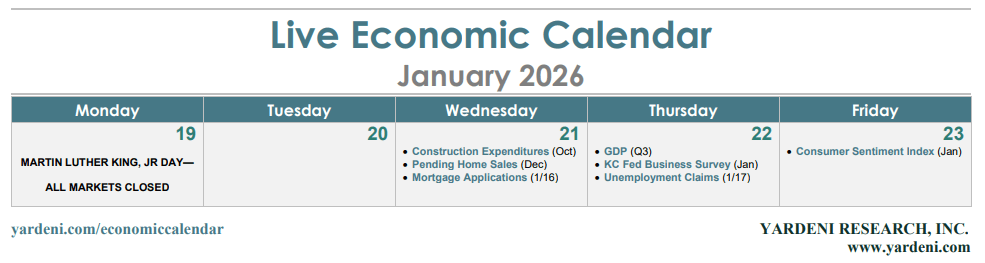

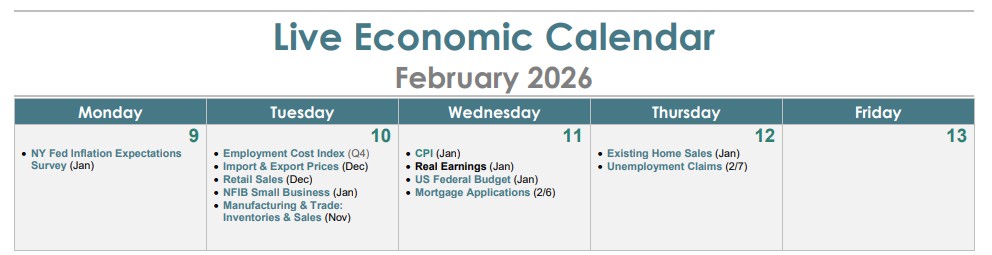

As a polar vortex brings arctic conditions across the U.S., the economic calendar is set to heat up. The week ahead features two of the most consequential data releases for shaping Federal Reserve policy expectations: the January employment report and the Consumer Price Index (CPI).

Owing to recent government shutdowns, the January employment report (Wednesday) and CPI release (Friday) will be published unusually close together. The labor report is particularly significant, as January data typically incorporates annual revisions to employment figures, raising the possibility of notable downward adjustments for the year through March 2025.

A key reference point will be the Federal Reserve’s own assessment of potential overstatement in jobs growth. In December, Fed Chair Jerome Powell noted that internal research suggested official figures may have overstated monthly job gains by as much as 60,000 since April. Given that reported job growth averaged just under 40,000 per month over that span, the scope of upcoming revisions could have meaningful implications for the FOMC’s March policy decision.

The week also features remarks from several Fed officials, including Governors Christopher Waller (Monday), Stephen Miran (Monday and Thursday), and Michelle Bowman (Wednesday). Among voting Fed presidents this year, Cleveland Fed President Beth Hammack and Dallas Fed President Lorie Logan are both scheduled to speak on Tuesday.

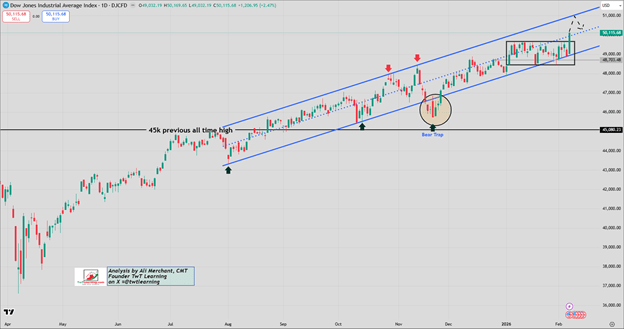

Markets will also be watching price action on Wall Street following last week’s record close for the Dow Jones Industrial Average above 50,000. The ongoing AI-led shakeout among major technology stocks bears close scrutiny, as does the renewed “old economy” rotation bringing previously sidelined sectors—such as oil and gas, chemicals, transportation, and regional banks—back into focus. Adding to the cross-currents is gold’s continued rally, occurring alongside a sharp pullback in bitcoin.

The following data releases carry the greatest potential to move markets and shape the Federal Reserve’s assessment of whether further rate cuts are warranted:

Employment

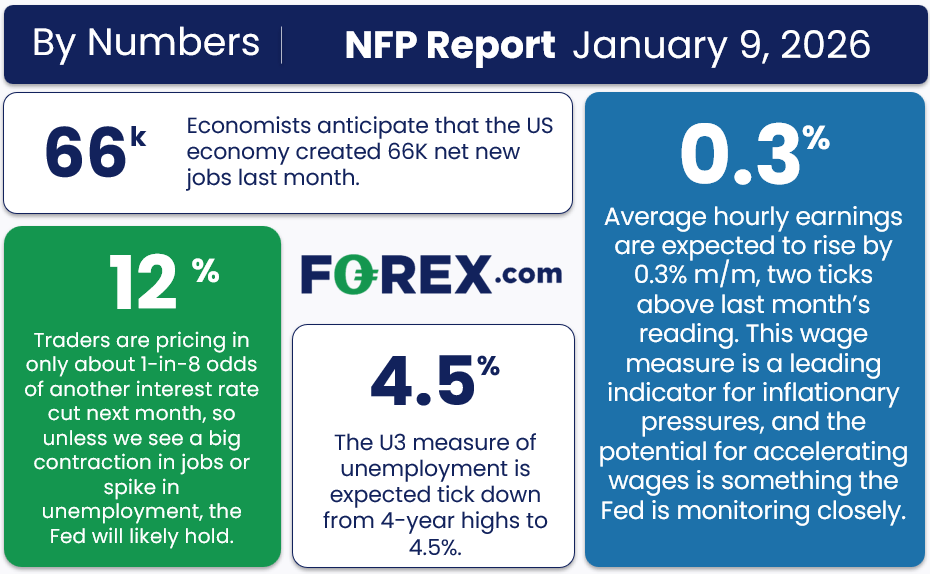

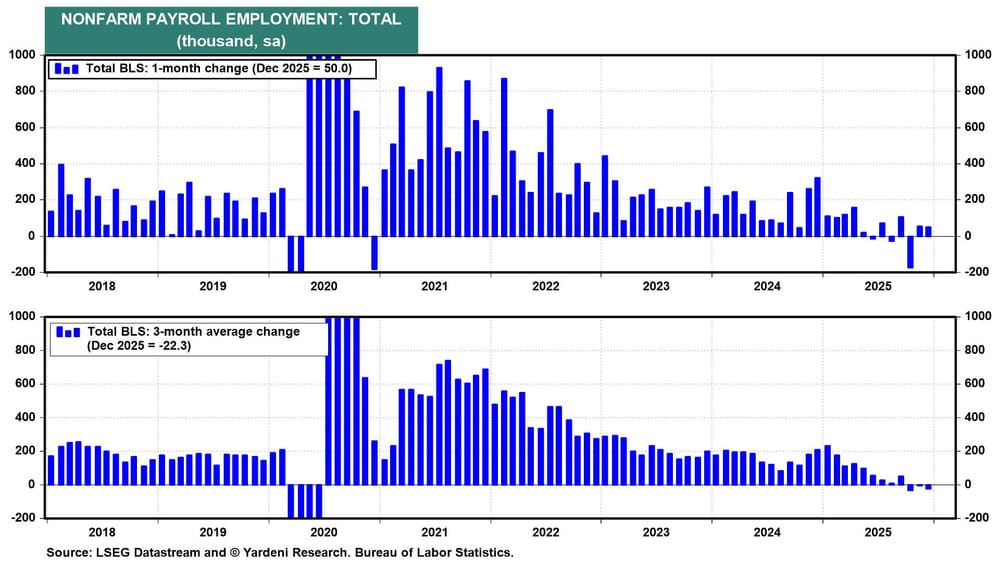

We expect nonfarm payrolls to rise by 60,000 in January, following a 50,000 increase in December (see chart). Markets will be closely focused on the size and direction of revisions to prior data. A meaningful downside surprise could increase pressure on Chair Powell to consider a rate cut later this month, even though we do not believe monetary policy can directly address the underlying weaknesses in the labor market.

CPI

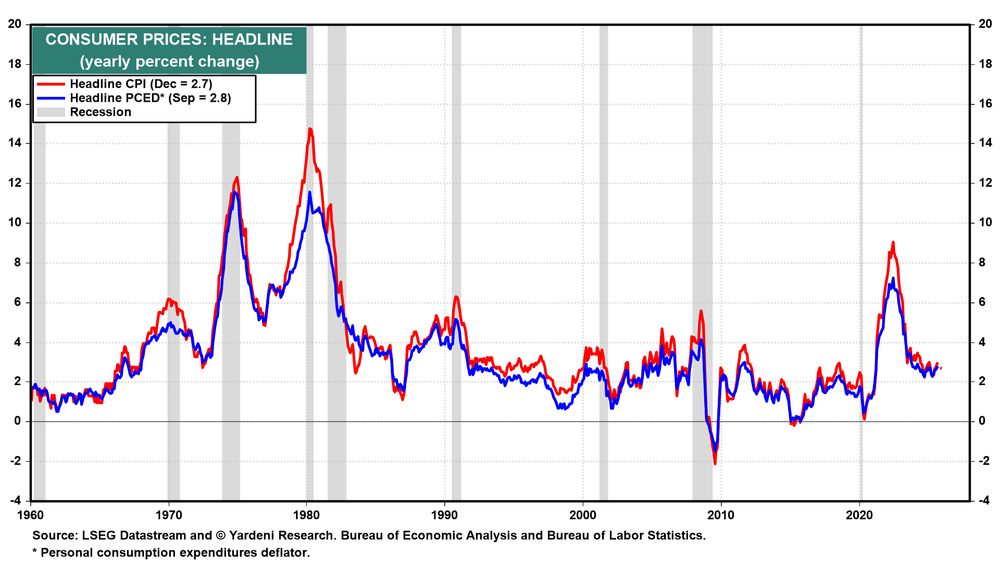

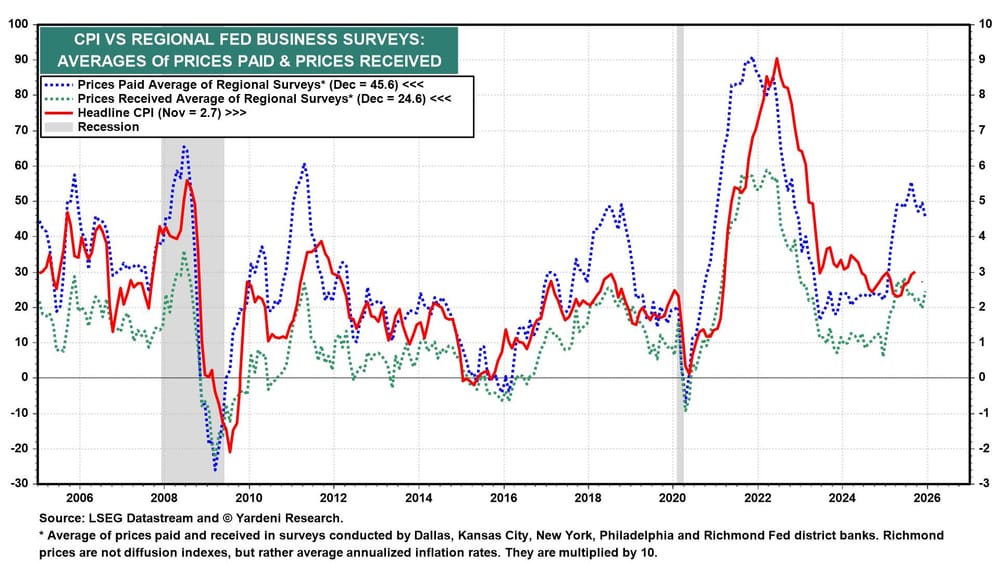

Markets are seeking further confirmation that inflation continued to ease in January. December’s 2.6% year-over-year reading matched a four-year low in core CPI inflation (see chart). The Cleveland Fed’s Inflation Nowcasting model currently projects a 0.22% month-over-month increase in core inflation, translating to a 2.45% annual rate. Additional insight on inflation pressures will come from the Q4 2025 Employment Cost Index and December import and export prices, both due Tuesday, as well as the New York Fed’s January inflation expectations survey on Monday.

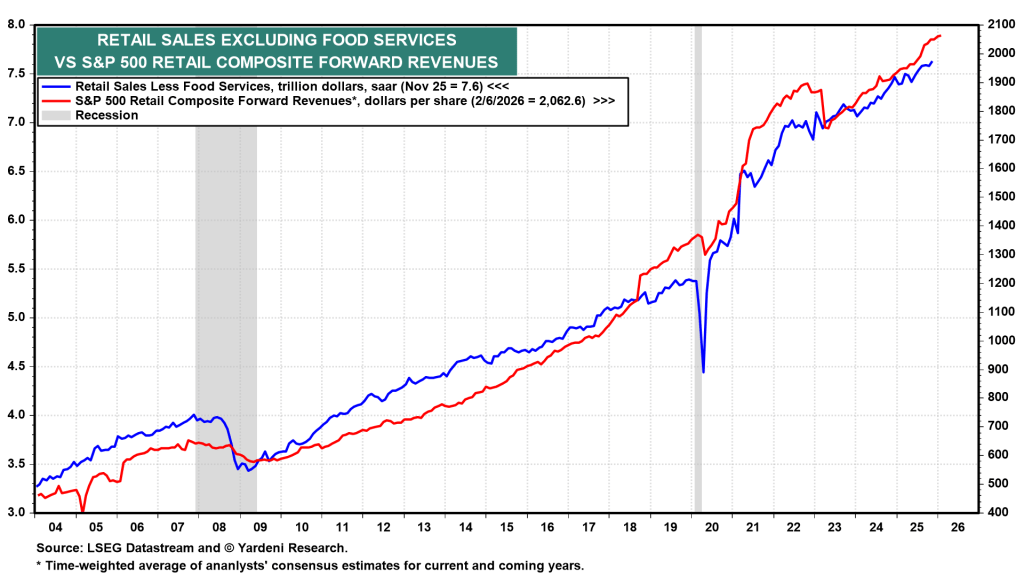

Retail sales

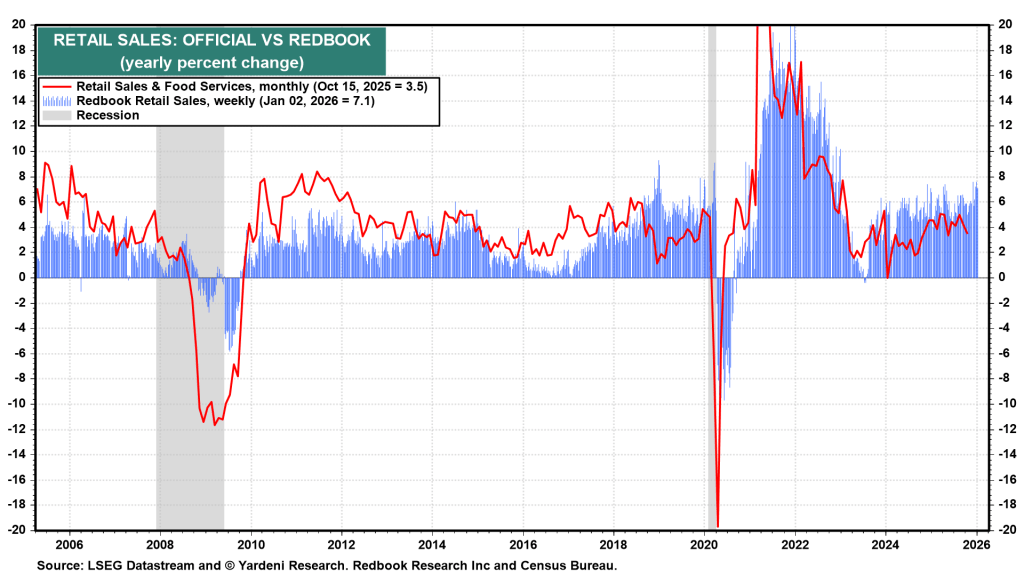

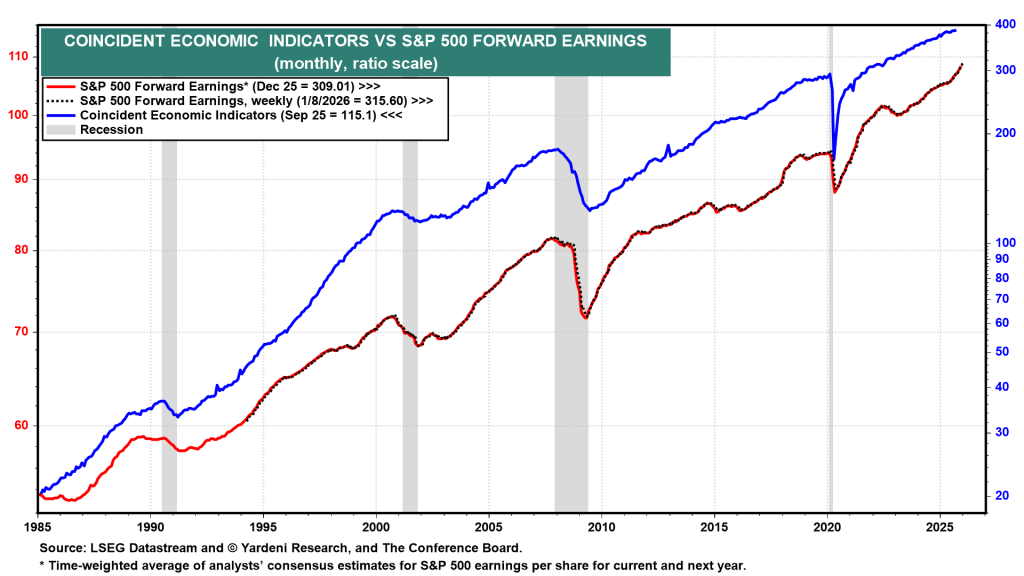

Despite ongoing concerns about the cost of living and a fragile labor market, household spending continues to show resilience. Retail sales in December, due Tuesday, are expected to post another solid gain following November’s 0.6% month-over-month increase. Looking ahead, larger annual tax refunds should help sustain consumer spending momentum. Reflecting this strength, forward earnings for the S&P 500 Retail Composite climbed to a record high during the week of February 6 (see chart).

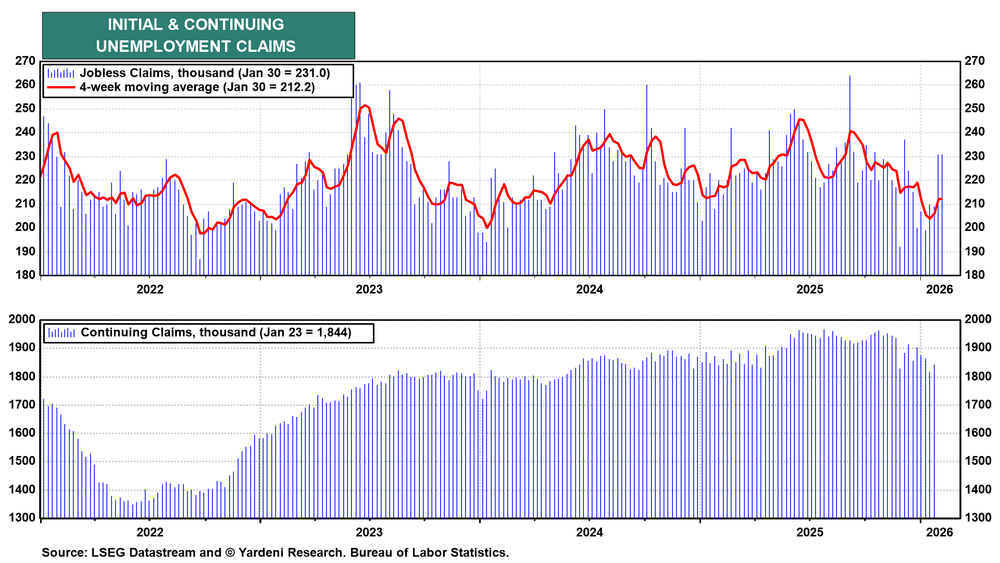

Jobless claims

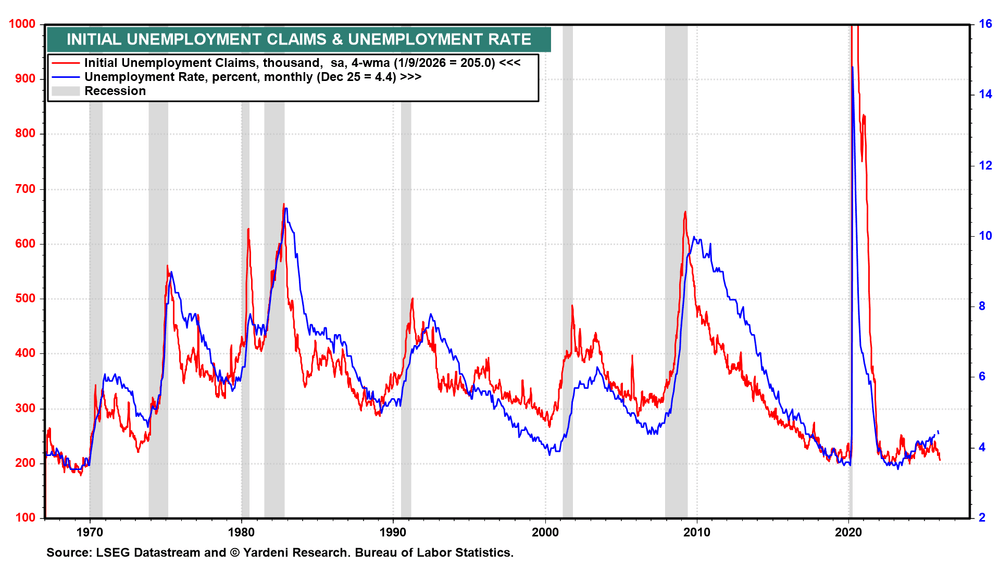

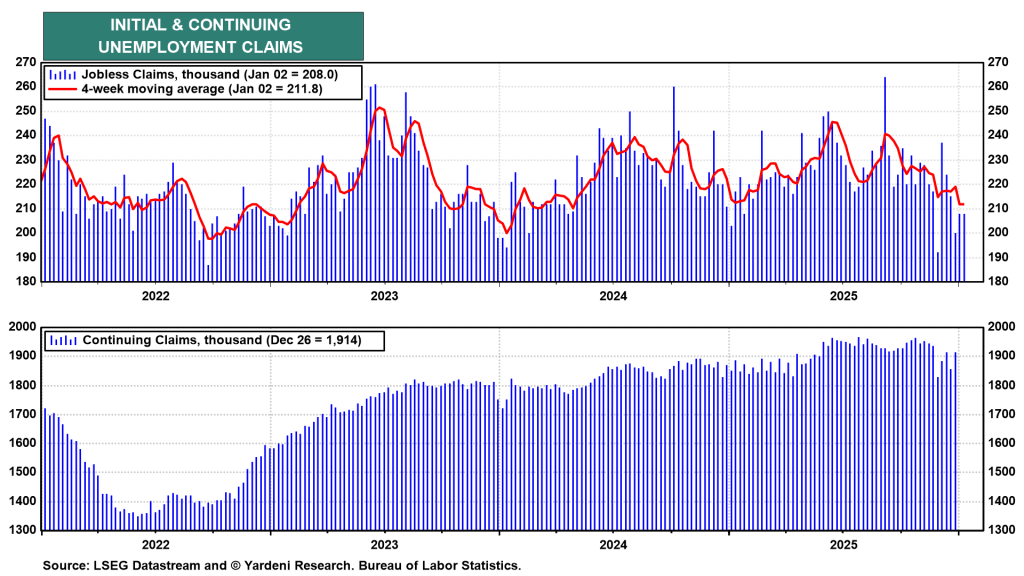

Initial jobless claims due Thursday will draw heightened scrutiny as investors look to determine whether last week’s jump to 231,000 was driven by severe winter storms rather than a broader acceleration in layoffs. The balance of evidence points to a weather-related distortion, which would likely reassure the Fed that the labor market remains on relatively stable footing.

Sources: Ed Yardeni