleet is in operation. Repeated production delays and Tesla’s focus on higher-visibility ventures such as passenger cars, AI, and robotics have kept the Semi on the sidelines. Still, 2026 could prove to be the decisive year in determining whether the truck can evolve from a pilot project into a viable commercial offering.

Worldwide sales of heavy-duty trucks reached roughly 2.8 million units in 2024, including about 400,000 in the U.S. Yet electrification in the Class 8 segment remains minimal, as fleet operators tend to prioritise total cost of ownership over branding or technological novelty.

Tesla argues that the Semi offers a strong economic proposition, citing a claimed 500-mile range from an approximately 850 kWh battery, ultra-fast charging rates of up to 1.2 MW, and significantly lower energy and maintenance costs compared with diesel alternatives. Elon Musk has repeatedly characterised demand as “ridiculous” and the business case as a “no-brainer” for fleet operators.

On paper, momentum appears to be building. Filings associated with California’s electric-truck incentive programme indicate that nearly 900 Semis were applied for in 2025—more than any traditional truck manufacturer has historically secured. Early customers, including DHL and RoadOne, report performance exceeding expectations and have signalled intentions to expand their fleets once mass production begins.

Execution risks, however, remain substantial. Tesla is aiming for annual output of up to 50,000 units from its Nevada facility by the end of 2026, a lofty target given that the entire U.S. day-cab tractor market totals fewer than 100,000 units per year. Additional concerns include battery supply constraints following a significant writedown by a major 4680-cell supplier, while drone footage suggests the Nevada production line is not yet fully installed.

Bernstein analysts also caution that, based on current assumptions, the Semi’s total cost of ownership may still marginally exceed that of best-in-class diesel trucks.

For established manufacturers such as Daimler, Volvo, and Paccar, Tesla’s influence is unlikely to be felt immediately. Diesel-powered trucks continue to dominate the market, and the electrification of long-haul freight is expected to progress gradually.

However, if Tesla succeeds in scaling production in 2026, the Semi could alter industry perceptions, prompting increased investment and putting pressure on margins within one of the sector’s most important profit pools.

Monday – U.S. markets were closed for Martin Luther King Jr. Day.

Ciena Corp

What happened? On Tuesday, Bank of America lowered its rating on Ciena Corp. (NYSE: CIEN) to Neutral and set a price target of $260.

TL;DR: Ciena shares have jumped on strong hyperscaler-driven growth, but BofA turned more cautious due to concerns over potential backlog risks.

What’s the full story? Ciena’s shares have surged to record levels, now trading at roughly 40x forward earnings, about twice its 10-year average, reflecting strong expectations for sustained growth. Demand from hyperscale cloud providers has driven a sharp acceleration in revenue growth—from around 8% to approximately 30% in 1Q26—supported by a $5 billion backlog that provides solid visibility into next year’s revenues.

Analysts believe the current cycle has durability, fueled by rapid expansion in scale-across deployments, which are projected to rise 11-fold to $808 million by 2026, alongside continued leadership in 800G optical technology. Ciena’s market share has increased from 18% in 2024 to 22% in 9M25, with the company commanding roughly 50% share among major cloud providers, driven by its RLS systems and WaveLogic 6 Nano built on 3nm DSP, offering superior power efficiency versus competitors such as Cisco and Marvell.

However, risks remain. The company’s history offers a cautionary example: in 2022, backlog coverage fell sharply—from levels that once covered 96% of revenue to a 38% decline, triggering a 12% drop in the stock. With shares now valued at about 45x earnings, assumptions of peak growth leave little room for disappointment if backlog momentum weakens.

As a result, Bank of America downgraded the stock to Neutral, maintaining a $260 price objective, which implies only around 7% upside, suggesting much of the optimism is already reflected in the valuation.

Ulta Beauty

What happened? On Wednesday, Raymond James upgraded Ulta Beauty Inc. (NASDAQ: ULTA) to Strong Buy and raised its price target to $790.

TL;DR: Raymond James turns more bullish on ULTA, citing earnings upside from growth initiatives despite competitive and execution risks.

What’s the full story? Raymond James upgraded Ulta to Strong Buy from Outperform, lifting its price objective to $790 and modestly increasing its FY26 EPS forecast to $28.60 from $28.51. The firm sees a combination of strategic initiatives reigniting growth as Ulta enters FY26 following a year of restructuring.

Beauty demand remains resilient, while the company benefits from operational improvements implemented over the past year, including a refreshed leadership team, enhancements to its loyalty program, stronger digital capabilities, and expanded assortments in Wellness and Marketplace categories. Looking ahead, Raymond James highlights opportunities from deeper data analytics, adoption of agentic AI, and early-stage international expansion—initiatives expected to drive earnings growth without relying on valuation multiple expansion.

The firm believes Ulta is transitioning from an investment phase toward a period of return realization, with contributions expected across physical stores, e-commerce, and potential international markets. However, risks persist, including intensifying competition in beauty retail, potential softness in U.S. consumer demand, rising cost pressures, and execution risks tied to overseas expansion.

Overall, Raymond James views Ulta’s balanced exposure to both prestige and value-conscious consumers, its strong loyalty ecosystem, and improving operational leverage as creating an attractive risk-reward profile, supporting the Strong Buy rating.

Palantir

What happened? On Thursday, PhillipCapital initiated coverage of Palantir Technologies Inc. (NASDAQ: PLTR) with a Buy rating and a $208 price target.

TL;DR: PhillipCapital sees Palantir as a buying opportunity, driven by strong revenue and profit growth, and sets a $208 target.

What’s the full story? PhillipCapital expects Palantir’s FY25 revenue to rise 47% year over year to $4.2 billion, supported by a growing contribution from its commercial segment, which is forecast to expand 51% YoY, outpacing 43% growth in government revenue. The shift reflects accelerating enterprise adoption of AI-driven platforms beyond Palantir’s traditional defense and public-sector base. Net profit is projected to increase by approximately 1.9x, reflecting improving operating leverage.

The U.S. market, which accounts for roughly 66% of total revenue, is expected to remain the key growth driver. Revenue in the region is forecast to grow 66% YoY, supported by elevated government spending amid geopolitical tensions and a sharp acceleration in commercial contracts—nearly doubling in 3Q25—driven by demand for Palantir’s Artificial Intelligence Platform (AIP) and its ontology-based productivity tools.

PhillipCapital’s $208 price objective is derived from a discounted cash flow valuation, assuming an 8.3% WACC, 4.2% risk-free rate, and 8% terminal growth rate. While the stock trades at a lofty ~170x forward P/E, the firm argues this remains below prior peak valuation levels, leaving room for a potential re-rating as earnings visibility improves and Palantir’s addressable markets continue to expand.

Starbucks Co.

What happened? On Friday, William Blair upgraded Starbucks Corporation (NASDAQ: SBUX) to Outperform, without assigning a price target.

TL;DR: William Blair sees an imminent return to positive U.S. comparable sales, prompting an upgrade to Outperform.

What’s the full story? William Blair expects Starbucks to deliver its first positive domestic comparable-sales growth in two years during the December quarter, setting the stage for improved performance into fiscal 2026. While sales momentum is turning, the firm highlights margin recovery as the central investment debate. Americas operating margins are projected to fall to 13.4% in FY25, down from a peak of 20.8%, with an additional $500 million in labor-related cost pressures anticipated in the following year.

The firm is looking to Starbucks’ January 29 investor day for further clarity, anticipating a multi-year strategy focused on general and administrative cost reductions, productivity initiatives, and sustained comparable-sales growth. Over the longer term, William Blair models approximately 3% global unit growth combined with low-single-digit comparable sales, allowing consolidated margins to gradually approach 2023 levels by 2030.

Under this framework, Starbucks could generate a 15–20% compound annual growth rate in EPS over the next five years. Despite the stock being up roughly 15% year to date, William Blair sees a potential valuation path toward $140+ per share by 2029, based on a 30x multiple applied to $4.70+ in EPS, implying roughly 10% annual share price appreciation, with upside if comparable sales accelerate faster than expected.

As a result, William Blair upgraded Starbucks to Outperform, arguing that the recovery in sales is likely to precede and ultimately drive a more meaningful rebound in profitability beginning around 2027.

Shares of Apple (NASDAQ: AAPL) have come under sustained selling pressure, with the stock now trading around $245—nearly 15% below the record high reached just last month. The decline has been largely one-way, which is notable given Apple’s reputation as one of the market’s most reliable large-cap names. Broader market conditions have also weighed on the stock, as escalating geopolitical tensions have fueled a sharp risk-off move across equities in recent days.

What makes the current situation particularly striking is how stretched Apple’s technical signals have become. The stock’s relative strength index (RSI) has fallen into deeply oversold territory this month, currently hovering near 18—its lowest level since September 2008. Such an extreme reading suggests that selling may have been excessive and overly rapid, especially with the company’s earnings report scheduled for next week.

Understanding the Setup as Apple Heads Toward Earnings

An RSI reading this depressed would draw attention for any stock, especially one like Apple. With the company heading into a closely watched earnings report next week, the setup becomes even more compelling.

Apple has a well-established history of beating analysts’ expectations on a quarterly basis, and viewed through that lens, the current situation raises an important question. After such an aggressive sell-off, is it possible that the market has already priced in a worst-case outcome?

Apple’s Fundamentals Still Strengthen the Bullish Case

From a business perspective, Apple’s recent share price performance appears increasingly out of step with its underlying fundamentals. The company’s consistent ability to exceed earnings expectations is something few of its peers can rival. Gross margins remain solid, and its ecosystem-based model continues to deliver dependable cash flows.

Apple’s approach to returning capital also offers a meaningful buffer for investors considering an entry. A sizable share repurchase program alongside steady dividend growth means management is a regular buyer of its own stock during periods of weakness. While this doesn’t eliminate the risk of sharp pullbacks, it often helps prevent negative sentiment from persisting for long.

That said, the concerns driving the sell-off cannot be ignored. iPhone shipment volumes have softened, and the stock’s valuation is near the upper end of its recent range. These factors help explain investor caution, but they fall short of fully justifying the speed and magnitude of the recent decline.

Analyst Confidence Grows Ahead of Apple’s Earnings

The case for buying the dip is reinforced by steadfast analyst support for Apple. This week, Evercore added the stock to its tactical outperform list ahead of next week’s earnings, reflecting confidence that the company will deliver results above expectations.

Recent analyst commentary has focused on the composition of iPhone sales, with higher-end models reportedly making up a greater share of demand. This trend supports both average selling prices and margins. Meanwhile, services revenue is expected to continue providing a stable source of growth, helping to cushion any weakness in hardware volumes.

Evercore set a new price target of $330 for Apple, implying roughly 35% upside from current levels, and that still isn’t the most optimistic view on the Street. Wedbush released a bullish update last week, assigning a $350 price target and further supporting the argument that the market’s reaction has been excessive. With momentum already deeply washed out, even a modest beat on revenue or earnings could be enough to spark a meaningful shift in sentiment.

Apple’s Risk/Reward Looks Compelling at Current Prices

None of this suggests Apple is without risk. Next week’s earnings will carry more weight than usual, and a true disappointment could drive the stock lower—particularly if geopolitical tensions intensify.

That said, the risk/reward profile is becoming increasingly asymmetric. This is the most oversold Apple has been in nearly two decades, and for a company with its balance sheet strength, margin profile, and history of delivering shareholder returns, it’s difficult to ignore the appeal of buying at these levels.

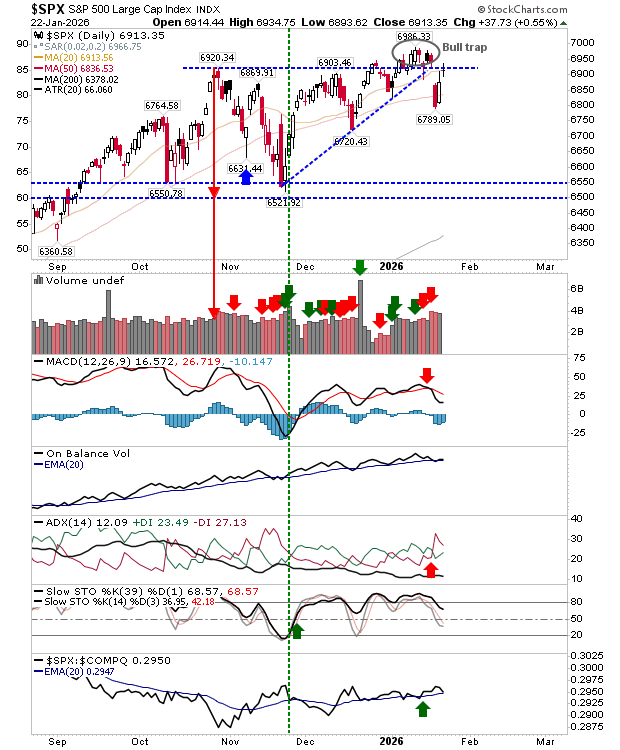

Markets managed to rebound after Tuesday’s sell-off, but the bounce—despite attracting attention—fell short of fully recouping the earlier losses. More importantly, a significant “bull trap” remains in place for the S&P 500. Technical signals for the index continue to be mixed, with momentum indicators such as stochastics failing to move back into overbought territory—a key condition needed to support a sustained rally.

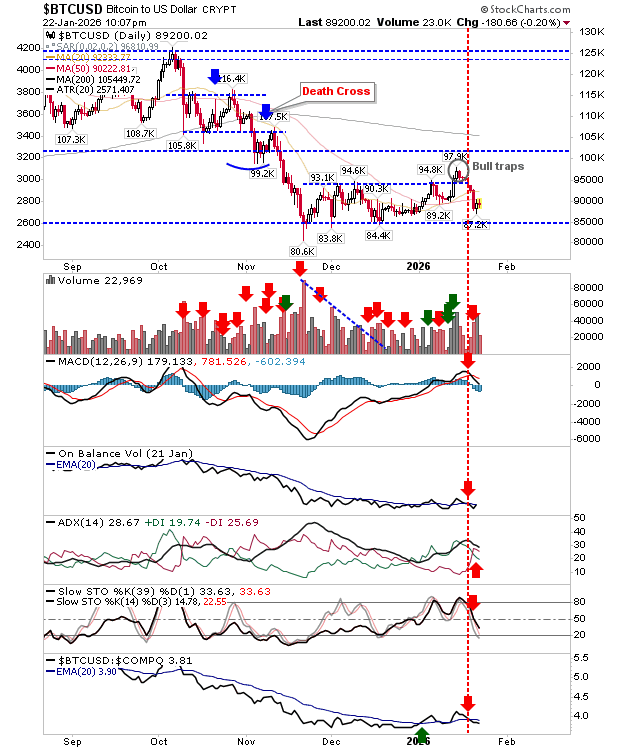

Bitcoin faces more significant challenges. Yesterday’s rise alone is far from sufficient to undo what was beginning to resemble the formation of a right-hand base. That said, this still appears to be the early stages of building a new base and could represent an attractive buying opportunity for investors willing to hold through what may be a year-long process, potentially targeting a move toward $125K. For now, technical indicators remain net bearish, and a break below $85K would invalidate any bullish outlook.

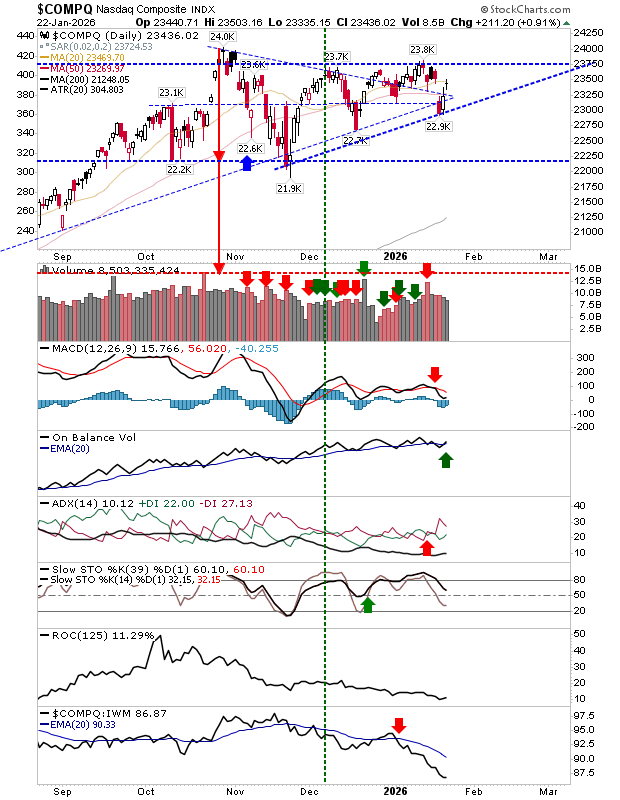

The Nasdaq has mounted a counter-trend bounce following the breakdown, but the symmetrical triangle pattern has already resolved, meaning attention now shifts to identifying new support and resistance levels. There is still a potential bullish scenario if price action evolves into a bullish ascending triangle.

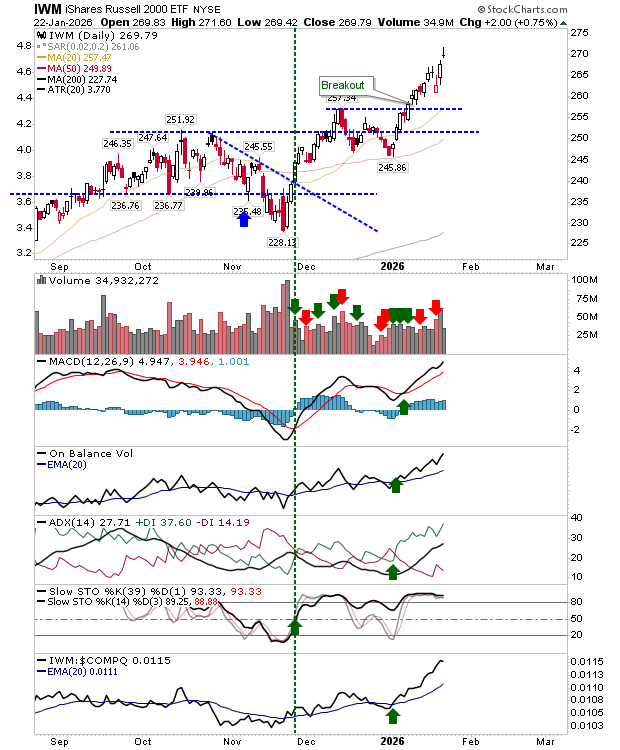

On the other hand, the Russell 2000 shows the potential to form a bearish “evening star” pattern, though this would require a gap lower today. Setting that possibility aside, the index remains firmly in rally mode and is far from any “bull trap” conditions. Overall, technical indicators are net bullish.

For today, bulls may want to focus on Bitcoin, while bears should monitor the Russell 2000 for signs that a bearish “evening star” pattern could emerge.

Geopolitical tensions are rising as President Trump moves ahead with threats to levy tariffs on eight NATO allies while continuing his push regarding Greenland. Although overall markets have weakened, these frictions may spur higher defense budgets, accelerated resource reshoring, and expanded infrastructure investment. Below, we identify five U.S.-based companies that stand to gain from the intensifying U.S.–NATO standoff.

As tensions between the U.S. and NATO escalate over fresh tariffs and Greenland’s strategic resource base, defense, mining, and industrial shares appear well positioned for a strong upswing. Against this backdrop, five companies stand out—Lockheed Martin (NYSE:LMT), RTX (NYSE:RTX), Critical Metals (NASDAQ:CRML), Teck Resources (NYSE:TECK), and Caterpillar (NYSE:CAT). Each is set to benefit from increased U.S. defense spending, intensifying competition for Arctic resources, and ongoing efforts to shift supply chains away from Europe and China.

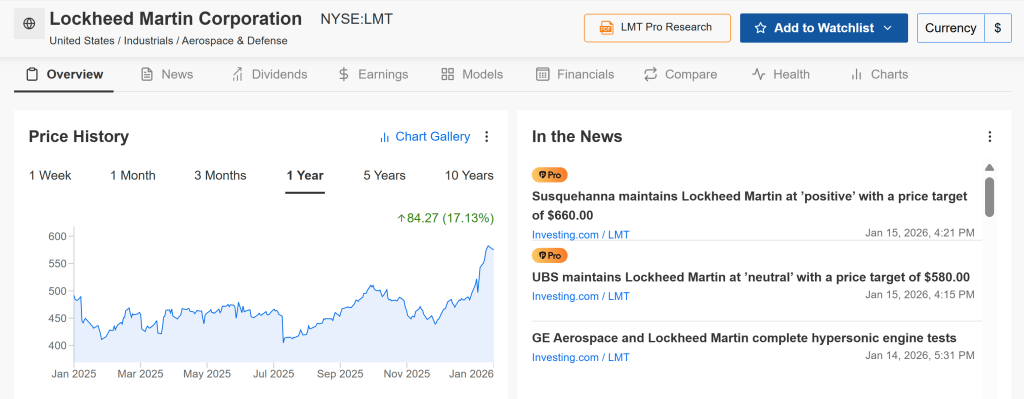

Lockheed Martin: A Leader in Arctic Defense Capabilities

Lockheed Martin appears to be among the primary beneficiaries of rising U.S.–NATO tensions, particularly as Greenland’s strategic value elevates the need for enhanced Arctic defense capabilities. The company’s advanced military platforms and surveillance systems are well suited to the region’s demanding operational environment.

Its F-35 fighter aircraft, along with missile defense and radar solutions such as the “Golden Dome,” play a central role in Arctic security, where Greenland’s geographic position strengthens U.S. monitoring capacity and deterrence against potential Russian and Chinese advances.

So far in 2026, Lockheed Martin’s shares are up roughly 19% year to date, supported by President Trump’s proposed $1.5 trillion defense budget for 2027, which points to expanded procurement activity. In periods of sustained geopolitical strain, investors typically favor companies with stable revenues and long-term contracts. Against this backdrop, Lockheed’s robust order backlog, strong free cash flow generation, and reliable dividend profile position it as a traditional “geopolitical hedge” stock.

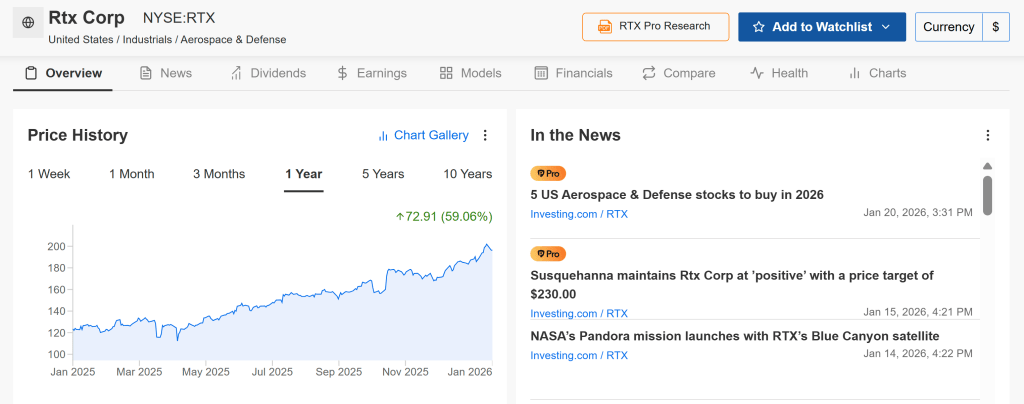

RTX: Rising Demand Across Aerospace and Missile Systems

RTX, formerly known as Raytheon, stands out as a key beneficiary due to its broad defense technology portfolio tailored to the demanding requirements of Arctic environments. The company’s missile defense and advanced radar solutions are central to securing and monitoring strategically vital regions such as Greenland.

In particular, RTX’s Patriot missile defense system is regaining prominence as governments prioritize battle-tested platforms capable of operating in extreme climates while defending against increasingly sophisticated threats.

RTX shares are up about 7% year to date in 2026, following a strong 60% advance in 2025, with a record backlog of $251 billion underpinning continued momentum.

Looking ahead through the rest of 2026, RTX remains attractive amid rising orders from the Middle East, its inclusion in leading defense-focused ETFs, and expectations for roughly 20% earnings growth.

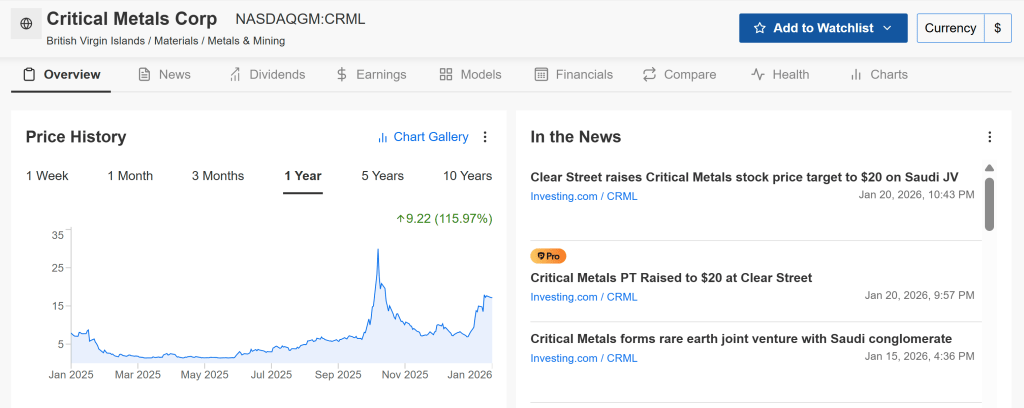

Critical Metals controls the Tanbreez project in Greenland, the largest non-Chinese rare earth deposit globally, directly linking the company to U.S. strategic resource objectives. Heightened geopolitical tensions could accelerate Washington’s push to secure access to these materials, which are essential for defense systems, missile technologies, and electric vehicles—reducing reliance on China and enhancing CRML’s strategic importance.

In addition, the company’s proprietary rare earth processing capabilities and its focus on North American operations position it to benefit from government initiatives aimed at strengthening domestic critical-materials supply chains and expanding strategic mineral stockpiles.

CRML shares have surged nearly 150% so far in 2026, propelled by strong high-grade drilling results and regulatory approval for its pilot processing plant in Greenland.

While the stock carries elevated risk, it offers substantial upside potential this year, with the possibility of capturing up to 50% of the Western rare earth supply. Despite ongoing volatility, secured offtake agreements and heightened U.S. national security priorities support the bullish case, with the stock still trading at an estimated 22% discount to net present value.

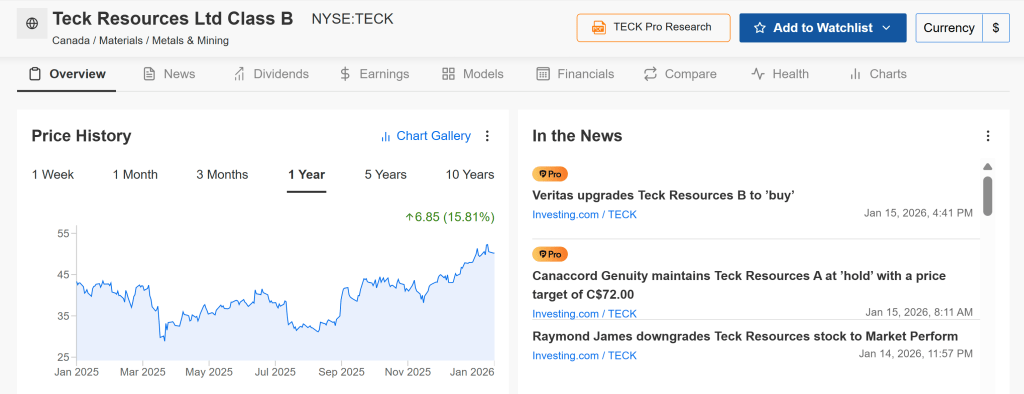

Teck Resources: A Global Metals and Mining Leader

Teck Resources is a leading diversified mining company with significant exposure to steelmaking coal, copper, zinc, and other essential industrial metals. While its operations are not exclusively Arctic-centric, Teck’s asset base firmly places it within the strategic raw materials space that underpins infrastructure development, defense manufacturing, and the global energy transition.

Should 2026 be marked by robust commodity demand, sustained decarbonization spending, and intensifying geopolitical rivalry, diversified miners such as Teck are well positioned to benefit from favorable pricing dynamics and rising shipment volumes.

TECK shares are up roughly 5% year to date, notching fresh 52-week highs as copper prices rally and investors rotate into the materials sector.

Looking ahead, Teck presents a compelling copper-focused opportunity, with its merger with Anglo American set to create a top-five global producer, unlock an estimated $800 million in synergies, and benefit from AI-driven demand growth. Analyst price targets in the $80–90 range are underpinned by structural supply constraints and sustained long-term commodity demand.

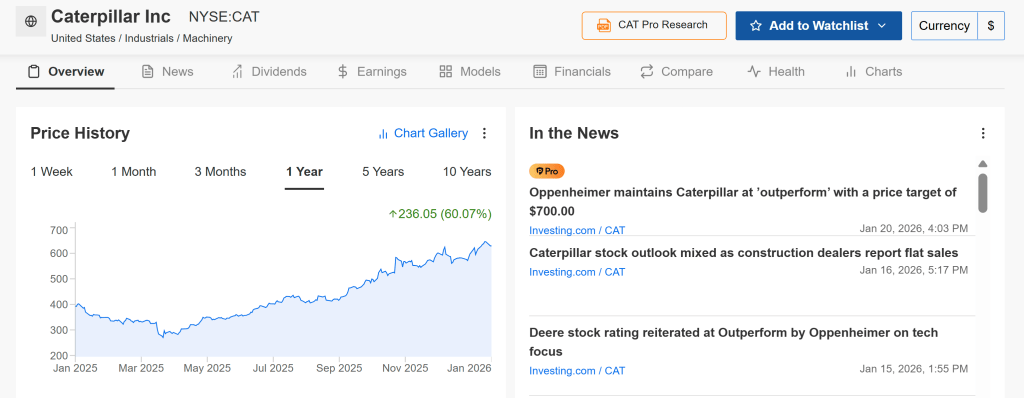

Caterpillar – Infrastructure & Arctic Expansion

Caterpillar stands out as a key beneficiary through its portfolio of heavy machinery and construction equipment critical to Arctic infrastructure expansion, including military installations, transportation networks, and mining projects.

Its specialized cold-weather and Arctic-rated equipment gives Caterpillar a distinct advantage in supporting development across Greenland and other high-latitude regions that gain strategic relevance amid heightened geopolitical tensions.

CAT shares are up roughly 10% year to date in 2026, building on a strong 58% gain in 2025, supported by a record backlog of $39.9 billion.

Looking ahead, Caterpillar remains a solid hold for 2026, with earnings per share projected to grow about 20.5%, aided by continued spending under the U.S. Infrastructure Act and expanding construction tied to AI-driven data center development.

Last week, we kicked off a broad review of the key macro forces shaping the stock market, focusing on the health of the economy and earnings expectations. The takeaway was clear: the economy appears to be in solid shape, and consensus forecasts for earnings growth this year are not just positive, but notably strong.

Admittedly, there has been no shortage of headlines and market volatility since then. It would be reasonable to dive into geopolitical developments, market breadth, or the current state of the AI trade. However, at least for now, none of these factors have altered the market’s primary trend. With that in mind, it makes sense to continue our top-down assessment of the major macro drivers.

Having already examined the economy and earnings, the remaining areas to address are inflation, Federal Reserve policy and interest rates, and market valuations. Let’s turn to those next.

What Is Inflation?

The Federal Reserve defines inflation as a sustained rise in the prices of goods and services over time, reflecting a general increase in the overall price level across the economy. Similarly, Investopedia and standard economics textbooks describe inflation as a gradual erosion of purchasing power, manifested through a broad-based increase in the prices of goods and services over time. The International Monetary Fund frames inflation as the pace at which prices rise over a given period, indicating how much more costly a representative basket of goods and services has become.

Or, as I was taught in my very first economics class many years ago, inflation can be summed up as “too much money chasing too few goods.”

In Focus

There is little doubt that inflation has dominated the attention of the Federal Reserve, policymakers, consumers, and financial markets for several years. Unless one has been completely disconnected from events, it is well known that inflation surged in the aftermath of the COVID crisis, driven by trillions of dollars in government stimulus flowing into household bank accounts and severe disruptions across global supply chains.

This surge fueled fears that the United States was heading back toward the inflationary turmoil of the 1970s—a period the Fed ultimately subdued, but only at significant cost to the economy. With the Consumer Price Index approaching double-digit territory in early 2022, such concerns were understandable.

As the pandemic faded and supply chains normalized, inflationary pressures also began to ease. By early 2024, CPI readings had fallen back near pre-pandemic levels, when face coverings were not yet a cultural norm. The key question now is whether the inflation spike has been fully brought under control.

While corporate pricing strategies and consumer behavior—both central drivers of inflation—are inherently difficult to forecast, it remains possible to analyze the components of the CPI and examine the historical forces that have shaped inflation trends.

A Framework for Understanding Inflation

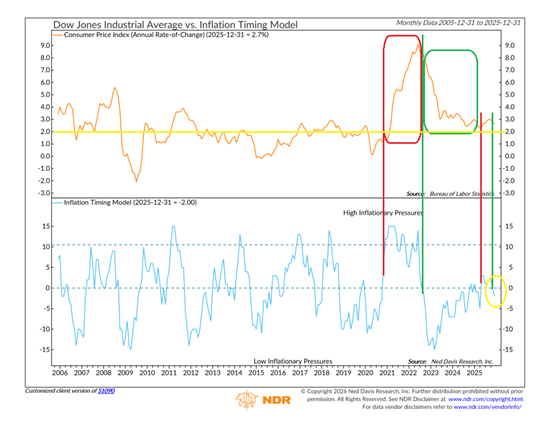

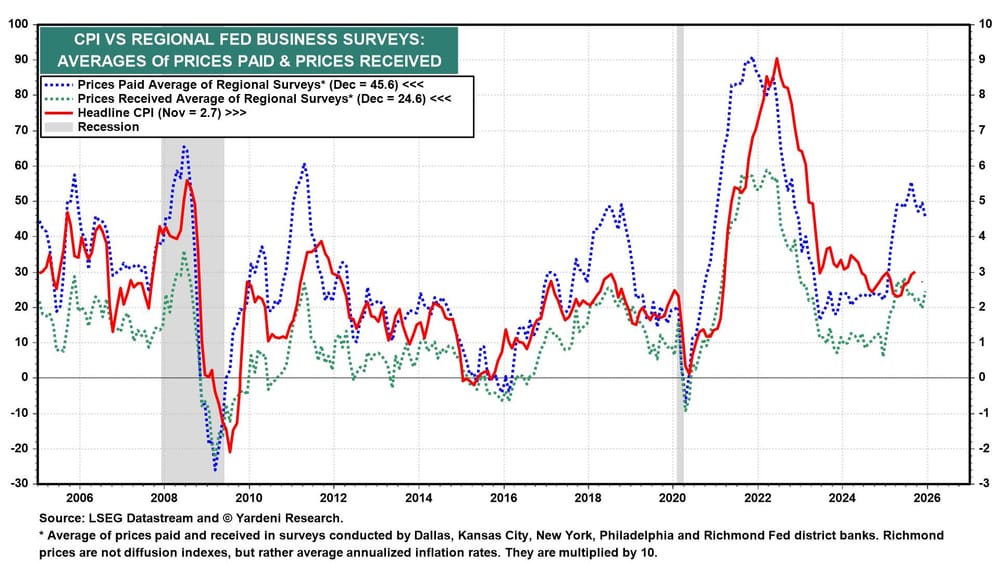

Unsurprisingly, the team at Ned Davis Research Group has already taken this step. In short, there is indeed a model that addresses this—shown below.

The upper chart shows the Consumer Price Index, which represents the inflation rate, while the lower chart displays NDR’s Inflation Timing Model. Reading the model is fairly intuitive. When the blue line rises above zero, it signals that inflation pressures are likely increasing. Historically, readings above 10 have coincided with periods when inflation was significantly above normal levels.

The red box highlights the CPI period from late 2020 through early 2022. During that phase, the model effectively flagged the acceleration in inflation and warned that conditions were set to deteriorate. The model also performed well in the opposite direction in the fall of 2022. While widespread concern about inflation persisted, the model correctly indicated that inflation was poised to ease—and it did.

That downtrend continued until late 2024 or early 2025, when the model briefly suggested inflation was no longer moving in the right direction. However, the signal proved temporary, as the model dropped back below the zero line by the end of 2025. Encouragingly, recent data has validated the model’s current reading, with price pressures generally moderating and the inflation rate falling back below 3%.

Is 3% Becoming the New Inflation Norm?

Inflation skeptics are quick to push back against my relatively calm view, pointing out that inflation remains well above the Federal Reserve’s stated 2% target. From that perspective, they argue the Fed is unlikely to turn accommodative anytime soon. While this logic is understandable, it overlooks two important points: first, the Fed operates under a dual mandate, and second, its preferred inflation gauge—core PCE—differs from the inflation measures most often highlighted in the media.

Crucially, inflation is not the Fed’s sole concern. Maintaining a healthy labor market is equally central to its mission. As a result, the Federal Open Market Committee must carefully balance inflation pressures against broader economic conditions.

This helps explain why the Fed has been cutting interest rates even as inflation remains above target. The labor market has shown signs of weakening, prompting policymakers to act. Equity bulls have welcomed these moves, mindful of the long-standing adage that it rarely pays to fight the Fed. With rates coming down, investors have largely aligned with the bullish camp.

That said, it’s important to recognize that the Fed is not engaged in an aggressive stimulus campaign. Chair Jerome Powell and his colleagues are not attempting to jump-start the economy. Instead, they are seeking to bring interest rates back toward a more neutral, “normal” level—one that balances inflation with labor market stability.

In this context, the prevailing view is that the Fed is willing to tolerate inflation running somewhat above its 2% target while it works to shore up employment conditions. From that standpoint, an inflation rate around 3% may be acceptable—for the time being.

In Summary

The encouraging takeaway is that history suggests a modest amount of inflation can actually be beneficial—supporting stock prices, home values, and corporate earnings. From that perspective, inflation does not appear to be a headwind for equities at present. While this may not be a classic “don’t fight the Fed” environment, the central bank is also not acting as an adversary. As a result, my view is that investors can remain on the bullish path—for now.

U.S. stock index futures edged higher on Tuesday evening after Wall Street suffered sharp losses amid rising geopolitical tensions linked to President Donald Trump’s demands regarding Greenland. Netflix was a notable mover in after-hours trading, sliding nearly 5% after the streaming company issued guidance that disappointed the market.

Futures stabilized following Wall Street’s worst session in three months, as investors grew uneasy over President Trump’s push to acquire Greenland despite resistance from European leaders. S&P 500 futures gained 0.1% to 6,838.0 by 18:27 ET, while Nasdaq 100 and Dow Jones futures also rose 0.1% to 25,152.75 and 48,727.0, respectively.

Netflix falls after issuing a weaker-than-expected outlook; more earnings reports ahead

Netflix Inc (NASDAQ: NFLX) fell 4.8% despite reporting December-quarter earnings that topped market expectations, as its first-quarter guidance disappointed investors. The company pointed to weakening viewership for non-branded licensed content, signaling softer demand beyond its flagship in-house programming. Netflix’s outlook for 2026 also came in below expectations.

The results arrive amid a wave of mixed corporate earnings over the past week, particularly among major U.S. banks. The fourth-quarter earnings season continues in the days ahead, with Johnson & Johnson (NYSE: JNJ), Charles Schwab Corp (NYSE: SCHW), and Prologis Inc (NYSE: PLD) scheduled to report on Wednesday.

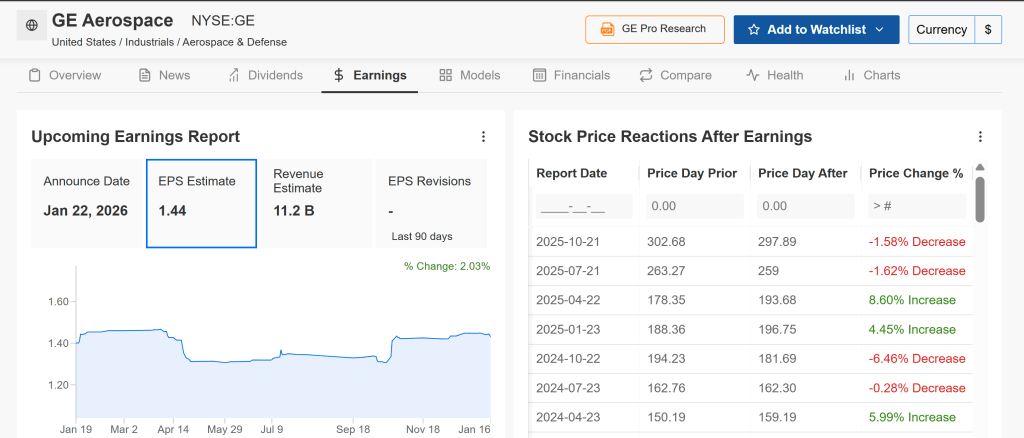

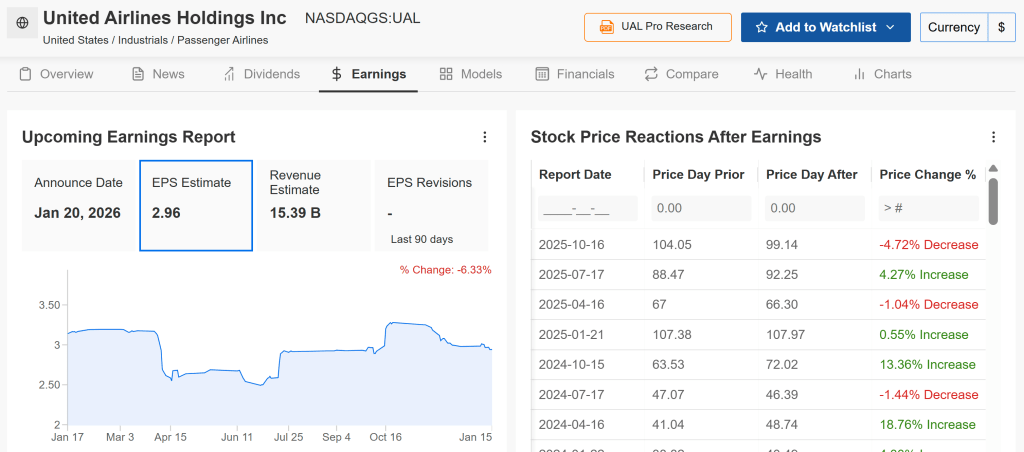

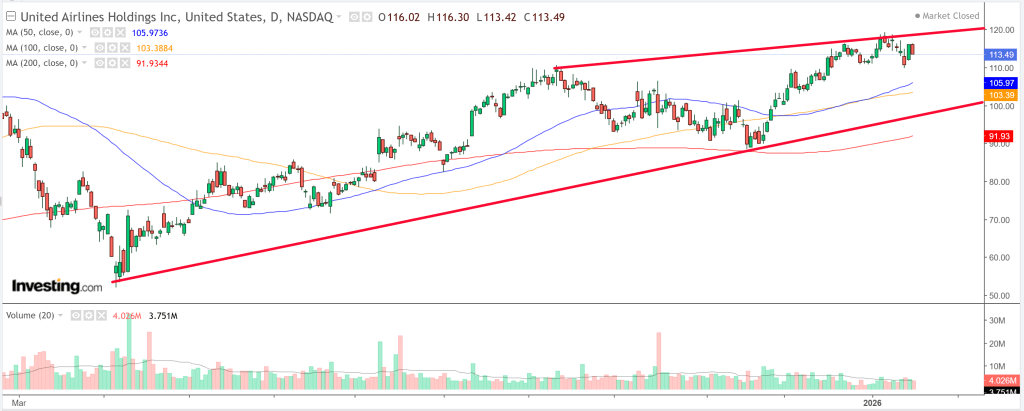

On Thursday, earnings are due from Procter & Gamble (NYSE: PG), GE Aerospace (NYSE: GE), Intel (NASDAQ: INTC), Abbott Laboratories (NYSE: ABT), and Intuitive Surgical (NASDAQ: ISRG). Elsewhere in Tuesday evening trading, United Airlines Holdings Inc (NASDAQ: UAL) jumped 5% after posting strong quarterly earnings and an upbeat outlook.

Wall Street rattled by Trump–Greenland dispute

Wall Street’s major indexes slumped sharply on Tuesday — the first trading day after a long weekend — as investors were unnerved by escalating geopolitical tensions tied to President Donald Trump’s aggressive push over Greenland and tariff threats against several European countries. The sell-off marked one of the market’s worst sessions in months, with the S&P 500, Dow Jones, and Nasdaq all posting significant declines amid heightened risk aversion.

Trump’s plan to pressure European allies with new tariffs in an effort to secure U.S. leverage over Greenland drew strong rejection from European leaders and amplified fears of broader trade conflict, prompting a flight from risk assets.

On the trading day, the S&P 500 dropped about 2.1%, the Nasdaq Composite slid nearly 2.4%, and the Dow Jones Industrial Average fell roughly 1.8%. Tech and broader market stocks led the weakness, underscoring how geopolitical uncertainty can quickly sour sentiment across sectors.

Few analysts had a U.S. invasion of Greenland anywhere near the top of their 2026 market outlooks. President Trump’s surprise weekend tariff move has triggered a classic risk-off reaction, with gold rallying around 2%, equities down 1.0–1.5%, and the dollar coming under modest pressure. This week’s World Economic Forum in Davos is now set to become a focal point for U.S.–European diplomacy, with elevated FX volatility likely.

USD: Too Early to Embrace the ‘Sell America’ Narrative

Washington escalated its pursuit of Greenland over the weekend, with the threat of 10% tariffs—potentially rising to 25%—on eight European countries appearing consistent with a broader “maximum pressure” strategy to force a deal. Political commentary in Europe suggests this could mark the end of the EU’s long-standing policy of accommodation toward the U.S., with France emerging as a key advocate for deploying the EU’s Anti-Coercion Instrument, which allows for retaliatory measures spanning tariffs, taxation, and investment restrictions against coercive trade actions.

The issue, alongside growing concerns about strains within NATO, is set to dominate the policy agenda in a week that might otherwise have focused on Ukraine. President Donald Trump is scheduled to speak at the World Economic Forum in Davos on Wednesday, followed by an EU leaders’ meeting on Thursday. A central question is whether Europe adopts China’s approach from last year—matching U.S. tariffs one-for-one—to ultimately force a de-escalation from Washington.

Initial market reactions have been cautious but telling: gold has gapped roughly 2% higher, German DAX futures are down around 1.5%, and the U.S. dollar is marginally weaker. While U.S. cash markets are closed for the Martin Luther King Jr. holiday, S&P 500 futures are indicating losses of about 0.8%. Still, it may be premature to revive the “Sell America” narrative. As with last April’s near-50% “Liberation Day” tariff threats, investors appear reluctant to chase what often proves to be aggressive rhetoric that ultimately gives way to diplomatic negotiation.

Nonetheless, these developments are likely to inject a degree of volatility into what has otherwise been a relatively calm investment environment. On the broader “Sell America” theme, we noted on Friday that there was little concrete evidence of meaningful de-dollarisation last year. Even in a scenario where geopolitical tensions were to escalate materially, it appears unlikely that the dollar would experience a sell-off on the scale of last year’s near-10% decline, particularly given that the buy-side was then unusually under-hedged in U.S. dollar exposure.

Beyond the Greenland issue, this week may also bring clarity on the future leadership of the Federal Reserve. President Trump could announce his nominee to succeed Jerome Powell as Fed Chair. The dollar rallied on Friday after reports suggested Trump wants Kevin Hassett to remain at the National Economic Council, with Kevin Warsh now viewed as the leading candidate—an outcome that would be modestly supportive for the dollar if confirmed.

Overall, U.S. economic data are likely to take a back seat to political developments in the coming days. In the near term, the dollar may probe lower levels. For DXY, gap resistance around 99.35 could cap upside, while a corrective move toward the 98.80–98.85 zone remains the mild tactical bias.

EUR: Unwelcome Developments