US stock futures stabilized on Tuesday following a shaky start to the week, as renewed selling linked to AI disruption concerns unsettled investors. Sentiment was also dented by fresh uncertainty around US President Donald Trump’s tariff agenda. Anxiety over artificial intelligence’s potential to disrupt software and wider industries intensified after a bearish report from Citirni Research highlighted AI-related risks extending beyond the tech sector.

While the intensity of the “AI scare” trade appears to be easing and traders are stepping back into some beaten-down tech names, markets remain cautious amid ongoing tariff confusion. This comes after Friday’s turbulence triggered by the US Supreme Court’s decision to overturn President Trump’s sweeping tariff measures.

The US100 is trying to stabilize after sliding 1.13% in the previous session, breaking below a medium-term ascending trendline drawn from the August lows. The index is trading just beneath the 38.2% Fibonacci retracement of the October 30–November 21 decline from the record peak of 24,757. Immediate support is seen at the 23.6% Fibonacci level around 24,400, while a recovery could prompt a retest of the short-term SMAs near 25,075 and 25,300.

Tariff uncertainty and US-Iran tensions support Gold

Gold is retreating from a three-week high near 5,250 as a firmer US dollar and profit-taking pressure prices after a rally fueled by tariff uncertainty and geopolitical risks in the Middle East. Investors are awaiting further clarity on President Trump’s trade policy after the Supreme Court invalidated his earlier global tariff framework. The administration has since introduced temporary 15% tariffs aimed at addressing what it describes as a balance-of-payments crisis, a characterization questioned by many economists.

Attention also remains on escalating US-Iran tensions ahead of a third round of talks, as the White House signals it may be edging closer to potential military action related to Iran’s nuclear program, including additional naval deployments. Later today, President Trump’s State of the Union address could add another layer of volatility.

Technically, gold has snapped a four-day winning streak and is testing firm support at 5,141 — the 61.8% Fibonacci retracement of the January 29–February 2 decline from its record high. Further support lies near the 20-day SMA around the key 5,000 mark. Despite the pullback, the broader bias remains positive, with both MACD and RSI still in bullish territory, albeit turning cautious. A rebound could target 5,342, with scope for fresh highs above 5,420.

Yen ahead of CPI

The yen extended its decline against a stronger dollar as tariff concerns resurfaced and reports suggested Japanese Prime Minister Sanae Takaichi voiced caution about additional Bank of Japan rate hikes during discussions with Governor Kazuo Ueda. The yen’s rebound following the February 8 election has faded, reviving the so-called “Takaichi trade” amid fears that fiscal expansion could further weaken the currency.

Yen weakness also shifts attention to Friday’s Tokyo CPI data. Current fiscal measures may struggle to keep inflation anchored at the BoJ’s 2% target, while recent figures indicate earlier cost-push pressures are easing. Continued currency softness could bring forward expectations for the next BoJ rate hike from December to as early as April.

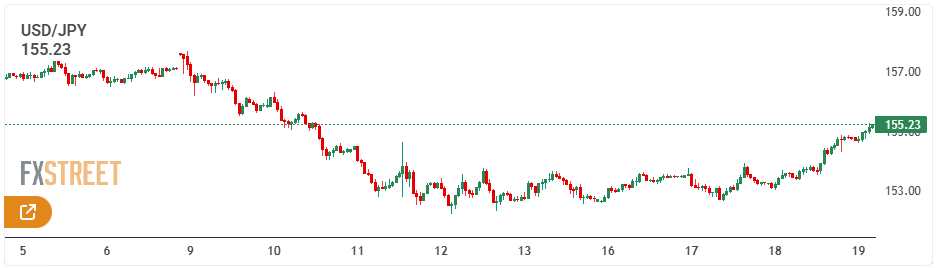

Technically, USD/JPY is approaching an upside breakout from a symmetrical triangle pattern, testing two-week highs around 156.30. Momentum remains modest, with the RSI hovering near the neutral 50 level and the MACD still below zero. A daily close above the 50-day SMA — coinciding with the triangle’s upper boundary — could pave the way toward 157.60. On the downside, a move below the 20-day SMA may expose the psychological 154.00 level.

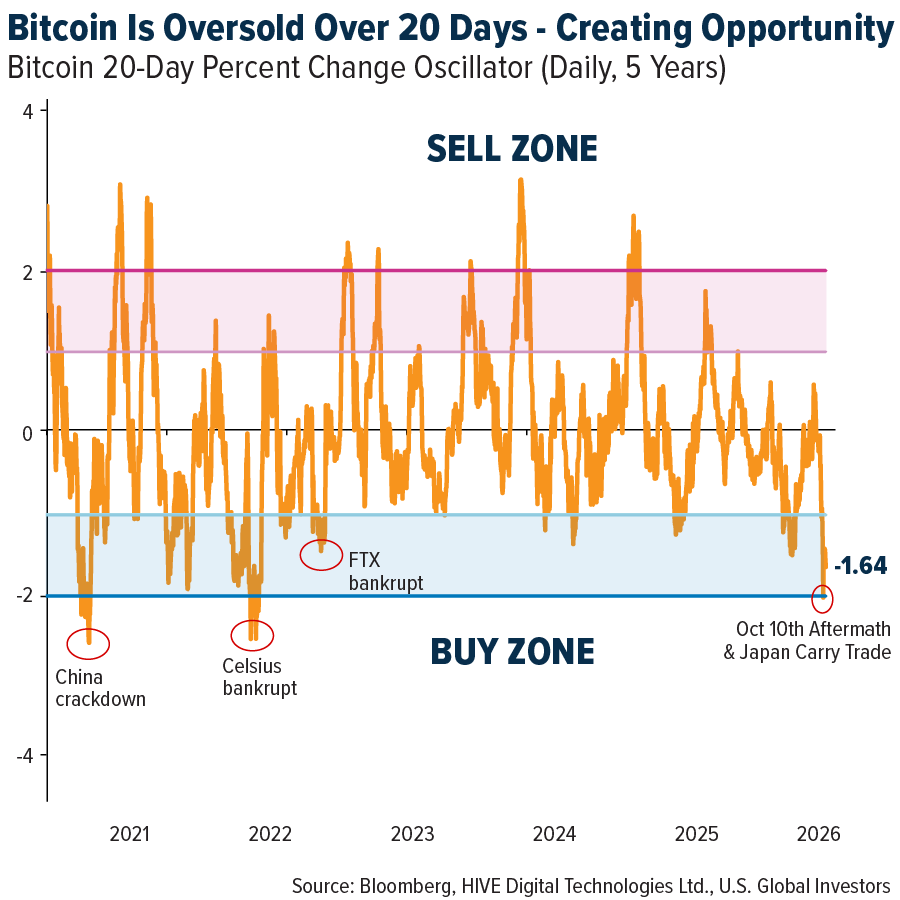

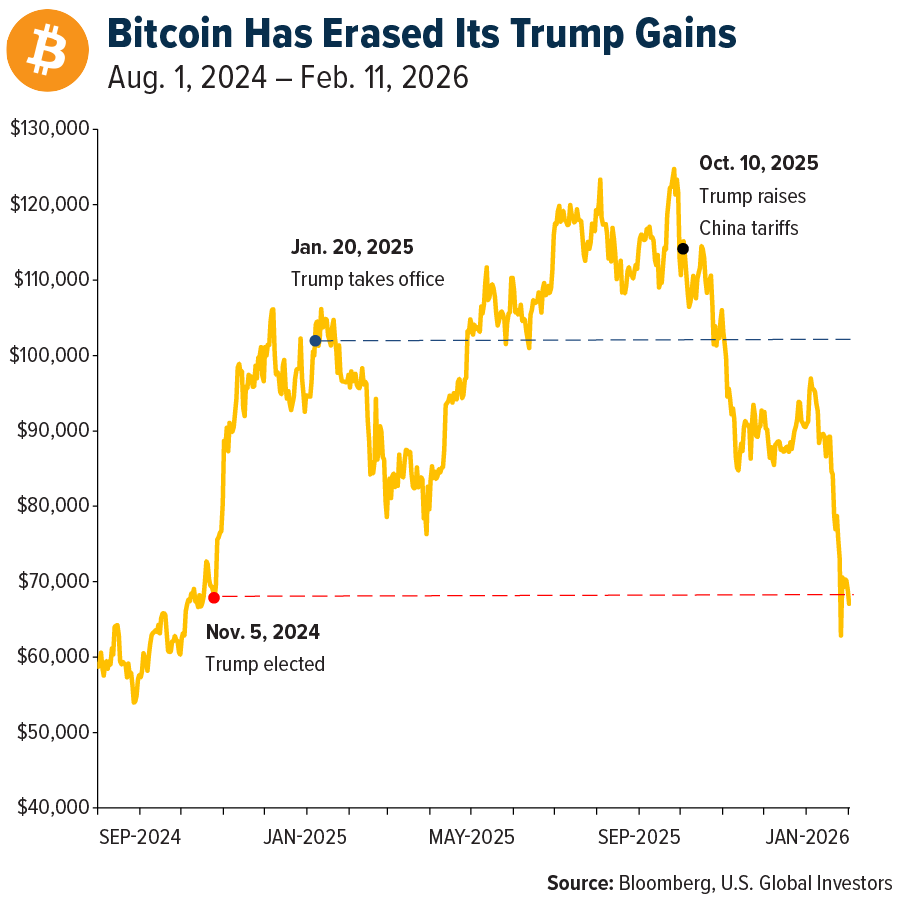

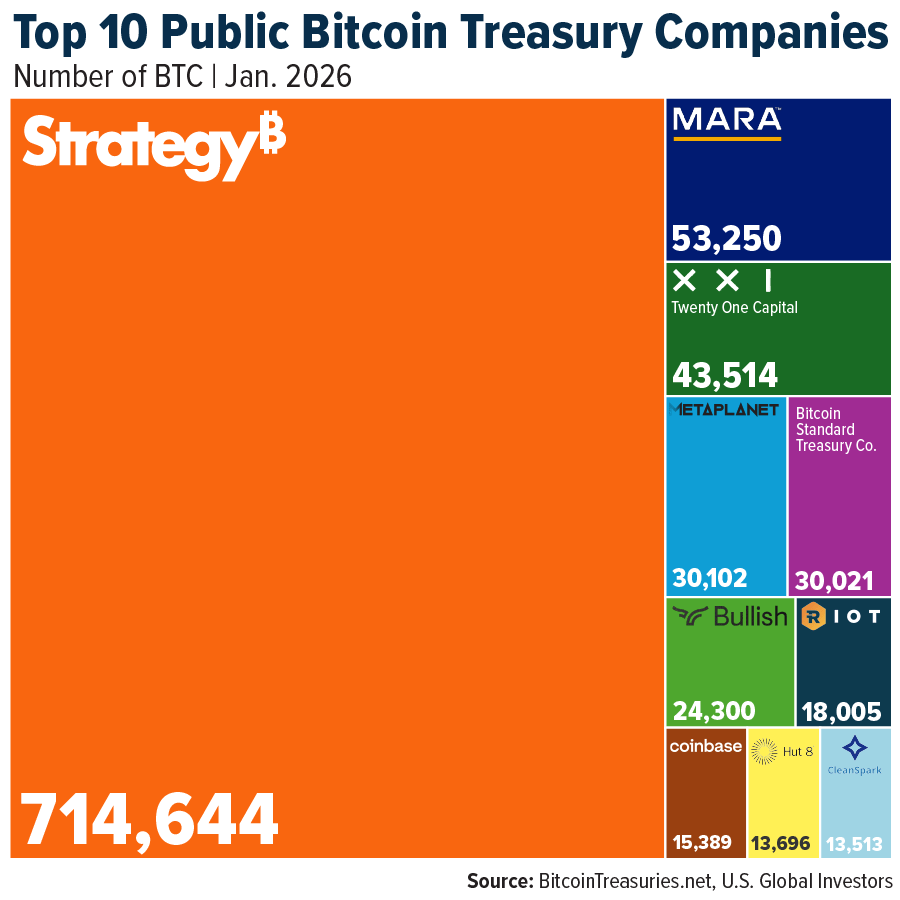

Bitcoin fell again on Tuesday, deepening its recent slide and now trading roughly 50% below its October record high, as uncertainty surrounding U.S. tariff policy dampened risk appetite for digital assets.

The world’s largest cryptocurrency slipped 0.9% to $64,169.6 by 17:35 ET (22:35 GMT), after touching an intraday low of $62,650.1.

Broader crypto markets also remained under pressure, with both institutional and retail investors continuing to reduce exposure. Escalating geopolitical tensions involving Iran, along with an AI-driven selloff on Wall Street, further weighed on sentiment.

Bitcoin down 50% from peak

With Tuesday’s losses, Bitcoin is now trading about half below its early-October all-time high of $126,186.

The cryptocurrency has been in a sustained downturn since that peak, as fresh U.S. regulatory measures and ongoing purchases by major corporate holder Strategy failed to meaningfully support prices.

On Monday, Strategy revealed it had acquired an additional 592 Bitcoin. However, the firm is currently facing significant unrealized losses, as Bitcoin trades below its reported average purchase price of $76,020.

On-chain data from CryptoQuant and Coinglass indicated that large holders—commonly known as “whales”—continued transferring substantial amounts of Bitcoin to exchanges, suggesting further selling pressure.

Meanwhile, major buyers appear scarce. Data from Glassnode showed institutional investors recorded a fifth straight week of net outflows from U.S. spot Bitcoin ETFs as of Monday.

Iliya Kalchev of Nexo Dispatch noted that U.S. spot Bitcoin ETFs saw around $203 million in net outflows on Monday alone. At the same time, derivatives markets still show demand for downside hedging, while long-term holders have not signaled broad capitulation—leaving Bitcoin in what he described as a fragile balance between visible pressure and underlying structural conviction.

He highlighted the $60,000–$72,000 range as the key near-term zone. If ETF flows stabilize and macro volatility subsides, the range could form a base. But if outflows continue, focus may shift toward the realized price area near $55,000 as the next major reference point.

Tariff uncertainty adds pressure

Bitcoin’s latest weakness was largely driven by renewed uncertainty over U.S. trade policy after the Supreme Court struck down much of President Donald Trump’s tariff framework.

In response, Trump announced new universal tariffs of 15% under a different legal authority, though the initial rate implemented at midnight Tuesday was 10%. The president now faces additional legal hurdles in expanding tariffs but has shown little intention of retreating from his trade agenda, even warning that countries seeking to renegotiate trade deals could face higher duties.

Although cryptocurrencies are not directly tied to trade flows, they are highly sensitive to shifts in global risk sentiment. The uncertainty surrounding U.S. tariffs has triggered broader risk aversion across financial markets, spilling over into digital assets.

Altcoins follow Bitcoin lower

Most altcoins tracked Bitcoin’s decline, with the broader market showing little sign of relief from the ongoing downturn.

Ethereum slipped 0.1% to $1,857.78, hovering near early-February lows. XRP and BNB fell 0.2% and 1.9%, respectively, while Cardano declined 1.4%. Solana bucked the trend, rising 0.9%.

Among meme tokens, Dogecoin dropped 1.1%, while TRUMP gained 1.3%.

The U.S. dollar recovered on Tuesday after the prior session’s slide, supported by upbeat economic data, while investors stayed cautious amid fresh volatility tied to President Donald Trump’s tariff policies.

At 15:24 ET (20:24 GMT), the Dollar Index—measuring the greenback against six major currencies—rose 0.2% to 97.86, after falling as much as 0.5% a day earlier.

Strong data underpin dollar

Encouraging economic releases lent the dollar some backing. ADP reported a gain of 12.8K in private payrolls last week, exceeding the previous reading. In addition, the Conference Board’s consumer confidence index for February surprised to the upside at 91.2.

According to José Torres, senior economist at Interactive Brokers, the stronger-than-expected figures nudged both the dollar and yields modestly higher, with a bear-flattening move led by shorter-dated maturities that are more sensitive to monetary policy.

He noted that firmer labor data are pushing rates up, as improving employment conditions weaken the case made by dovish Federal Reserve members for interest rate cuts based on softening job trends.

Trade tensions cloud outlook

Despite the rebound, uncertainty surrounds the U.S. currency as Trump’s revised tariff plans take shape following a Supreme Court ruling that his use of a 1977 emergency law to impose tariffs overstepped his authority.

In response, Trump said he would lift a temporary import tariff from 10% to 15% on goods from all countries. The move has cast doubt on the reliability of trade agreements reached prior to the ruling. Reflecting this uncertainty, the European Parliament delayed a vote on the European Union’s trade pact with the United States due to the new import tax.

Trade concerns have resurfaced at a time when questions are also emerging over the durability of heavy investment in artificial intelligence and the resilience of the U.S. economy after last week’s weak growth data.

Euro steady; Yen under pressure

In Europe, EUR/USD slipped 0.1% to 1.1779, with the euro largely steady after ECB President Christine Lagarde reiterated in Washington that the European Central Bank’s rate policy remains in a “good place,” while emphasizing the need for flexibility.

GBP/USD edged up 0.1% to 1.3501 ahead of parliamentary testimony from four Bank of England rate-setters, which may shape expectations before the March policy meeting.

In Asia, USD/JPY jumped 1% to 155.76 as expectations for near-term tightening by the Bank of Japan softened. The yen was also pressured by a Nikkei report suggesting U.S. authorities led recent rate-check efforts aimed at supporting Japan’s currency.

USD/CNY fell 0.4% to 6.8830 after the People’s Bank of China kept its one-year and five-year loan prime rates unchanged, signaling Beijing’s preference for calibrated support while balancing growth and financial stability. Chinese markets reopened Tuesday following the Lunar New Year holiday.

Elsewhere, AUD/USD rose 0.1% to 0.7060, while NZD/USD advanced 0.2% to 0.5967.

Gold edged higher in Asian trading on Wednesday, recovering slightly after the prior session’s pullback driven by profit-taking, as markets weighed the effects of newly enacted U.S. tariffs and looked ahead to upcoming U.S.–Iran negotiations later this week.

Spot gold climbed 0.8% to $5,184.55 per ounce as of 21:08 ET (02:08 GMT), while U.S. gold futures advanced 0.5% to $5,203.10 an ounce. The metal had dropped 1.6% on Tuesday, ending a four-day winning streak.

On Tuesday, the U.S. began enforcing a temporary 10% blanket import tariff, with the Trump administration aiming to raise it to 15%. The move has heightened concerns about global trade disruptions and inflationary pressures. This action came after a U.S. Supreme Court decision last week invalidated earlier broad tariffs introduced under emergency powers, prompting the government to reinstate duties using alternative legal grounds.

Investors also monitored geopolitical developments, as Washington and Tehran are scheduled to hold a third round of nuclear discussions in Geneva on Thursday.

Despite the rebound, gold’s upside remained limited amid expectations that U.S. interest rates will stay higher for longer. Two Federal Reserve officials indicated on Tuesday that there is little urgency to adjust monetary policy, reinforcing a rate outlook that tends to weigh on non-yielding assets like gold.

Additional pressure came from a firmer U.S. dollar, which makes commodities priced in dollars more expensive for foreign buyers. The U.S. Dollar Index was broadly unchanged after rising 0.1% in the previous session.

Among other precious metals, silver gained 1.6% to $88.59 per ounce, while platinum surged 2.3% to $2,224.60 an ounce.

Oil price

Oil prices stayed close to seven-month peaks on Wednesday, as fears of potential U.S.–Iran military confrontation that could disrupt crude supplies kept investors cautious ahead of fresh talks scheduled for Thursday.

Brent crude rose 43 cents, or 0.6%, to $71.20 per barrel by 0400 GMT, while WTI gained 38 cents, or 0.6%, to $66.01. Brent touched its highest level since July 31 last week, and WTI reached its strongest point since August 4 earlier this week. Both benchmarks have remained elevated as Washington deployed additional military assets to the Middle East in an effort to pressure Tehran into negotiations over its nuclear and ballistic missile programs.

A prolonged conflict could threaten exports from Iran—the third-largest producer within Organization of the Petroleum Exporting Countries—as well as other key producers in the region. Analysts at ING noted that persistent uncertainty is likely to keep a significant geopolitical risk premium embedded in prices, leaving markets highly responsive to new developments.

U.S. representatives Steve Witkoff and Jared Kushner are expected to meet Iranian officials in Geneva on Thursday for a third round of negotiations. Iran’s Foreign Minister Abbas Araqchi said a deal is achievable, provided diplomacy takes precedence. Meanwhile, Donald Trump has warned of “very bad consequences” if no agreement is reached, with uncertainty remaining over whether Iran’s potential concessions would satisfy Washington’s demand for zero uranium enrichment, according to IG analyst Tony Sycamore.

Heightened tensions have also coincided with reports that Iran and China are advancing discussions over the purchase of Chinese anti-ship cruise missiles, which could pose a threat to U.S. naval forces stationed near Iran’s coastline. Experts say such weapons would significantly bolster Tehran’s strike capabilities.

Trump is set to address Congress in his State of the Union speech on Tuesday evening, where he is expected to outline his Iran strategy, though specific details have not been disclosed.

Beyond geopolitics, traders are monitoring supply-demand dynamics. The American Petroleum Institute reportedly showed a sharp 11.43-million-barrel increase in U.S. crude inventories for the week ended February 20, even as gasoline and distillate stocks declined. Official data from the U.S. Energy Information Administration is due later Wednesday.

The purpose here isn’t to make a forecast, but to stay open-minded about money as both a social construct and a carrier of utility value.

The prevailing view argues that the US dollar is destined to collapse, steadily declining toward worthlessness. According to this narrative, the United States will keep creating new dollars to sustain the illusion of stability, until excessive money printing ignites hyperinflation and erodes what little value the dollar has left.

This outlook draws heavily from historical episodes such as the Weimar Republic, where large-scale money creation ultimately destroyed the currency. It’s possible the dollar could follow a similar path.

But money behaves in complex ways. Because it is fundamentally a social agreement, its potential outcomes are broader than we often assume. So instead of assuming collapse, let’s imagine a case for continued dollar dominance.

Consider two hypothetical types of money. The first is a globally recognized currency backed by a basket of industrial commodities—metals like silver and copper, fuels like oil, and other tangible resources. Its value stems not from scarcity alone but from the practical utility of the assets supporting it. Since it is tied to a physical reserve, new units can only be issued if that reserve grows. It cannot be created through lending by banks.

The second type of currency expires after a set period and must be spent before it loses all value. This resembles “scrip” money. Together, these two examples illustrate money’s dual role: a store of value and a medium of exchange.

Naturally, we would save the first form for long-term security—its value rests on enduring real-world utility. The expiring currency, by contrast, would be spent quickly on goods and services.

Now consider another scenario: traveling abroad and collecting small amounts of foreign cash. Each note is valuable within its home country but useless elsewhere until exchanged. The same logic applies to precious metals. If you try to pay for a bowl of noodles with silver, the vendor must convert it into local currency, incurring transaction costs. And if taxes are owed, the government will not accept silver—only its own currency.

This highlights a frequently misunderstood aspect of fiat money. It isn’t “backed by nothing.” Its value lies in granting access to participate fully in the issuing country’s economy.

If that seems abstract, think of a work or residency permit. Without it, economic participation is limited and costly. With it, participation becomes smoother, safer, and more efficient. Currency functions similarly.

Now ask yourself: which currency would most likely be accepted almost anywhere in the world—from a remote market to a major city?

A crisp $100 US bill would probably be welcomed in more places than most alternatives. This isn’t because the paper itself has special intrinsic value. It reflects the network effect: what is already widely recognized and used carries greater practical utility than lesser-known options.

No single form of money perfectly combines store of value, ease of exchange, universal acceptance, and low friction. Searching for one flawless form is probably futile. Instead, currencies that provide:

Access to the largest economic sphere,

The strongest network effect and recognition, and

Reliable price discovery with relatively stable value

That will tend to have higher utility and lower transaction costs than competing alternatives.

Demand for a currency arises from multiple sources: the desire to preserve value, the need to transact, and the appeal of participating in the broadest economic network.

State-issued money has another distinctive trait: its supply can expand or contract. If supply grows more slowly than demand, purchasing power can rise—just as with any other commodity.

Supply is easier to measure than demand, which reflects the collective decisions of millions seeking safety, liquidity, efficiency, and opportunity.

The argument for continued US dollar dominance rests on its imperfect but still advantageous blend of features: relatively transparent pricing, low-friction transactions, powerful global network effects, and access to the world’s largest economic system.

These strengths are not merely products of short-term central bank policies. They reflect the broader framework of governance, institutions, economic depth, social trust, and cultural influence behind the issuing state.

If global uncertainty increases, demand for such a currency could outpace supply. As demand rises and network effects strengthen, a self-reinforcing cycle may emerge—supporting, rather than undermining, the dollar’s supremacy.

Money behaves in peculiar ways. We often assume we fully understand it, and even when we’re convinced a currency is about to collapse, it somehow endures—and sometimes even outperforms expectations.

The goal here isn’t to make a prediction. Rather, it’s to remain open-minded about currency as both a social construct and a vessel of utility value.

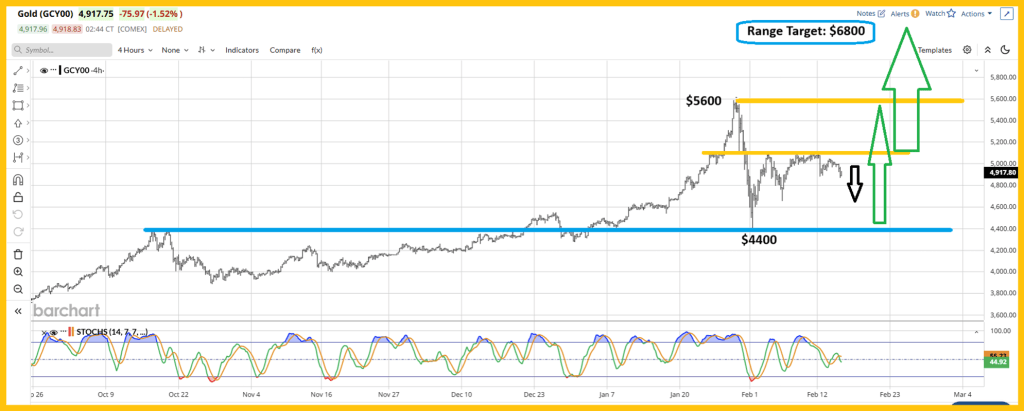

Gold is consolidating after climbing to a monthly peak of $5,250 during Tuesday’s Asian session. The U.S. dollar is attracting renewed demand as liquidity improves and risk appetite stabilizes, even as uncertainty surrounding U.S. tariffs persists.

Despite the pullback, bullion is holding above the 61.8% Fibonacci retracement level at $5,142, which is now acting as key support. Meanwhile, the daily Relative Strength Index (RSI) continues to signal bullish momentum, suggesting the broader uptrend remains intact for now.

XAU/USD Technical Overview

The 21-day Simple Moving Average has climbed above the 50-, 100-, and 200-day averages, and all four are trending higher, highlighting a solid bullish outlook. Price action remains above these key indicators, with the 21-day SMA at $5,029.61 acting as immediate dynamic support. Meanwhile, the 14-day RSI stands at 59.50, slightly above the midpoint, signaling sustained upside momentum.

From the swing high at $5,597.89 down to the low at $4,401.99, the market is consolidating between the 61.8% Fibonacci retracement level at $5,141.05 and the 78.6% level at $5,341.96, which is currently limiting further advances. A decisive daily close above the 78.6% retracement would pave the way for a retest of the previous high, whereas failure to break higher could trigger a decline toward the 50-day SMA at $4,742.30. As long as prices stay above the short-term moving averages, the near-term bias supports continued movement within the retracement range before a clearer breakout emerges.

Fundamental Overview

As trading resumed in China and Japan, liquidity returned to the markets, helping the US Dollar (USD) stabilize after recent pressure.

Investors had previously leaned into “sell America” positions following tariff-related confusion triggered by US President Donald Trump over the weekend, which dented overall market confidence.

Wall Street’s slide continued on Monday amid persistent uncertainty surrounding Trump’s tariff agenda, escalating geopolitical tensions, and caution ahead of AI heavyweight Nvidia’s earnings release on Wednesday.

Gold ended its four-session rally as the USD staged a modest rebound, with prices retreating from monthly peaks to test key support near $5,142.

Market participants remain highly sensitive to tariff developments, particularly after The Wall Street Journal reported early Tuesday that the Trump administration is considering fresh national security tariffs on several industries. The report followed a recent Supreme Court ruling that struck down a number of second-term levies.

At the same time, geopolitical concerns persist, with tensions between the United States and Iran continuing to simmer.

Ongoing expectations that the Federal Reserve will deliver at least two interest rate cuts this year should help limit deeper losses in Gold, which remains a traditional safe-haven asset.

Further underpinning prices, investment demand from India has stayed resilient despite record-high levels, according to Money Metals Exchange.

Bitcoin Cash slipped below the $500 mark on Tuesday, extending losses after plunging 13% in the previous session.

Hyperliquid fell another 1% on Tuesday, marking its fourth straight day of declines following Monday’s sharp 9% drop.

Pump.fun also came under pressure, sliding beneath a key psychological support level after tumbling 11% on Monday.

Altcoins such as Bitcoin Cash (BCH), Hyperliquid (HYPE), and Pump.fun (PUMP) have led declines over the past 24 hours as Bitcoin slipped below the $64,000 level on Tuesday. Technical indicators for BCH, HYPE, and PUMP point to further downside risks amid broad-based market selling.

The wider cryptocurrency market remains under strain as Donald Trump explores new legal avenues, citing national security concerns, to introduce additional tariffs. Meanwhile, U.S. equities ended Monday’s session in negative territory, adding to the cautious tone across risk assets.

CoinMarketCap’s Fear and Greed Index has dropped to 11, signaling extreme fear in the market and underscoring that sellers remain firmly in control.

Bitcoin Cash slips beneath the $500 mark

Bitcoin Cash was trading below the $500 level on Tuesday, extending losses after plunging 13% in the prior session. The altcoin has slipped beneath its 200-day Exponential Moving Average (EMA) at $544, while the 50-day EMA — now trending lower at $555 — is approaching a potential death cross formation.

Technically, the path of least resistance appears tilted to the downside, with the next key support seen around $443, corresponding to the October 17 low.

Daily chart indicators reinforce the bearish momentum shift. The Relative Strength Index (RSI) has dropped to 36, edging closer to oversold territory as selling pressure intensifies. Meanwhile, the Moving Average Convergence Divergence (MACD) has crossed below its signal line, signaling a bearish crossover.

BCH/USDT

If Bitcoin Cash reclaims the $500 psychological barrier with a strong daily close above it, selling pressure could begin to fade, potentially paving the way for a rebound toward the 200-day EMA near $544.

Hyperliquid was trading below $26 on Tuesday, extending losses after falling 9% in the previous session. The HYPE token has now declined for a fourth straight day and remains well under both its 50-day EMA at $29.08 and 200-day EMA at $32.37, reinforcing a bearish outlook.

On the daily chart, the Relative Strength Index (RSI) stands at 38 and continues to trend lower, with further room before entering oversold territory. Meanwhile, the Moving Average Convergence Divergence (MACD) and its signal line are steadily declining, with widening bearish histogram bars signaling strengthening downside momentum.

Immediate support levels are seen at $23.58, marking the December 21 low, followed by $20.82, the October 10 low.

HYPE/USDT

On the upside, Hyperliquid would need to break back above its 50-day EMA at $29.08 to revive short-term bullish momentum and signal the start of a potential recovery.

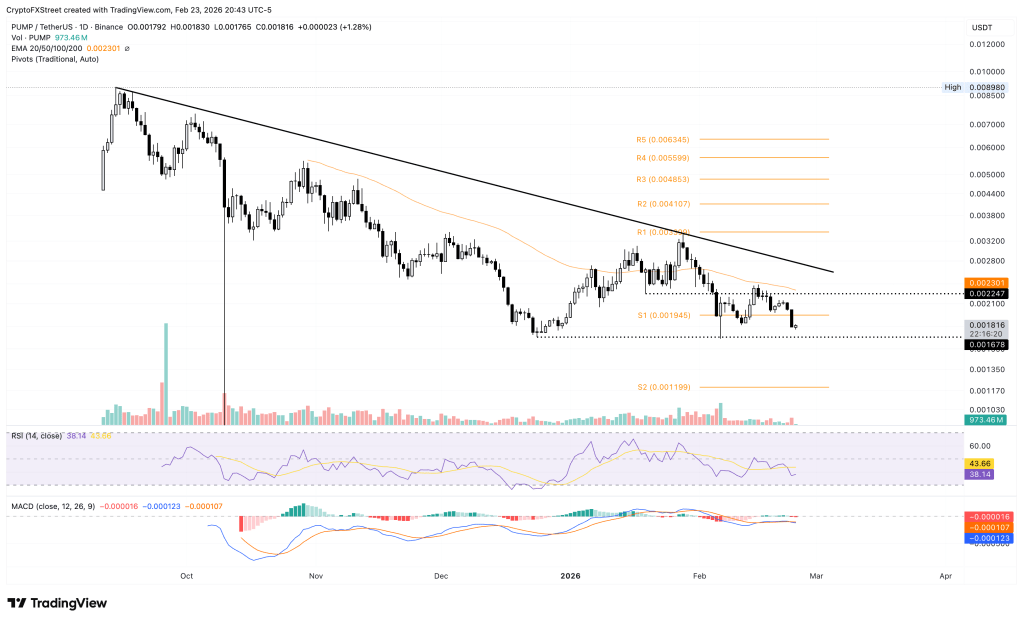

Pump.fun slides toward all-time low amid heavy selling

Pump.fun was trading around $0.001800 at the time of writing on Tuesday, after tumbling 11% in the previous session. The meme-coin launchpad token has continued its broader downtrend since late September and is now eyeing support at $0.001678 — a level that previously sparked a rebound on February 6.

A firm break and close below this support could open the door to further losses toward the S2 pivot at $0.001199.

Momentum indicators point to mounting downside pressure. The Relative Strength Index (RSI) sits at 37, hovering just above oversold territory and reflecting persistent selling interest. Meanwhile, the Moving Average Convergence Divergence (MACD) and its signal line have resumed a downward trajectory following a bearish crossover on Monday, indicating renewed negative momentum.

PUMP/USDT

If Pump.fun climbs back above the S1 pivot at $0.001945, it may pave the way for a move toward the 50-day EMA near $0.002300, potentially easing near-term bearish pressure.

The U.S. dollar weakened on Monday as investors assessed the implications of the Supreme Court of the United States decision to strike down tariffs introduced by Donald Trump, along with the administration’s subsequent response.

Traders were also monitoring renewed nuclear negotiations between Washington and Tehran.

As of 14:12 ET (19:12 GMT), the Dollar Index — which measures the greenback against a basket of six major currencies — was down 0.2% at 97.65. The currency had posted a gain of roughly 1% last week, marking its strongest weekly advance in more than four months.

Dollar pressured by mounting trade uncertainty

The Supreme Court of the United States ruled on Friday that sweeping tariffs introduced by Donald Trump exceeded his authority. In response, Trump criticized the court and unveiled a blanket 15% levy on imports.

The new duties are set to remain in place for 150 days, but it remains unclear whether the U.S. government must reimburse importers for tariffs already collected, as the Court did not address that issue.

The uncertainty could trigger prolonged legal battles and further confusion as Trump explores alternative mechanisms to reinstate broad-based global tariffs on a more permanent footing.

Thierry Wizman, global FX and rates strategist at Macquarie, said the firm’s bearish U.S. dollar outlook for 2026 was based on the view that tariffs signal U.S. “disengagement” from the rules-based order underpinning free trade. He added that tariff conflicts themselves generate uncertainty centered on the United States — a negative for the dollar.

“In that sense, while the Supreme Court ruling may have strengthened institutional checks, it also heightens uncertainty, as Trump is likely to revive the tariff war through different — and more legally grounded — channels that have yet to be detailed. We see no reason to revise our broader expectation for a weaker USD in 2026,” Wizman said.

Beyond trade policy, investors are also watching a U.S. military buildup in the Middle East aimed at pressuring Iran to abandon its nuclear ambitions, with further talks between Washington and Tehran expected later this week.

Euro advances as confidence in Europe strengthens

In Europe, EUR/USD rose 0.2% to 1.1799, with the single currency drawing support from trade-driven weakness in the dollar.

Growing confidence in the region’s economic outlook also underpinned the euro, following data on Friday showing eurozone business activity expanded faster than expected this month, as manufacturing returned to growth for the first time since October.

Momentum was reinforced on Monday as Germany’s Ifo business climate index climbed to 88.6 from 87.6 the previous month, signaling improving sentiment in Europe’s largest economy.

Meanwhile, GBP/USD added 0.1% to 1.3497, with sterling firming ahead of key event risks this week — including testimony before the Treasury Committee by Andrew Bailey, governor of the Bank of England, and Thursday’s UK by-election in Gorton and Denton.

Yen edges higher

In Asia, USD/JPY fell 0.4% to 154.48, with the Japanese yen supported by its traditional safe-haven appeal as investors remained cautious about the economic impact of higher U.S. tariffs. Trading volumes were thinner due to a public holiday in Japan.

USD/CNY was little changed at 6.9087, with Chinese markets shut for New Year holidays. Elsewhere, AUD/USD declined 0.3% to 0.7060, while NZD/USD also dropped 0.3% to 0.5961.

Thierry Wizman of Macquarie said that while the dollar could remain under pressure amid persistent U.S.-driven uncertainty, some currencies — such as the yuan and the euro — may outperform, whereas others, including the Canadian and Mexican pesos, could lag. He added that even in the face of potential credit rating actions, long-term U.S. Treasury yields might rise due to uncertainty over revenue replacement, and equities could come under strain if higher yields lead to valuation compression.

U.S. stock index futures edged higher on Monday night after growing uncertainty surrounding Donald Trump’s tariff policies and concerns about AI-related disruption in the software sector triggered steep losses on Wall Street.

Lingering unease over a potential U.S.-Iran conflict, along with caution ahead of this week’s closely watched earnings from NVIDIA Corporation (NASDAQ: NVDA), also kept sentiment restrained.

As of 19:30 ET (00:30 GMT), S&P 500 Futures were up less than 0.1% at 6,855.0 points. Nasdaq 100 Futures gained 0.1% to 24,781.0 points, while Dow Jones Futures added nearly 0.1% to 48,873.0 points.

FedEx sues U.S. government to recover tariff payments

FedEx Corporation (NYSE: FDX) filed a lawsuit against the U.S. government on Monday evening, seeking a “full refund” of emergency tariffs it paid over the past year.

The action comes only days after the Supreme Court of the United States ruled the levies illegal, with the tariffs scheduled to be lifted from midnight Tuesday.

FedEx is the first company to formally pursue reimbursement following the Court’s decision, joining a broader wave of firms mounting legal challenges against tariff measures introduced under Donald Trump.

However, the ruling did not clarify how the more than $160 billion in revenue already collected from the invalidated tariffs will be handled.

Wall Street battered by tariff uncertainty and AI concerns

Wall Street’s major indexes each dropped more than 1% on Monday as uncertainty surrounding Donald Trump’s tariff policies and mounting concerns about artificial intelligence disrupting the software industry kept investors in a risk-off mood.

Technology sentiment remained fragile ahead of quarterly results from NVIDIA Corporation (NASDAQ: NVDA), scheduled for Wednesday. Widely viewed as a key gauge of AI demand, the world’s most valuable company is expected to post robust earnings growth compared with last year.

Markets also grappled with renewed tariff worries after Trump unveiled a 15% universal tariff under a different legal authority. A report from The Wall Street Journal indicated the administration is considering additional levies on at least six more sectors.

The president appeared to double down on his trade agenda, even as several countries that recently reached agreements with Washington sought greater clarity on the scope and implementation of the tariffs. He also cautioned that nations retreating from newly negotiated trade deals could face steeper duties.

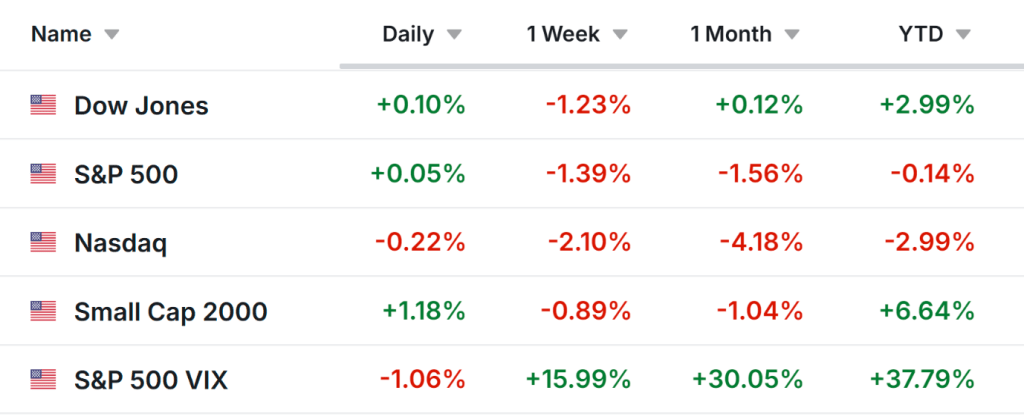

The S&P 500 declined 1%, while the NASDAQ Composite fell 1.1%. The Dow Jones Industrial Average led losses, tumbling 1.7%.

Technology stocks continued to lag, with software names hit by renewed selling pressure amid rising anxiety over AI-driven disruption. Part of the concern stemmed from a speculative note by Citrini Research envisioning a June 2028 scenario in which rapid AI adoption leads to widespread displacement of white-collar jobs.

Oil prices edged higher during Asian trade on Tuesday, remaining just under the seven-month peaks reached in the prior session, as markets looked ahead to upcoming U.S.–Iran discussions later this week. Ongoing uncertainty surrounding trade tariffs continued to temper investor sentiment.

At 22:22 ET (03:22 GMT), Brent crude futures climbed 0.8% to $72.04 per barrel, while U.S. West Texas Intermediate (WTI) crude futures also advanced 0.8% to $66.81 per barrel.

Both benchmarks had approached seven-month highs in the previous session before ending slightly lower.

Market participants are holding back ahead of US – Iran talks scheduled for later this week.

Markets stayed tense ahead of a third round of nuclear talks between Washington and Tehran set for Thursday in Geneva. Strains have persisted since last week amid indications that the situation could escalate. The U.S. pulled some non-essential embassy staff from Beirut, underscoring concerns that diplomacy might collapse and spark conflict.

President Donald Trump warned in a social media post on Monday that it would be a “very bad day” for Iran if no agreement is reached.

“In the event of a deal, we would likely see a significant unwinding of the risk premium currently built into prices — though securing such an agreement is far from straightforward,” analysts at ING noted.

A failure in negotiations could heighten worries about stricter sanctions enforcement or potential disruptions in the Strait of Hormuz, a crucial corridor for global crude shipments. Fears of a possible military clash contributed to a 6% surge in oil prices last week.

Tariff tensions under Donald Trump weigh on demand outlook

Oil markets are also contending with wider macro uncertainty after the Supreme Court of the United States invalidated an earlier round of tariffs introduced under emergency powers.

Donald Trump has since sought to reinstate duties of up to 15% using alternative legal provisions and cautioned that countries that “play games” in trade negotiations with the U.S. could be hit with steeper tariffs.

The risk of renewed trade tensions has darkened the global growth and fuel demand outlook, limiting oil’s advance even as geopolitical concerns continue to lend support to prices.

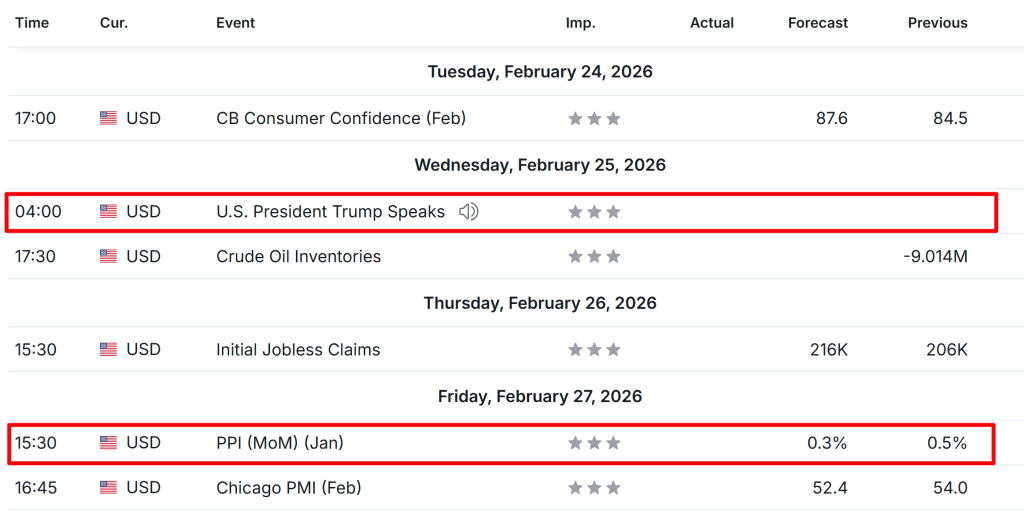

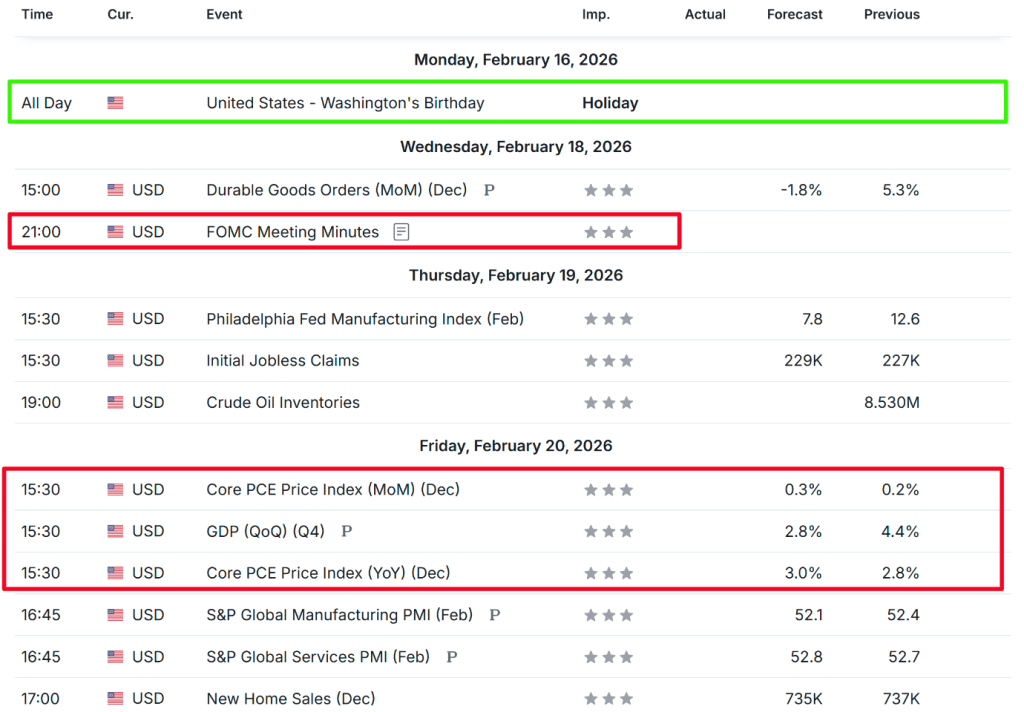

U.S. PPI inflation data and Nvidia’s earnings will take center stage in the coming week.

Nvidia appears set to post another standout quarter.

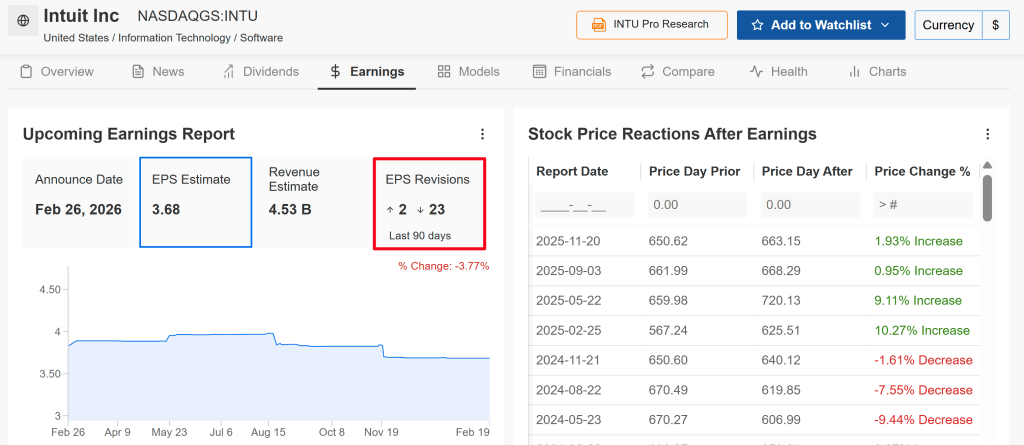

Meanwhile, Intuit is confronting mounting fundamental and technical pressures ahead of its results.

U.S. equities closed higher on Friday after the Supreme Court invalidated President Donald Trump’s tariffs. Trump criticized the decision as a “disgrace” and said in a Truth Social post on Saturday that he would introduce a new 15% global tariff, just one day after announcing a 10% levy.

After Friday’s gains, the 30-stock Dow Jones Industrial Average finished the week up about 0.3%. The S&P 500 advanced 1.1%, while the tech-heavy Nasdaq Composite broke a five-week slide with a 1.5% surge. The small-cap Russell 2000 added nearly 0.7%.

Markets may see heightened swings in the days ahead as investors weigh prospects for growth, inflation, interest rates, and corporate earnings against a backdrop of renewed trade frictions.

With a relatively light economic calendar, attention will center on Friday’s January U.S. producer price index report. As of Sunday morning, traders are pricing in slightly better than even odds that the Federal Reserve will lower rates by its June meeting.

On the earnings front, Nvidia’s (NASDAQ: NVDA) report will headline the week as the season winds down. Beyond Nvidia, investors will be tracking several major tech names, particularly software companies facing pressure from concerns that AI could disrupt their core businesses, including Salesforce (NYSE: CRM), Intuit (NASDAQ: INTU), Snowflake (NYSE: SNOW), Zscaler (NASDAQ: ZS), and Zoom Video Communications (NASDAQ: ZM).

AI infrastructure providers Dell Technologies (NYSE: DELL) and CoreWeave (NASDAQ: CRWV) are also set to post results. Outside the tech space, prominent retailers such as Home Depot (NYSE: HD), Lowe’s Companies (NYSE: LOW), and TJX Companies (NYSE: TJX) are scheduled to report.

At the same time, markets will be parsing President Trump’s State of the Union address on Tuesday and monitoring any developments involving the U.S. and Iran.

No matter which way markets move, below I outline one stock that could attract buying interest and another that may face renewed downside pressure. Keep in mind, this outlook covers only the week ahead—Monday, February 23 through Friday, February 27.

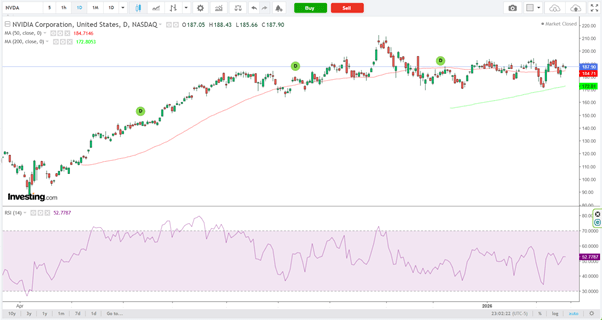

Stock to Buy: Nvidia

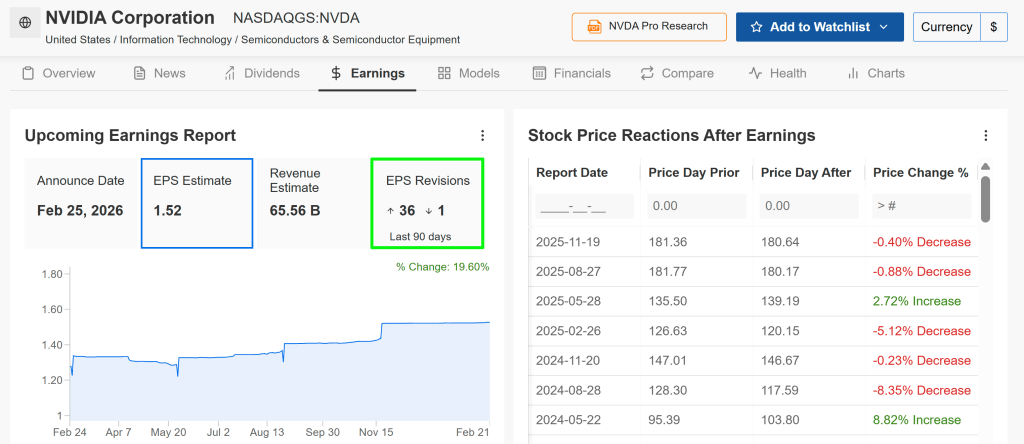

Nvidia heads into its earnings report with analysts anticipating another “beat-and-raise” performance, fueled by robust demand for AI infrastructure. Fourth-quarter results are scheduled for release after Wednesday’s market close at 4:20 p.m. ET, followed by a 5:00 p.m. ET conference call with CEO Jensen Huang.

According to an InvestingPro survey, profit forecasts have been lifted 36 times in recent weeks, compared with just one downward revision—highlighting growing optimism around Nvidia’s earnings outlook. In the options market, traders are pricing in a potential move of roughly ±6% in NVDA shares following the announcement.

Wall Street expects the AI powerhouse to deliver earnings of $1.52 per share, up 71% from a year earlier. Revenue is forecast to climb 67% to $65.6 billion, underscoring the company’s ongoing strength in the AI chip space.

Citi recently suggested that January-quarter revenue could exceed $67 billion, with projections pointing to even stronger results in the April quarter.

Another solid showing in data-center sales, along with widening margins and healthy free cash flow, would bolster the view that Nvidia remains firmly in the midst—not at the tail end—of an AI supercycle.

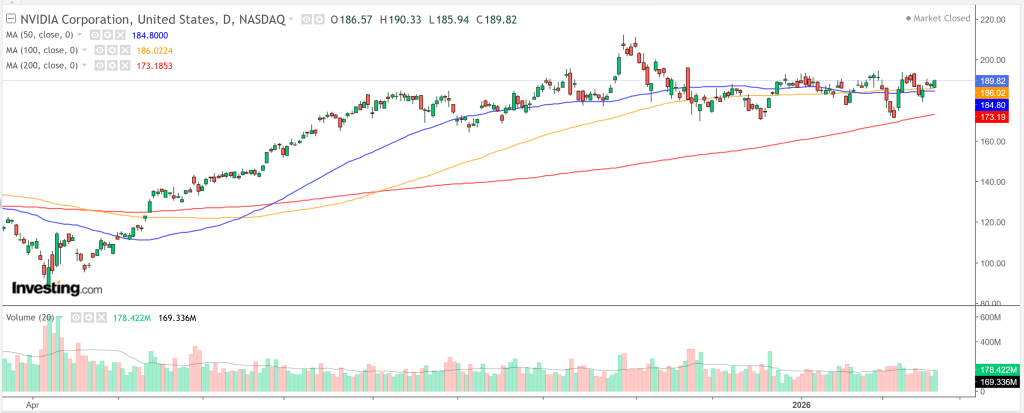

NVDA shares ended Friday at $189.82, consolidating after a strong advance but still positioned to move higher on favorable catalysts. Across multiple timeframes—from intraday charts to the monthly view—technical indicators and moving averages continue to signal a “strong buy.”

A beat-and-raise report could ignite another leg up, particularly if management emphasizes longer-term visibility into 2026–2027 growth driven by next-generation architectures such as Rubin.

Trade Setup:

Entry: Near current levels (around $190)

Target: $210 (approximately 10% upside)

Stop-Loss: $184 (roughly 3.5% downside risk)

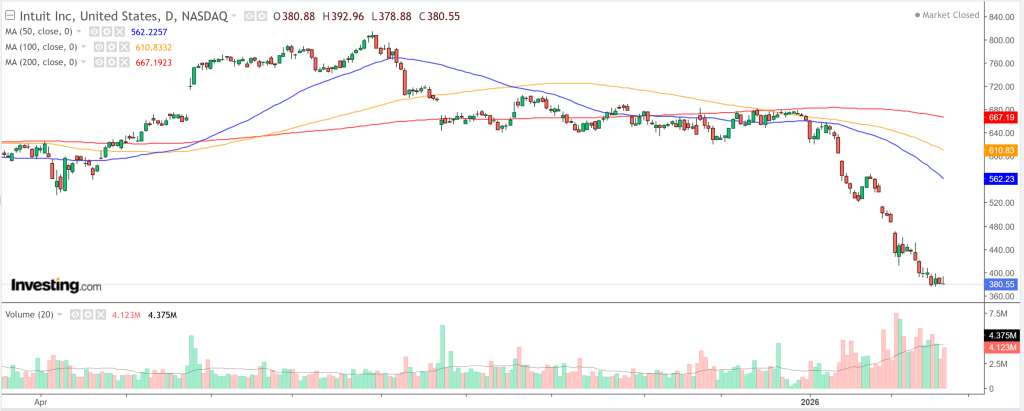

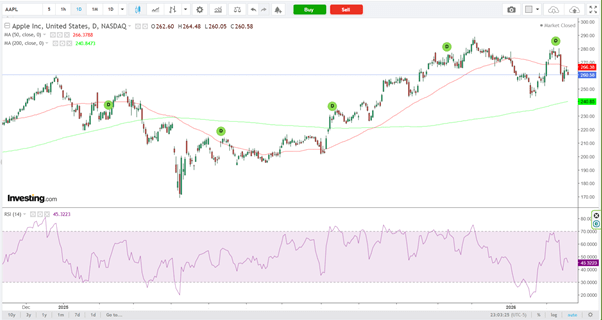

Stock to Sell: Intuit

Intuit—the parent company of TurboTax, QuickBooks, Credit Karma, and Mailchimp—heads into earnings week facing mounting pressure. Concerns have escalated in early 2026 that generative AI tools could weaken its competitive moat across tax prep, accounting, and financial software by enabling free or lower-cost alternatives, custom AI agents, or in-house solutions for small businesses and consumers.

This anxiety has fueled broader “SaaSpocalypse” sentiment, with the software sector shedding trillions in market value. INTU shares have been particularly hard hit in recent months, sliding sharply alongside peers such as Salesforce.

Analyst sentiment has also turned more cautious ahead of the report, with 23 of the last 25 estimate revisions moving lower—signaling growing skepticism around near-term performance.

Wall Street expects Intuit to post earnings of $3.68 per share, up roughly 11% year over year, on revenue of about $4.5 billion. The bigger concern, however, centers less on the headline numbers and more on the narrative surrounding AI-driven disruption.

Although Intuit has made significant investments in artificial intelligence, investors seem to view these efforts as largely defensive—designed to protect its existing franchises rather than meaningfully expand them or counter broader competitive threats. TD Cowen recently cut its price target, pointing to doubts about the strength of Intuit’s AI strategy and intensifying competition.

Any remarks about rising competitive pressures, decelerating growth in key segments, or conservative forward guidance could amplify downside risks—particularly in a stock that may be technically oversold but remains vulnerable in a sentiment-driven market.

Shares of Intuit have fallen 42.5% over the past three months and are now hovering just above their 52-week low of $375.40. Technical signals remain decisively negative: across timeframes—from hourly charts to the monthly view—both moving averages and momentum indicators continue to flash “strong sell.”

With management’s outlook likely to face intense scrutiny, any earnings miss or cautious commentary reflecting a more competitive, AI-driven environment could deepen the selloff.

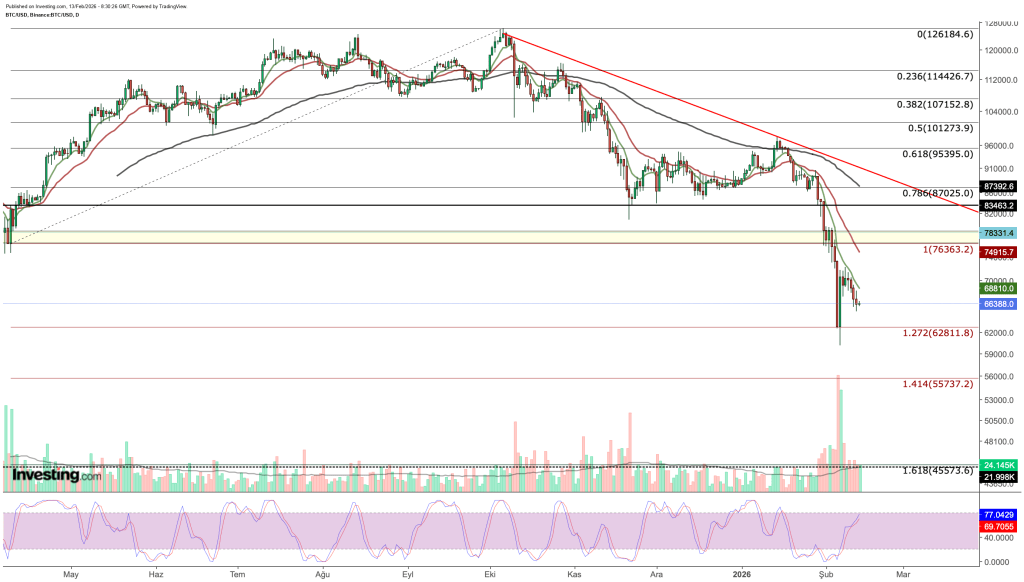

Bitcoin falls beneath the lower boundary of its consolidation range on Monday, and a decisive close below this level could open the door to a more pronounced correction.

Ethereum drops under $1,900, marking a continuation of its six-week decline.

XRP dips below $1.40, unable to hold support at the lower edge of its trendline channel.

Bitcoin (BTC), Ethereum (ETH), and Ripple (XRP) continue to weaken on Monday after posting modest losses last week. BTC has slipped beneath the $65,000 consolidation floor, while ETH has fallen under $1,900, both marking a sixth consecutive week of declines. Meanwhile, XRP drops below $1.40, failing to hold support at its lower trendline — collectively signaling the risk of a deeper correction across the top three cryptocurrencies.

Bitcoin breaks below consolidation support

Bitcoin had been trading within a sideways range between $65,729 and $71,746 since February 7. On Monday, BTC moved below the lower boundary of this range, changing hands near $64,700.

A confirmed daily close beneath $65,729 would strengthen the bearish case and could open the path toward the next major support around $60,000.

On the daily chart, the RSI stands at 31, hovering close to oversold territory and reflecting strong downside momentum. Meanwhile, the MACD lines are tightening, suggesting growing indecision in the market.

BTC/USDT

However, if BTC manages to reclaim and hold above the $65,729 level, a rebound toward the upper boundary of the range at $71,746 remains possible.

Ethereum extends its correction

Ethereum continued to edge lower last week, prolonging its slide that began in mid-January. As of Monday, ETH is down 4.77%, trading around $1,864.

A daily close beneath the lower consolidation boundary at $1,747 would reinforce the bearish outlook and could drive prices toward the next key support at $1,669.

Similar to Bitcoin, Ethereum’s RSI points to strengthening downside momentum, while the MACD lines are narrowing, reflecting growing uncertainty among market participants.

ETH/USDT

On the flip side, a recovery from current levels could see ETH rebound toward the upper end of its consolidation range near $2,149.

XRP deepens its pullback after breaking below key lower trendline support.

XRP is hovering below $1.40 on Monday after slipping beneath the lower boundary of a falling wedge pattern.

Should the pullback persist, the token may slide further toward the weekly support around $1.30.

Similar to Bitcoin and Ethereum, XRP’s RSI points to building bearish pressure, while the MACD lines are tightening, signaling trader uncertainty.

XRP/USDT

On the other hand, if price manages to reclaim and hold the lower trendline as support, a rebound toward the psychological $1.50 level could follow.

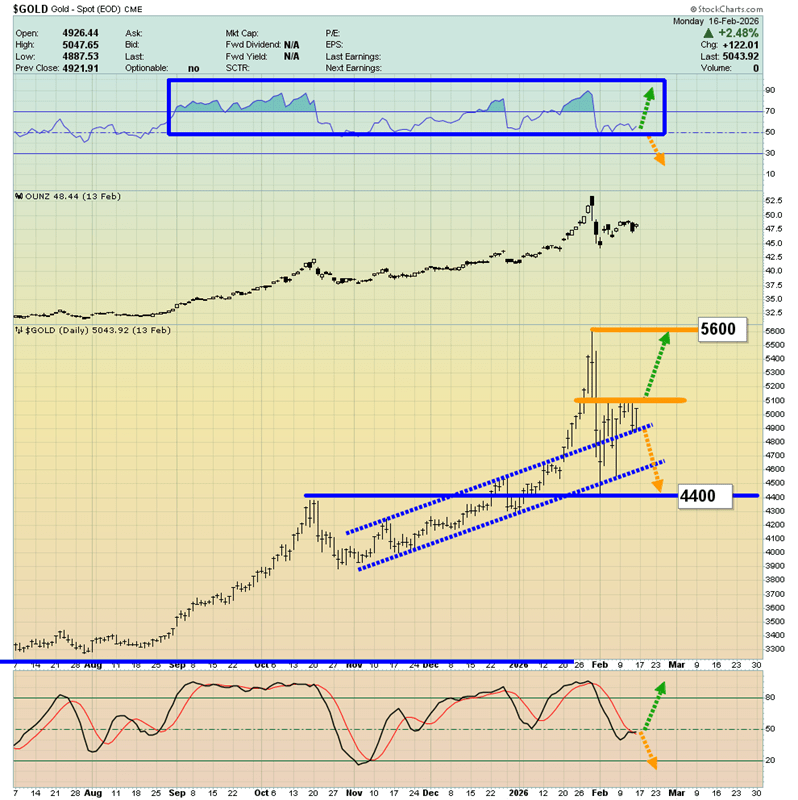

Gold extended its rally for a fourth consecutive session, supported by a mix of favorable drivers.

Ongoing trade uncertainties and escalating geopolitical tensions continued to bolster demand for the safe-haven metal.

Expectations of Federal Reserve rate cuts, along with a broadly softer U.S. dollar, offered further support to the non-yielding asset.

Gold (XAU/USD) posted its strongest-ever weekly close above the $5,100 level on Friday and carried that momentum into the new week. The metal has now advanced for a fourth consecutive session, climbing past $5,150 during the Asian session to reach a fresh monthly high. Persistent trade-war concerns and escalating geopolitical tensions in the Middle East continue to channel safe-haven flows into bullion.

U.S. President Donald Trump introduced a new trade framework after a Supreme Court ruling blocked his earlier sweeping tariff plan, announcing a 15% global tariff on imports—the maximum permitted under the law. The move heightened fears of retaliatory action and broader economic fallout from supply chain disruptions, dampening risk appetite and reinforcing demand for gold as a defensive asset.

On the data front, Friday’s release showed the U.S. Personal Consumption Expenditures (PCE) Price Index rose 2.9% year-over-year in December, while the core measure increased 3.0%, tempering expectations of a March rate cut by the Federal Reserve. Even so, markets continue to anticipate the possibility of two 25-basis-point reductions later this year.

Those expectations were supported by weaker U.S. growth figures, with GDP expanding at a 1.4% annualized pace in the fourth quarter—slowing sharply from 4.4% in Q3—amid the longest government shutdown on record. Combined with trade-related uncertainty, the softer growth backdrop has pulled the U.S. dollar back from last week’s highs, adding further support to non-yielding gold.

Additionally, the risk of military confrontation between the U.S. and Iran has contributed to the metal’s upward momentum. Officials from both sides are scheduled to meet in Geneva on Thursday after Iran submitted a detailed nuclear proposal. Reports indicate that President Trump is weighing potential military action if diplomatic efforts fail to restrain Tehran’s nuclear ambitions, further underpinning safe-haven demand.

XAU/USD H4 chart

Gold buyers remain in control, with Friday’s surge beyond the $5,100 level still holding firm.

From a technical standpoint, the solid upside continuation at the beginning of the week confirms last Friday’s breakout above the $5,100 horizontal resistance, reinforcing the bullish outlook for XAU/USD. The MACD remains above both the Signal line and the zero level, while the expanding positive histogram points to building upward momentum.

In addition, gold is trading comfortably above the ascending 200-period EMA, which underpins the current advance and keeps the near-term bias skewed to the upside. However, the RSI at 73.23 signals overbought conditions, suggesting that immediate gains could be capped.

As long as prices stay above the rising 200-period EMA at $4,864.04, the broader bias remains constructive, with dips likely to be limited. The MACD continues to support the bullish case, though a narrowing histogram would indicate fading momentum. With the RSI stretched into overbought territory, a period of consolidation or mild pullback may emerge before the uptrend resumes. Still, holding above the 200-period EMA would preserve the overall recovery structure, even if short-term consolidation unfolds.

Oil prices fell more than 1% in Asian trading on Monday, taking a breather after last week’s sharp rally, as investors assessed the likelihood of a third round of U.S.-Iran nuclear negotiations and renewed uncertainty around U.S. trade policy.

By 20:50 ET (01:50 GMT), Brent crude for April delivery dropped 1% to $71.03 a barrel, while WTI crude declined 0.9% to $65.75 a barrel.

Both benchmarks had climbed nearly 6% last week amid signs of a potential U.S.-Iran confrontation and an unexpected drawdown in U.S. crude inventories, which supported prices.

Traders watch third round of U.S.- Iran nuclear talks

Iran and the United States are expected to hold a third round of nuclear discussions on Thursday in Geneva, raising hopes that tensions may ease.

Iranian Foreign Minister Abbas Araghchi told CBS’s “Face the Nation” on Sunday that there is a strong possibility of reaching a diplomatic resolution, adding that an agreement is within reach. Markets viewed the remarks as a signal of potential compromise.

Iran is a major producer within OPEC and possesses some of the largest proven oil reserves globally. The country also borders the Strait of Hormuz, a vital chokepoint that handles about one-fifth of the world’s seaborne oil. Any escalation involving Iran could disrupt shipments and drive up freight and insurance costs.

Trump raises global tariffs to 15%

Meanwhile, U.S. President Donald Trump unveiled new global tariffs, initially imposing a 10% duty on imports for 150 days after the U.S. Supreme Court invalidated his previous, broader tariff plan.

The administration increased the rate to 15% on Saturday—the maximum permitted under the applicable law—adding fresh uncertainty to global trade and demand prospects.

Higher tariffs can strain supply chains and prompt retaliatory actions from trade partners. Slower trade activity and weaker industrial production typically weigh on fuel consumption.

Gold extended its rally for a fourth consecutive session on Monday, building on last week’s advance as new global tariff measures from U.S. President Donald Trump and softer U.S. economic data boosted demand for safe-haven assets.

Spot gold climbed 0.8% to $5,143.55 an ounce by 19:53 ET (00:53 GMT), while U.S. gold futures jumped 1.7% to $5,165.86.

Bullion gained more than 1% last week as escalating geopolitical tensions between the U.S. and Iran encouraged a risk-off tone across markets.

Late last week, Trump announced a 10% tariff on global imports for 150 days under Section 122 of U.S. trade law, following a decision by the Supreme Court of the United States to strike down a broader tariff framework. The administration subsequently increased the levy to 15%—the maximum permitted under the statute—heightening fears of retaliatory actions and disruptions to global supply chains.

The tariff move dampened investor sentiment, driving flows into traditional safe havens such as gold and U.S. Treasuries. Ongoing uncertainty about how long the tariffs will remain in place, along with potential legal and congressional challenges, added to market volatility.

Gold also found support in recent U.S. data. The economy expanded at an annualized 1.4% pace in the fourth quarter, a notable slowdown from the prior quarter. Meanwhile, the Personal Consumption Expenditures (PCE) price index—the inflation measure favored by the Federal Reserve—rose 2.9% year-on-year in December, with core inflation near 3.0%, still above the central bank’s 2% target.

The mix of moderating growth and persistently elevated inflation strengthened gold’s role as both a hedge against economic uncertainty and a store of value.

The US dollar at one stage surged sharply against the Mexican peso, but by week’s end it had given back some of those gains. The 17.00 area below continues to act as a key support zone, and a decisive break beneath it could open the door for a move toward 16.50.

While short-term bounces are possible, the broader setup suggests selling into strength. The 17.50 region remains a significant resistance barrier, and the wide interest rate differential still strongly favors the Mexican peso.

S&P 500

The S&P 500 pulled back early in the week but appears to be stabilizing as it continues to trade within a broader consolidation range. Since early December, price action has been confined between 6,800 and 7,000, suggesting a market building momentum for its next major move.

The bias still leans to the upside. A decisive daily close above 7,000 could trigger a stronger breakout and accelerate gains. On the other hand, a breakdown below 6,800 would signal a shift in tone and mark a more bearish development.

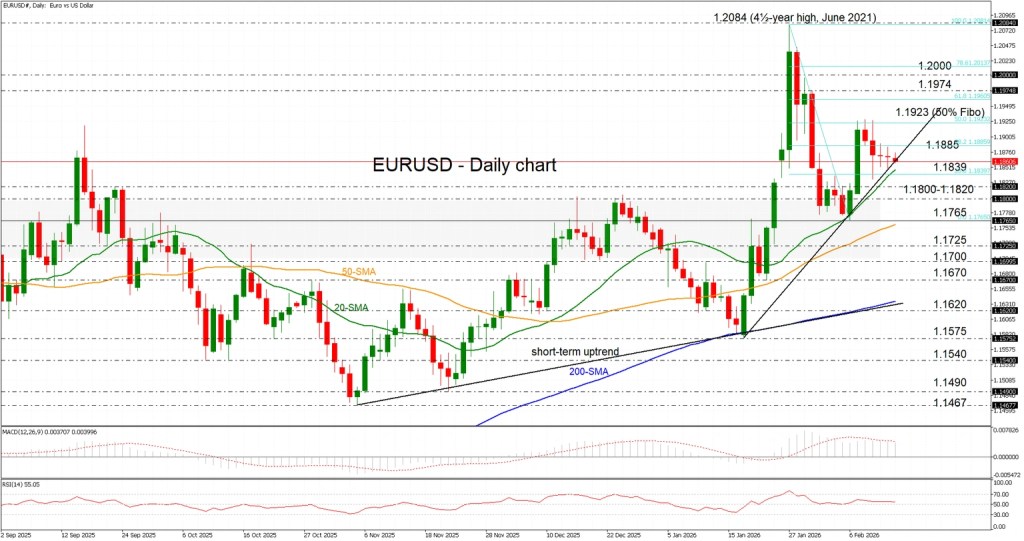

EUR/USD

The euro declined notably over the course of the week, but it continues to find buyers near the 1.18 level, making that area especially important to watch. Given the current structure, caution is warranted when trading this pair.

Price action appears largely range-bound, with 1.18 acting as a central pivot or magnet. Resistance stands near 1.1850, while solid support can be found around 1.1750, reinforcing the broader sideways pattern.

USD/CAD

The US dollar has advanced against the Canadian dollar, but price action remains choppy around the 1.3750 zone — an area that has repeatedly proven significant. The pair appears to be oscillating as traders assess whether momentum can build for a sustained move higher.

A decisive push and hold above 1.3750 would signal renewed strength for the US dollar. Conversely, a breakdown below 1.35 would represent a notably bearish shift in sentiment.

Major Technical Support and Resistance Levels

Gold (XAU/USD)

Gold remains choppy, initially easing back during the week, yet buyers continue to emerge on dips, stepping in whenever prices soften. The 4,800 level appears to be firm support, while the 5,000 mark is likely to act as a psychological magnet for price action.

The broader bias still favors buying pullbacks, with the expectation of an eventual move higher. However, volatility may persist after the sharp turbulence seen in recent weeks, following what had previously been a near one-way surge. Over the longer term, a retest of the highs seems plausible, though it will likely require patience amid ongoing fluctuations.

Bitcoin (BTC)

The Bitcoin market is still searching for renewed upside momentum, but the encouraging development is that price action has at least stabilized. Given the prolonged weakness seen in recent periods, simple stability is a constructive step forward for the market.

The $60,000 level remains a crucial support zone and a major psychological benchmark. Holding above this area is essential if Bitcoin is to maintain any realistic prospect of a sustained recovery.

USD/JPY

The US dollar posted solid gains against the Japanese yen over the week, with the ¥152 level continuing to provide strong support. The 50-week EMA is positioned just beneath that area, reinforcing the floor and encouraging dip-buying as the interest rate differential remains in favor of the US dollar.

With the Bank of Japan maintaining its current policy stance, there appears to be little immediate catalyst for a structural shift. As a result, the pair may be entering a consolidation range between ¥152 on the downside and ¥158 on the upside. A decisive move above ¥160 would represent a significant breakout, clearing a resistance zone that has been in place since 1990.

GBP/USD

The British pound declined sharply during the week, dropping to test the 1.35 level — a large, round psychological threshold that has proven important on multiple occasions. The fact that buyers are attempting to defend this area is at least a constructive short-term signal.

However, recent UK economic data has been somewhat underwhelming. As a result, sterling may currently be one of the weaker major currencies against the US dollar. This pair deserves close monitoring, as broader dollar strength could translate into pronounced downside pressure here, potentially making GBP/USD particularly vulnerable.

Cryptocurrency markets moved within a tight range late in the week as traders remained cautious ahead of important U.S. inflation and growth releases. According to Nexo analyst Iliya Kalchev, broader macro uncertainty continues to guide investor sentiment.

Bitcoin held just above the $68,000 mark, while Ethereum struggled to push past $2,000, signaling selective positioning rather than a broad return to risk appetite. A more guarded macro tone has emerged in recent days, with hawkish cues from the Federal Reserve’s January meeting minutes pressuring risk assets and strengthening the view that interest rate cuts may come later than previously anticipated.

Geopolitical concerns have further shaped market behavior. Heightened tensions involving the U.S. and Iran have driven demand for traditional safe havens such as the U.S. dollar and gold, while capping gains in liquidity-driven assets like cryptocurrencies.

Kalchev highlighted that U.S.-listed Bitcoin ETFs posted around $165 million in net outflows, and Ethereum ETFs saw roughly $130 million withdrawn. These flows reflect a broader sense of institutional caution as investors recalibrate exposure amid persistent macro volatility.

Bitcoin remains in a consolidation phase following its early-February pullback, even as underlying network metrics improve. Mining difficulty has risen notably, and hashrate levels have recovered, pointing to structural strength despite muted price action. Still, analysts note that the asset remains highly responsive to macro signals—particularly inflation data that could influence Federal Reserve policy expectations.

Outside of crypto, financial markets have displayed uneven risk appetite. Gold is trading near record highs, and the dollar is on course for a strong weekly advance as investors hedge against geopolitical instability and interest rate uncertainty.

Looking ahead, market participants are closely watching upcoming U.S. Core PCE inflation data and GDP figures. These releases could determine whether digital assets break out of their current consolidation range or continue moving sideways. While regulatory progress on stablecoin legislation may serve as a longer-term structural driver, Kalchev emphasized that near-term price movements will likely remain tied to macro developments and investor positioning.

The artificial intelligence trade faces its biggest test of the year this week as three cornerstone companies in the AI infrastructure ecosystem prepare to deliver quarterly earnings. With tech stocks showing signs of fatigue, investors want more than simple earnings beats. They’re looking for proof that heavy capital expenditure is translating into the successful deployment of next-generation hardware. All attention will turn to the after-market close (AMC) on Wednesday and Thursday to see whether the AI rally still has momentum.

NVIDIA: The undisputed AI infrastructure leader

NVIDIA (NVDA) is set to report fiscal Q4 2026 results on Wednesday, Feb. 25, after market close. As the dominant supplier of GPUs powering large language models, NVIDIA remains the clearest gauge of the AI trade’s health. Wall Street is anticipating a “beat and raise,” with consensus revenue estimates around $65.6 billion — an impressive 67% year-over-year increase.

Investors are especially focused on the production ramp of its Blackwell architecture chips. Any updates on supply chain constraints or the development timeline for the upcoming Rubin platform could influence not only tech stocks but the broader S&P 500. Options markets imply a potential 6.5% swing in either direction, making NVIDIA’s earnings the week’s must-watch event for global investors.

Hardware and cloud players: CoreWeave and Dell under the spotlight

On Thursday, Feb. 26, AMC, attention shifts to the physical backbone of AI infrastructure. CoreWeave (CRWV), a specialized cloud provider and key NVIDIA partner, will report against high expectations driven by its sizable revenue backlog. Analysts project Q4 revenue of roughly $1.53 billion, but the more significant figure is its $56 billion backlog — a forward-looking signal of how much computing capacity AI firms and tech giants are securing

Also reporting Thursday is Dell Technologies (DELL), which has repositioned itself as a major supplier of AI-optimized servers. Consensus forecasts call for earnings of $3.53 per share on $31.6 billion in revenue. Dell recently earned a spot on Evercore’s “Tactical Outperform” list, supported by a sharp rise in AI server orders and an $18.4 billion backlog exiting last quarter. The key question for Dell will be whether it can preserve margins while rapidly scaling production to meet surging demand for AI infrastructure.

The Australian government has pledged to “consider every possible response” after President Donald Trump raised the standard import tariff to 15%. The abrupt increase came just a day after an initial 10% rate was announced, surprising global markets.

Trade Minister Don Farrell described the decision as “unjustified” and suggested it could strain relations between the long-standing strategic partners. The move follows a U.S. Supreme Court ruling that invalidated the administration’s earlier targeted tariff system as unlawful.

In reaction, the President shifted to a universal global tariff. The first 10% duty is scheduled to take effect at 12:01 a.m. EST on February 24, but the implementation date for the additional 5% remains uncertain, leaving exporters with goods already in transit facing heightened uncertainty.

Economic repercussions and Australia’s reaction

For Australia, the implications are significant. As a leading exporter of iron ore, LNG, and agricultural commodities, a 15% tariff could erode the competitiveness of Australian products in the U.S. market. Trade Minister Don Farrell confirmed that officials are coordinating closely with Australia’s embassy in Washington to evaluate the potential impact.

Analysts note that keeping “all options on the table” may involve filing a formal complaint with the World Trade Organization (WTO) or imposing reciprocal, tit-for-tat duties on American imports. Such action would represent an unusual trade clash between AUKUS allies.

The across-the-board 15% tariff reflects a broad, uniform policy that overlooks customary bilateral arrangements. Should Canberra proceed with countermeasures, it could affect multi-billion-dollar energy and defense agreements that are currently being negotiated.

Market turbulence and the investor outlook

Investors are already responding to the uncertainty. The Australian Dollar (AUD) came under immediate pressure as traders assessed the potential blow to the nation’s trade balance, while mining and energy shares adopted a more cautious tone.

Should the full 15% tariff be implemented without carve-outs, Australian exporters may have to accelerate their shift toward Asian markets, potentially deepening the divide between Western trading partners.

Attention is now fixed on the February 24 deadline. If the White House does not clarify whether allies will receive exemptions, the risk of a formal trade conflict increases. Analysts caution that much of the added cost could ultimately be passed on to American consumers, heightening concerns about renewed inflation.

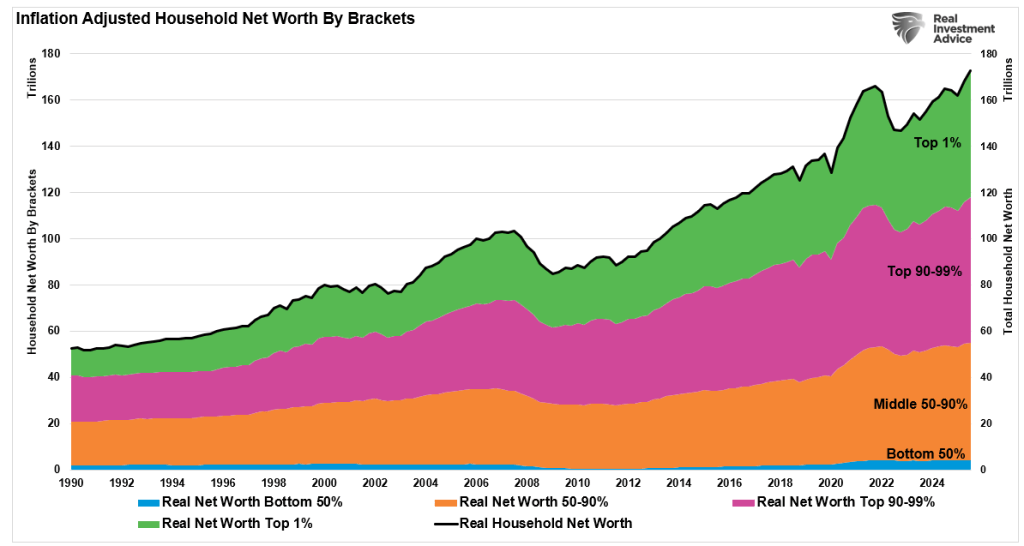

Money — everyone wants it, yet relatively few build lasting wealth. Recent data show the U.S. wealth gap continuing to widen, with the top 10% of earners controlling roughly two-thirds of total assets, while the bottom half owns only a small fraction. The frustration this creates fuels many narratives — corporatism, financial nihilism, inflation, stagnant wages, student debt, policy failures. These factors matter.

But they are not the root cause of individual financial outcomes.

At the personal level, wealth creation has always rested on a small set of enduring principles:

Spend less than you earn.

Save consistently.

Invest intelligently.

These rules are not new. They worked before the internet, before credit cards, and before retail trading apps. Most importantly, they still work — regardless of background, education, age, or economic cycle. Wealth is not a viral trend or a lucky break. It is a disciplined process repeated over time.

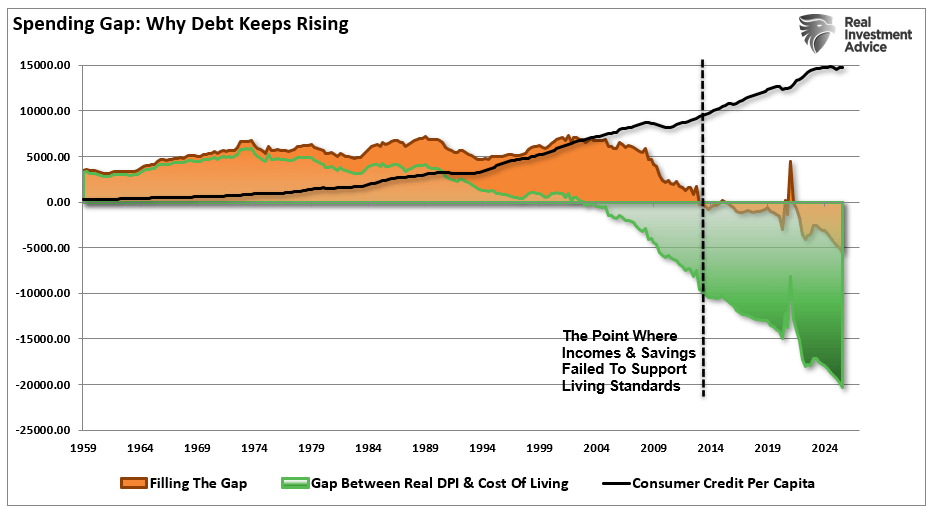

That does not dismiss today’s challenges. Inflation remains elevated compared to early-2000s norms. Real wage growth has struggled to outpace living costs. Mortgage rates have constrained affordability. Yet history shows that disciplined financial behavior, applied consistently, can overcome difficult macro environments.

Many people can articulate why the system feels unfair. Fewer commit to the habits that compound into independence. The difference between chronic financial stress and gradual wealth accumulation is often not luck or privilege alone — it is adherence to a workable framework.

This framework is neither radical nor controversial. It is the same path generations have followed to build stability and prosperity.

One uncomfortable truth is that we have largely failed to teach foundational money skills. Not advanced portfolio theory — but basics: budgeting, understanding credit, living below one’s means, and managing cash flow responsibly.

With that foundation in mind, here are the 10 Immutable Laws of Money.

10 Fundamental Principles of Money

Wealth Isn’t Created Effortlessly

Growing up, my father loved to share stories that, over time, I realized were slightly exaggerated. A few of his classics were:

“When I was your age, I walked uphill to school in the snow — both ways.” “I could see two movies, eat all the popcorn and drink all the soda I wanted for a nickel — and still get change back!” And, of course: “Where do you think money comes from? It doesn’t grow on trees!”

That last line stuck with me the most. What he was really trying to teach was respect — respect for the time, energy, and sacrifice required to earn a living. He often worked two jobs, sometimes even three, to provide for our family. We always had what we needed, though not always everything we wanted. As a child, I didn’t fully grasp the weight of that lesson. It wasn’t until I had a family of my own that I truly understood.

Most people work incredibly hard for their income. Yet it’s surprising how casually many treat the money they earn. They undermine their own efforts by overspending, living beyond their means, or making careless investment choices. If you value the work it takes to earn money, you should value how it’s managed.

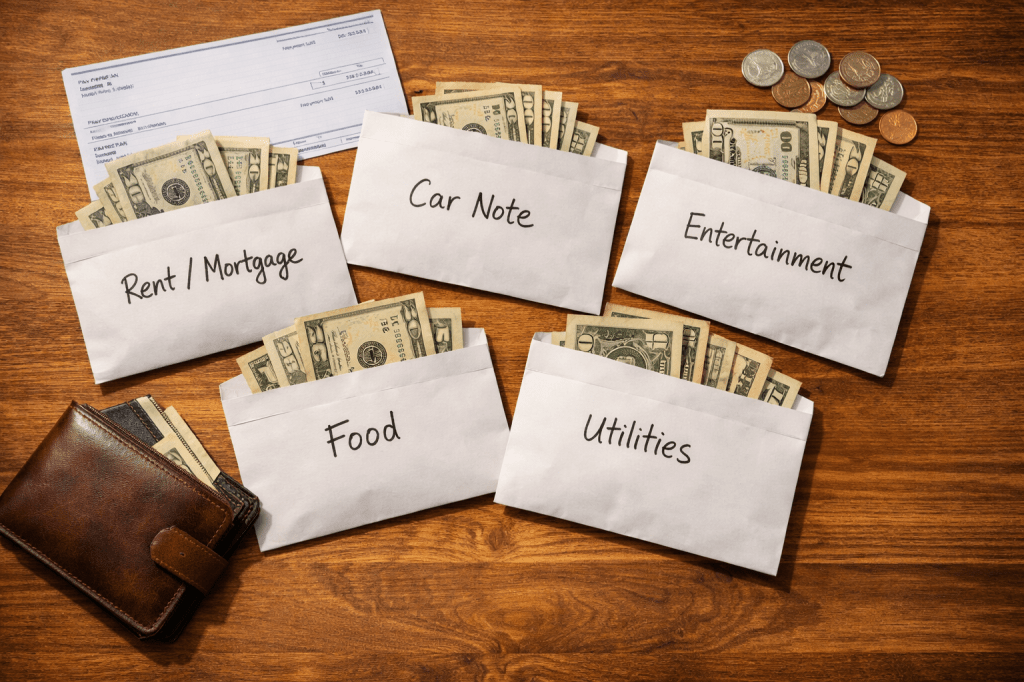

One practical way to build that respect is by using the “envelope system” for a few months.

The idea is simple: cash your paycheck and divide the money into separate envelopes labeled for expenses — rent or mortgage, car payments, groceries, utilities, entertainment, and so on. Then live normally. When an envelope runs out, that category is done for the month. No borrowing from another envelope.

This method quickly reveals where money is leaking away and forces awareness around spending habits. More importantly, it restores discipline and respect for the effort behind every dollar earned.

Note: The envelope system should cover about 80% of your overall budgeting approach, which we’ll explore shortly. The remaining 20% should be directed toward savings — but we’ll tackle that part step by step.

Desires Always Outpace Necessities

When I sit down with people to talk about financial planning, I’m always struck by the reaction the word “budget” triggers. The moment it’s mentioned, you’d think I had suggested something drastic — like giving up a limb.

But the reality is simple: financial success requires one fundamental rule — spend less than you earn.

I constantly hear people justify breaking this rule: “You don’t understand — I needed a new car.” “We needed a bigger house.” “We have to take our annual vacation.”

The line between a “want” and a “need” can occasionally blur, but most of the time they are worlds apart. Did you truly need a brand-new car — or could a reliable two-year-old model have saved you 20% in depreciation? Did you genuinely require more space, or could you have managed in your current home?

These are uncomfortable but necessary questions.

If your goal is to build wealth, your true needs are very limited:

Food

Shelter

Utilities

Taxes

That’s it. Everything else is a want.

Learning to control your wants is one of the most powerful steps toward financial stability. Before making a purchase, pause and ask yourself: Is this a need — or just a desire?

Here’s a practical guideline:

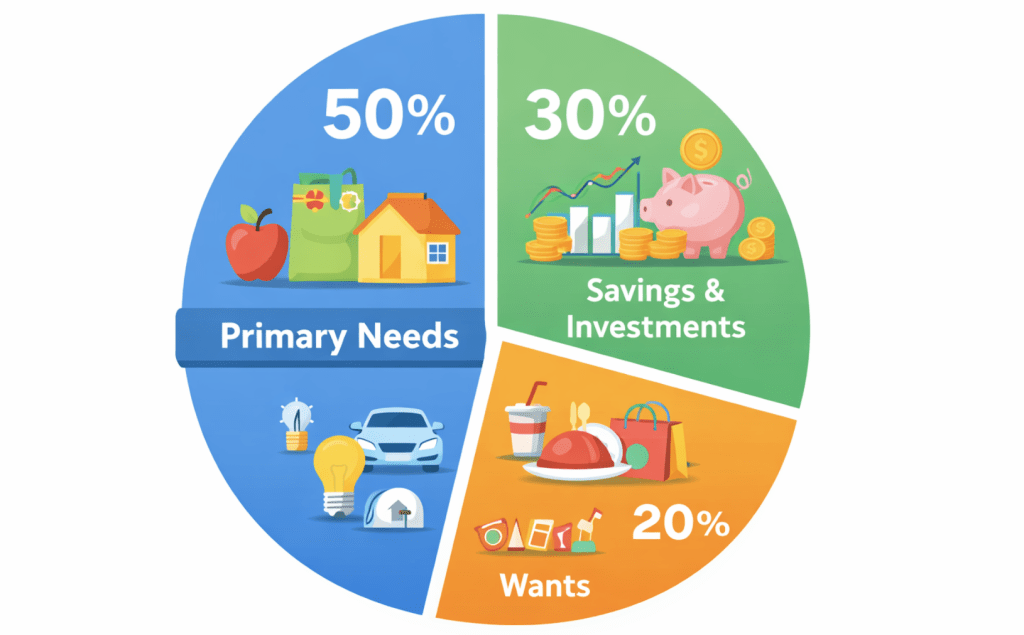

Your life should cost no more than 70–80% of your income.

When creating a budget, review your spending patterns and aim to keep your committed expenses at or below 70–80% of your gross income. That means 20–30% remains uncommitted — and that margin is where financial freedom begins.

This percentage isn’t a rigid law, but it’s a realistic and effective starting point. Once you structure your finances this way, constant expense tracking becomes less necessary. Your account balance itself becomes your guide. The real discipline lies in keeping those fixed obligations under control — and refusing to let wants quietly turn into “needs.”

What About the Remaining 20–30%?

That portion is what you “pay yourself first.”

Let’s break it down with a simple example.

Joe earns $100,000 per year and falls into a 25% tax bracket. If his goal is to save 30% of his income, he needs to set aside $22,500 annually.

Here’s how he does it:

$20,000 goes directly into his employer-sponsored retirement plan on a pre-tax basis.

He then contributes an additional $2,500 each year into a Roth IRA.

Just like that, Joe has hit his savings target.

After taxes and retirement contributions, the paycheck that lands in Joe’s bank account represents roughly 70% of his gross income. And here’s the beauty of the system: Joe is free to spend what’s in that account. He doesn’t have to think about saving — it’s already been handled.

Because the money moves into savings before he ever sees it, he adapts to living on the remaining amount. He never feels deprived because he never mentally counted that savings money as spendable income in the first place.

That’s the real secret to a budget that actually works.

Tracking every dollar you spend isn’t the magic solution — just like obsessively counting calories isn’t the true key to weight loss. The real power lies in building a financial structure that automatically balances income and spending, prioritizes saving, and leaves enough flexibility to absorb life’s inevitable surprises.

When the system is designed correctly, discipline becomes automatic — and wealth becomes a byproduct of structure, not willpower.

The Poor Owe — The Wealthy Own

This principle is straightforward: you cannot borrow your way to wealth — period.

There’s no late-night seminar teaching people how to become rich by shuffling balances between low-interest credit cards. Debt is not a wealth-building tool for consumers — it’s a wealth transfer mechanism, usually in the wrong direction.

For many people, high monthly credit card payments are the very reason their expenses feel suffocating. If you’re carrying significant non-mortgage debt, consider redirecting the 20% earmarked for long-term savings toward aggressively paying it down — but only after you eliminate access to more borrowing.

Every dollar of interest you don’t pay is equivalent to earning a guaranteed, risk-free, tax-free return equal to the interest rate on that debt. Few investments offer that kind of certainty.

And once the debt is gone — which can happen faster than you think if you apply 20% of your gross income toward it — immediately redirect that same money back into savings.

Signs You’re Damaging Your Financial Future

You may be off track if you:

See credit card balances rising while income is shrinking.

Pay only minimums — or less.

Shift balances or take cash advances to cover other cards.

Carry more credit cards than you can track.

Stay near your credit limits.

Charge more monthly than you repay.

Work overtime just to keep up with payments.

Avoid calculating your total debt.

Receive delinquency notices.

Use credit cards for essentials like food or gas.

Rely on credit because you lack cash.

Dip into savings or retirement accounts to cover bills.

Hide purchases from your spouse.

Open every unsolicited card offer.

Fear job loss because your debt load feels unmanageable.

The first step toward wealth is eliminating dependence on credit cards — for any reason. That may sound extreme, but you can’t break a habit while continuing the behavior. There’s no middle ground.

The Credit Card Roll-Up Strategy

If you’re serious about becoming debt-free, this structured approach works:

Cut up all your credit cards. Every single one.

List balances from largest to smallest, along with minimum payments.

Pay minimums on all cards — but pay five times the minimum on the smallest balance.

Repeat monthly. Ignore interest rates for now; the goal is quick psychological wins.

Once the smallest card is paid off, roll that full payment (including its former minimum) onto the next smallest balance.

Continue rolling payments upward until you attack the largest balance with significant monthly firepower.

Momentum builds quickly. What starts small becomes powerful.

When you eliminate your final credit card balance, reward yourself modestly — perhaps with two months’ worth of what used to be your debt payments.

Then immediately return to discipline.

Every dollar that once serviced debt now goes into savings and investment. You’ll have ground to make up — but you’ll also have the structure and momentum to build real wealth.

Debt keeps you working for your past. Savings and investment put your money to work for your future.

You Are Not Immune to Moral or Physical Risk

I remember watching Fear Factor hosted by Joe Rogan and realizing something simple: people will do almost anything for fast, easy money.

“Sure, I’ll eat those South American hissing cockroaches for $50,000.”

Yet many of those same people won’t consistently skip luxuries, reduce spending, or sacrifice short-term comfort to save $50,000 the slow and responsible way.

We’ve been conditioned to look for shortcuts. Instead of discipline, we gamble. The lottery — essentially a tax on poor financial judgment — becomes the dream strategy. Yet roughly 80% of lottery winners end up broke within a decade because sudden money cannot compensate for weak financial habits.

If I borrowed a page from David Letterman, I’d create a segment called “Financially Stupid Human Tricks” — highlighting the so-called “smart” financial moves that often create long-term damage.

Borrowing From Your 401(k)

Many employer-sponsored retirement plans allow loans. It feels harmless. After all, you’re “paying interest to yourself,” right?

Technically true.

But here’s what gets overlooked:

If you lose your job, the loan usually must be repaid within about 60 days.

If you can’t repay it, the balance is treated as a distribution — taxed and penalized.

Depending on your bracket, penalties and taxes can reach 40% or more.

And it gets worse: you can’t restore the lost compounding.

If you borrowed $7,000 and that money could have compounded at 8% annually, over time that single decision could cost tens of thousands — even $75,000 or more — in retirement value.

Your retirement account and your home equity should be financial “break glass only in absolute emergency” assets. If everything else in life goes wrong, those two pillars protect your shelter and your dignity.

Stretching to Buy a House

Homebuyers face enormous pressure.

Real estate agents earn more when you spend more. It’s no accident that you’re often shown a home slightly beyond your range first. Once you’ve walked through the upgraded kitchen and spa bathroom, the affordable house feels like a compromise.

Friends and family may encourage the stretch: “It’s an investment.” “You’ll earn more later.” “Real estate always goes up.”

Maybe. Maybe not.

Being “house poor” is real. When too much of your income goes toward housing, everything else suffers — vacations disappear, dining out shrinks, retirement contributions stall, college savings fade. Instead of cutting lifestyle, many simply layer on more debt to preserve appearances.

A house should support your life — not dominate it.

The common thread in all of this is risk blindness. People assume bad outcomes won’t apply to them. They believe they’ll keep the job, the market will cooperate, income will rise, and nothing unexpected will happen.

But wealth isn’t built on optimistic assumptions. It’s built on margin, discipline, and respect for risk.

Quick money excites. Structured money endures.

The Most Valuable Things in Life Don’t Cost Money

Too often, we confuse “quality time” with “costly activity.” We assume that spending meaningful time with family or loved ones requires tickets, reservations, travel, and swiping a credit card.

But isn’t the real goal connection?

You don’t need a weekend getaway to build memories. You need presence.

Learn to be creative:

Board games at home

Playing sports in the yard

A walk in the park with music or an audiobook

Movie nights with homemade popcorn