Passive income is a form of income that is generated repeatedly and relatively steadily after an initial investment of time, effort, or capital to build a system, asset, or operating model. Unlike active income, which requires a direct exchange of time for money, passive income leverages capital, technology, intellectual property, or branding to create long-term value. While it does not mean “earning money without doing anything,” passive income reduces dependence on daily labor and provides a more sustainable and resilient financial foundation over time.

The Benefits of Passive Income

Financial stability and diversification

Passive income creates a more secure financial position by ensuring that earnings continue even when active work is reduced or interrupted. This stability helps individuals and businesses better manage expenses and plan for the future.

Relying on multiple income streams lowers overall financial risk. If one source underperforms or stops, others can continue to provide cash flow, reducing vulnerability to economic or industry-specific shocks.

Time freedom and long-term wealth creation

Because passive income is not directly tied to hours worked, it allows individuals to reclaim time. This time can be invested in personal growth, strategic thinking, or higher-value activities.

Many passive income streams grow over time through reinvestment and compounding. Assets such as investments, digital products, or intellectual property can generate increasing returns without proportional effort.

Scalability and flexibility

Passive income models can expand without significantly increasing workload. Once systems are in place, income can grow through broader distribution, automation, or market expansion.

With steady passive income, individuals have more freedom to change careers, start new ventures, or pursue opportunities that may not offer immediate active income.

Financial resilience and leverage of assets

It allows people to maximize the value of existing assets—such as capital, expertise, content, or technology—by turning them into ongoing income-generating resources.

Reduced stress and strategic focus

Having reliable income streams beyond active work lowers financial pressure, leading to greater peace of mind and improved decision-making.

By reducing the need for constant operational involvement, passive income enables a shift toward long-term strategy, innovation, and sustainable growth.

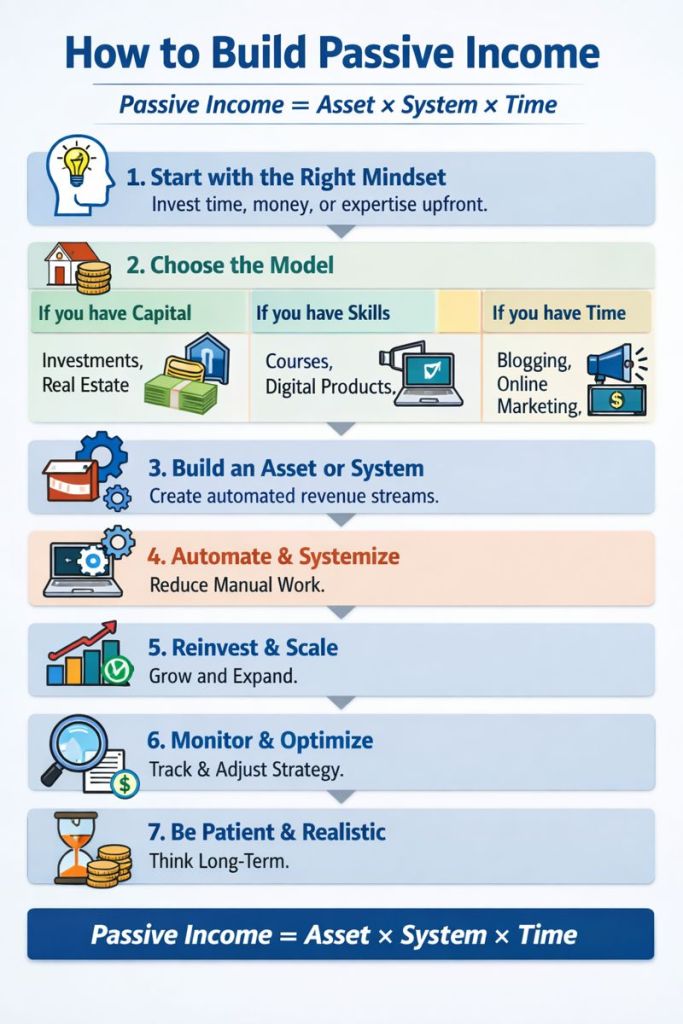

How to Create Passive Income

Before participating in trading or investing in economic or financial markets, acquiring knowledge is essential for preparing for sustainable long-term growth, helping investors develop discipline, risk management skills, and a clear strategic mindset to navigate market volatility.

How Can We Generate Passive Income?

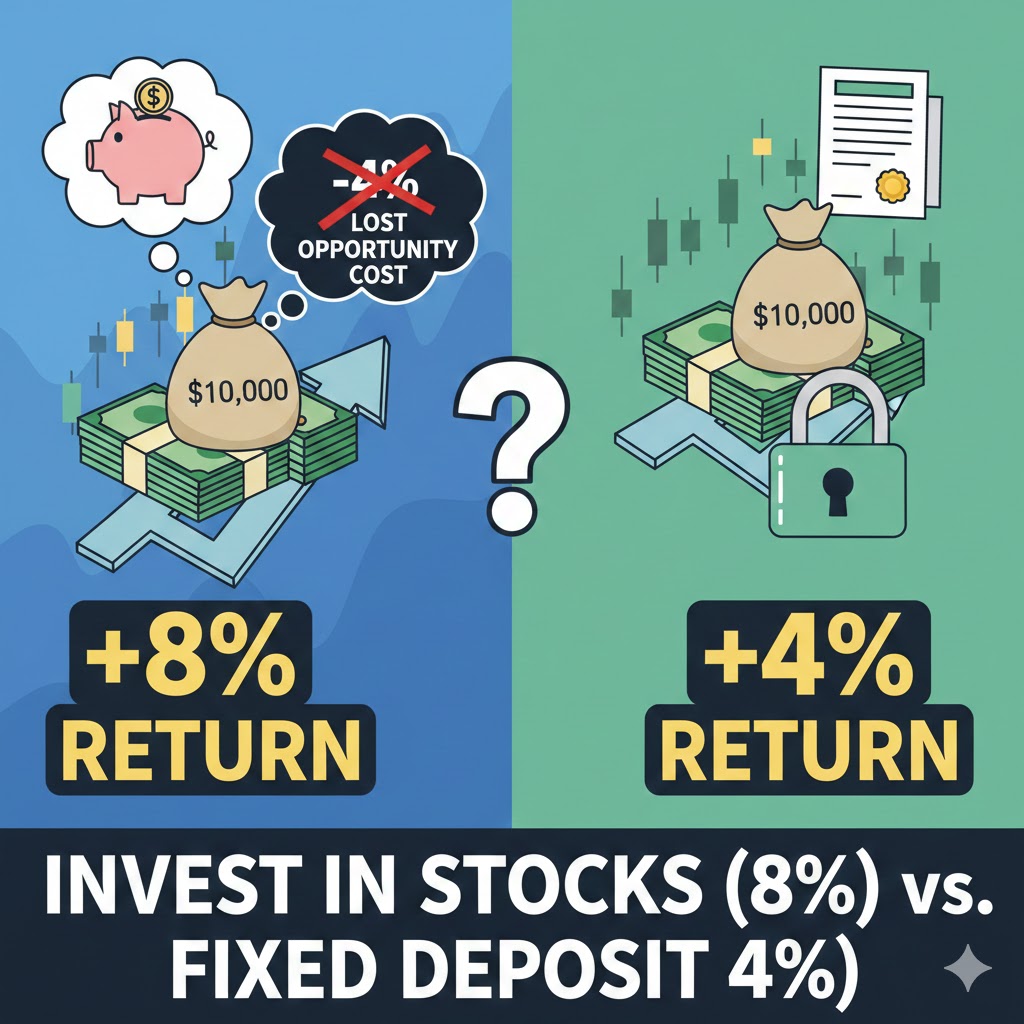

What is Stocks and Bonds?

Stocks and bonds are two common types of investments. Stocks represent ownership in a company, meaning you benefit when the company grows through rising share prices and sometimes dividends, but you also face higher risk because prices can fluctuate. Bonds, on the other hand, are loans you give to a government or company; in return, you receive regular interest payments and get your original money back at maturity, making them generally more stable but with lower returns than stocks.

What is high-risk investments?

High-risk investments are investments where the chance of losing money is significant, but they offer the potential for very high returns. Their value can change rapidly due to market volatility, economic events, or speculation, and outcomes are less predictable than traditional investments. Examples include cryptocurrencies, early-stage startups, speculative stocks, leveraged trading, and some derivatives. These investments are usually suitable only for investors who can tolerate large fluctuations and afford to lose part or all of their invested capital.